We’re back again with another monthly investor’s update, this time, wrapping up December 2025.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

As we move into 2026, the Australian economy shows a complex mix of resilience and pressure.

The residential property market remains a primary driver of national wealth, with significant growth in cities like Brisbane, Adelaide, and Perth, fuelled by a chronic shortage of available stock and the lagged effects of earlier rate cuts, even as the broader market began to cool toward the December holidays.

The narrative has shifted significantly from a few months ago. While many had hoped for a cycle of easing, the RBA has signalled that further rate cuts are unlikely in the short term. In fact, with inflation proving difficult to anchor, several major economists are now pricing in the possibility of a “fine-tuning” rate increase as early as February, depending on the next batch of data. However, this commentary has softened somewhat with the release of the CPI data for November, which showed that underlying inflation remains sticky at 3.2%.

What’s Next?

All eyes are now on the December 2025 quarterly CPI release, due at the end of January. Markets are bracing for potential volatility; if the quarterly print exceeds 0.8%, it may force the RBA’s hand toward a hike to ensure inflation returns to the target band by 2027.

Despite the “higher for longer” interest rate outlook, we expect the property market to remain resilient. While higher borrowing costs will naturally act as a handbrake on affordability, the sheer lack of housing supply continues to provide a floor for prices. Government efforts to stoke demand via first-home buyer schemes are still clashing with the reality of slow construction timelines, high material costs, and a shortage of skilled labour.

Consequently, our view is that while the rapid price surges of early 2025 may transition into a period of more moderate, stable growth, the fundamental “supply-demand” imbalance will prevent significant market correction in the year ahead.

Finally, we hope you had a restful break, and we look forward to a healthy and prosperous 2026 ahead!

To learn more, see our Investor FAQs.

Lending Activity Update

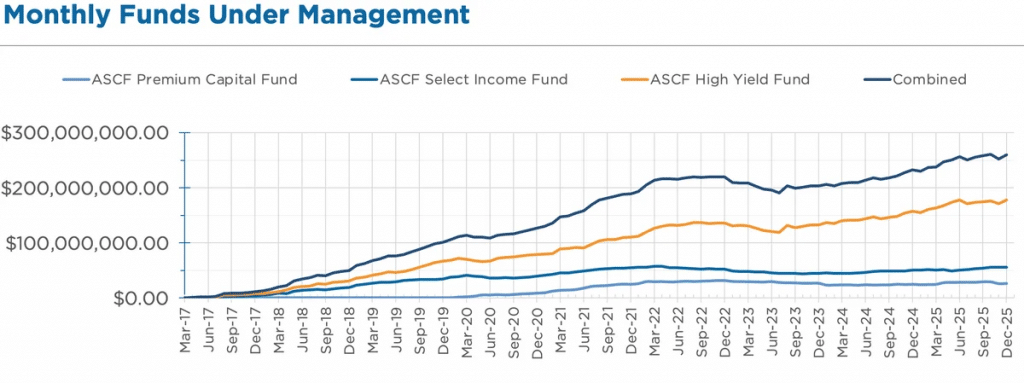

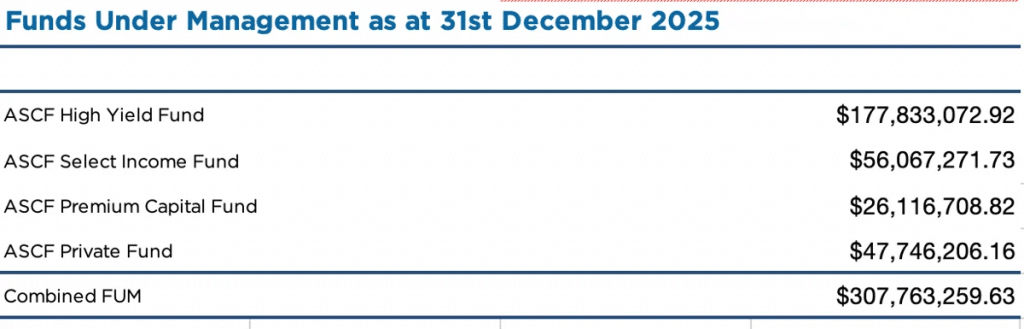

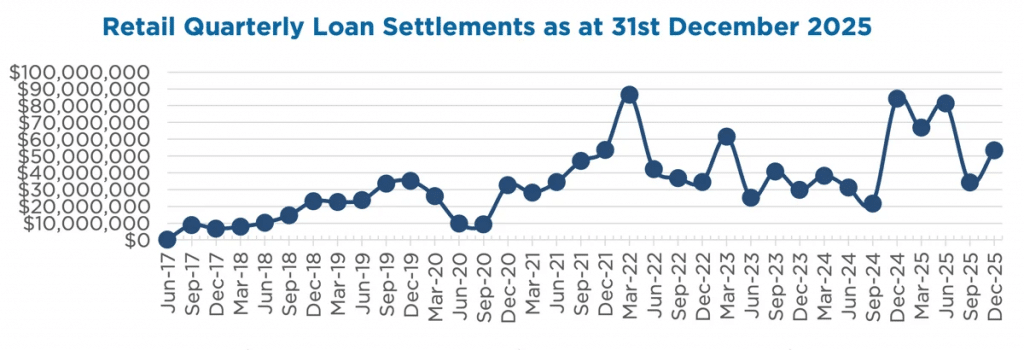

In December, loan originations and inquiry levels were strong, with $19,150,449.14 in loans settled.

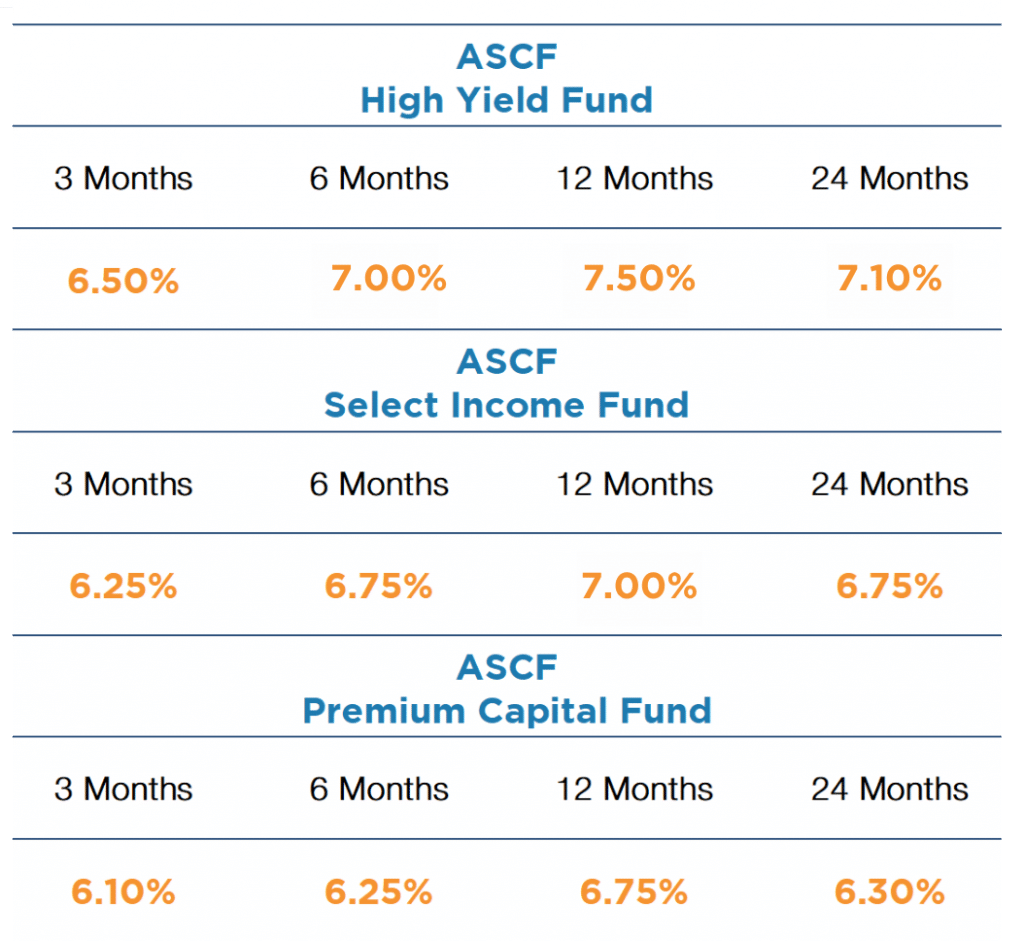

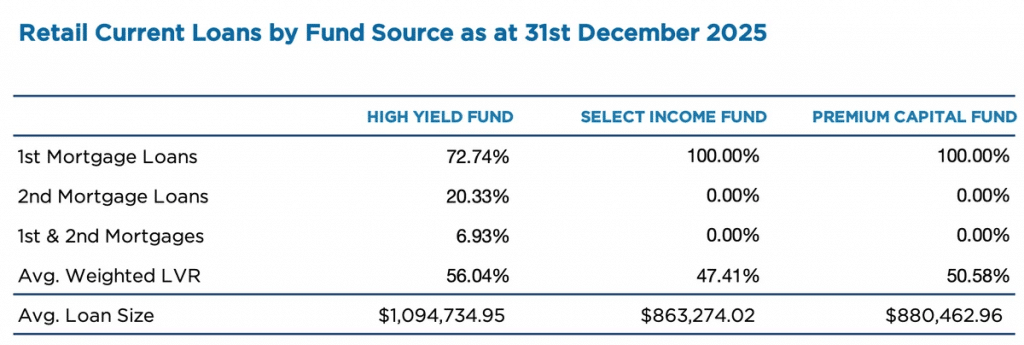

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of December.

To learn more, see our Borrower FAQs.

Why Invest With ASCF?

How ASCF Assesses and Manages Loans: A Behind-the-Scenes Look

One of the questions investors often ask me is: how do we assess the loans we undertake?

Usually, they are surprised at the lengths we go to in this assessment. However, this level of detail is essential, as we not only need to look after the security of the investment funds, but also stay compliant with a number of lending regulations.

At ASCF, capital preservation comes first. We assess every loan on its individual merits, using a structured, conservative approach designed to protect investor capital while generating reliable income.

It’s More Than Just Property Value

While the value of the underlying asset is important, it is only one part of the assessment equation. A strong valuation alone does not automatically make a loan suitable.

Rather, each loan must pass several layers of assessment.

Asset Type

The type of the asset is very important and has a direct bearing on the LVR. For instance, a residential property typically has a much higher chance of selling quickly than a commercial property. This is one of the factors we consider when determining the percentage of the asset we are prepared to loan against.

A Sensible Loan Purpose

Additionally, we look closely at why the borrower is seeking funds.

The loan purpose needs to be logical, transparent, and commercially sound, as loans that demonstrate a clear and sensible use of funds are far more likely to perform as expected.

Assessing the Borrowers

What’s more, ASCF assesses the character and track record of the borrower by asking a range of questions to ensure they fully understand what they are undertaking. If necessary, we also consider whether they have previous experience to support their plans. A borrower’s willingness and capacity to honour their obligations is a key part of our decision-making process.

Location Matters

The location of the asset also has a bearing on whether we want the loan and to what LVR we are prepared to go. We need to factor in the potential time to sell the asset should the need arise.

A Clear and Viable Exit Strategy

Every loan must have a realistic and achievable exit strategy (or strategies), which we also assess.

Common examples may include:

- Sale of the property.

- Refinancing through traditional lenders.

- Business cash flow.

If the borrower intends to use a traditional lender as their exit strategy, we need to be sure they service with a mainstream lender. Accordingly, we will run serviceability tests, and if the exit strategy is a sale, we will ensure the loan term is sufficient to enter into a contract and settle within the timeframe.

Ongoing Oversight

Once a loan is approved and funded, it doesn’t just disappear into the background.

We monitor their progress and keep a close eye on payments where required to maintain a gauge and to provide confidence that we are still on track.

Want to learn more? Contact us to explore your investment options.

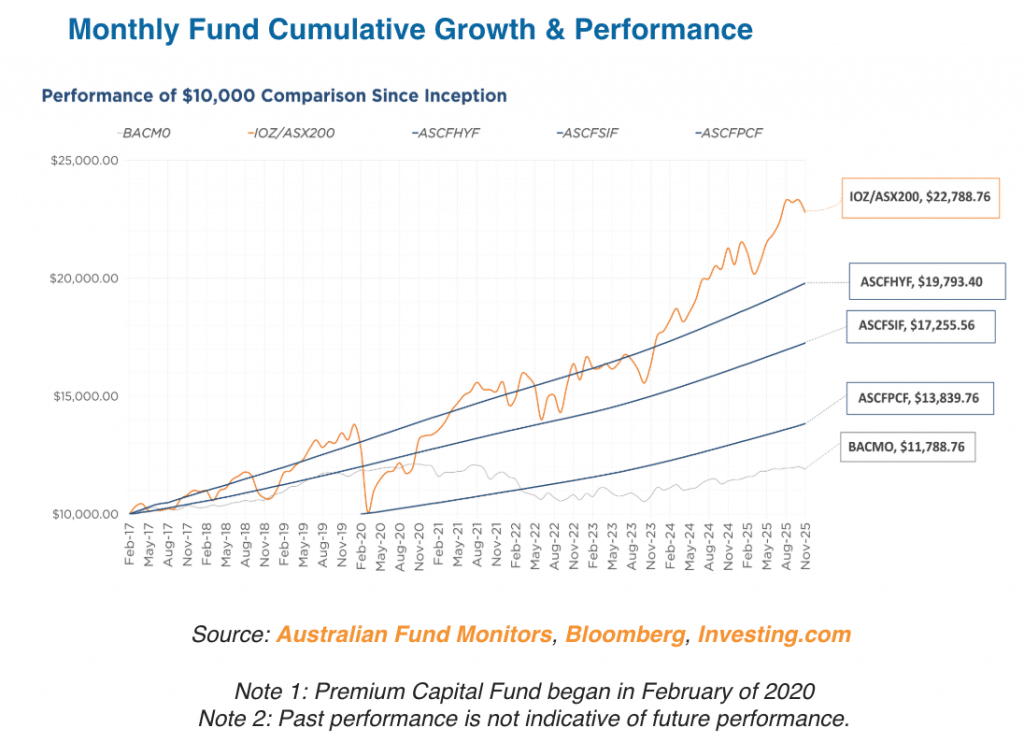

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem

A Finsure broker presented a client to us who was seeking funding to complete the renovation of a residential investment property in Malvern, VIC, which was to be sold upon completion. The customers contributed $1 million of their own funds into the renovation, but ran out of money before it was complete. This left them in a tricky situation, as traditional lenders are not interested in funding incomplete construction transactions.

Solution

ASCF engaged one of our panel valuers in Melbourne to complete both an “as is” and “as if complete” valuation, which came in at $1,975,000 and $2,400,000 respectively. We were able to offer the customer a gross loan amount of $282,000 on a 2nd mortgage over a 6-month term with retained interest for the term of the loan at an interest rate of 14.95% pa. The net proceeds of the loan were sufficient to meet the funding required to complete the renovation and prepare the property for sale. The LVR of 55.59% was based upon our valuer’s “as is” valuation amount.

What ASCF Does Differently

With builders continuing to experience upward pressure on building costs and delays, we are seeing an increasing number of these incomplete construction scenarios. Where there is sufficient equity, we continue to help our customers complete their projects when the traditional lenders in the market will not.

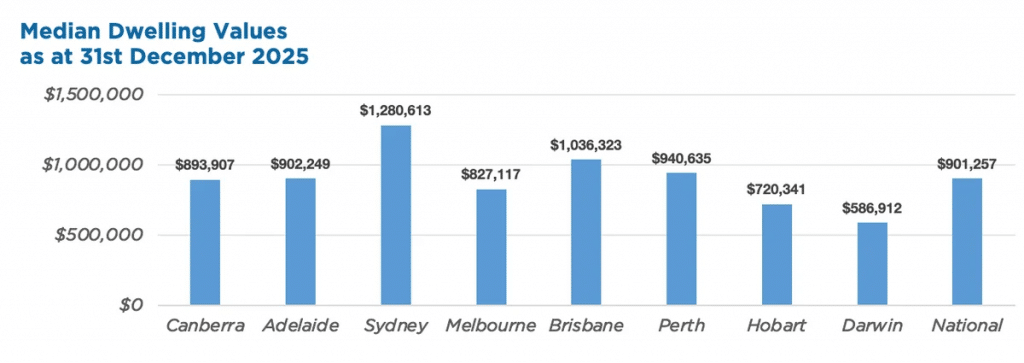

Market Update

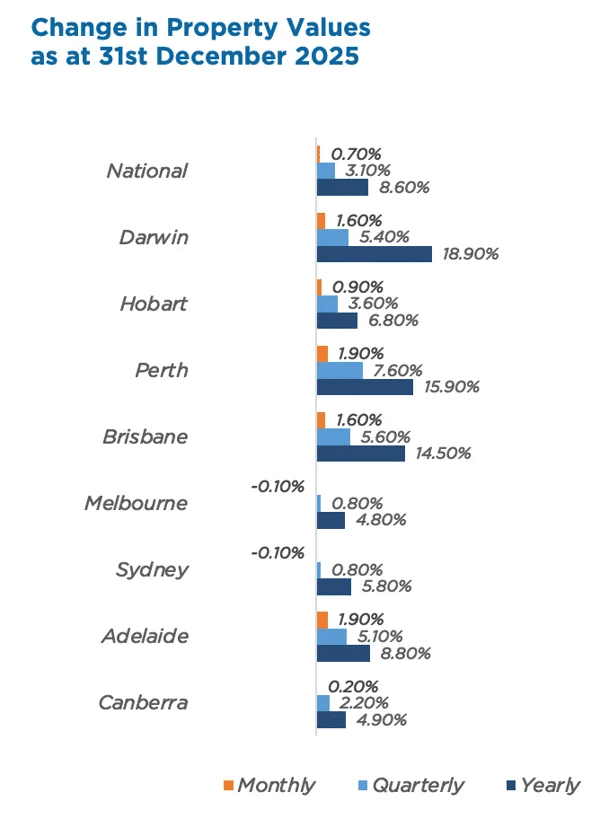

December saw the smallest national pricing gain in five months, rising by just 0.7%. Values in Melbourne and Sydney declining by 0.1% dragged this figure down. In contrast, Brisbane, Adelaide, Perth, and Darwin all saw increases of 1.6% or higher.

More broadly, the Australian housing market finished 2025 strongly, with the national median dwelling value surging 8.6% over the year—the most since 2021. Regional markets outperformed capital cities with a 9.7% annual rise, compared to 8.2% for the capitals.

In 2026, while economic uncertainty and affordability may temper the pace of growth, a persistent shortage of new housing supply should act as a floor for property values, protecting against significant price drops.

Source: Cotality HVI, 1 Jan 2026