We’re back with another ASCF investor’s update, analysing all the key economic and investment trends from the past month, from RBA prospects, to inflation, to the employment market, and beyond.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

After last month’s decision to hold the official cash rate at 4.35%, focus now turns to the RBA’s next meeting on August 11th.

CommBank, ANZ, and NAB are expecting the Board to remain on hold for the foreseeable future, and we tend to concur that the RBA is unlikely to raise rates at its next meeting or for the remainder of 2026. Westpac remains the hawkish outlier, predicting further rises in August and September. We believe the full impact of the recent budget changes are yet to be absorbed by the economy, and that they will have a stifling impact on GDP growth and result in weaker-than-expected unemployment and inflation data over the remainder of the year.

Inflation & Employment

Headline CPI inflation was 4% in the 12 months to May 2026, down from 4.2% in the 12 months to April, largely driven by a 3.8% seasonally adjusted decline in transport costs between April and May.

In the job market, the unemployment data released yesterday showed unemployment held steady at 4.4%. The RBA expects this to “increase to 4.7 per cent by mid-2028”, which, if inflation declines as expected over the next 12 months, should allow the RBA to start cutting rates by mid-2027.

The Westpac Melbourne Institute Consumer Sentiment Index was up 4.1% to 83.9 in July. However, this remains in the bottom 10% of historical readings, and we expect this figure to remain subdued until we get a clearer indication from the RBA on interest rates.

Property Market

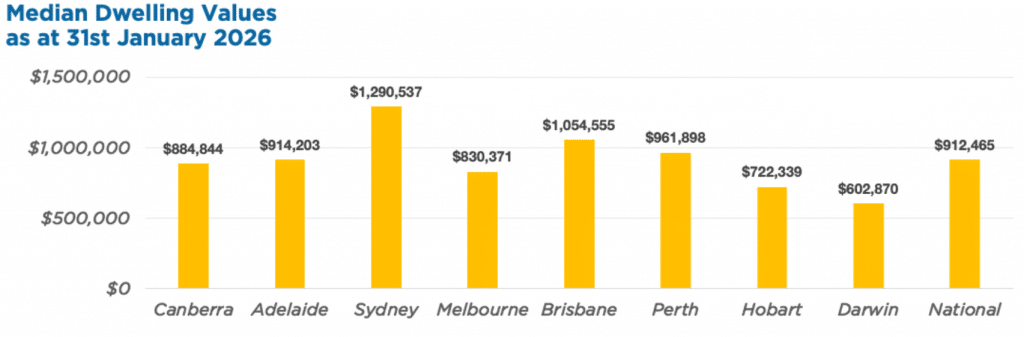

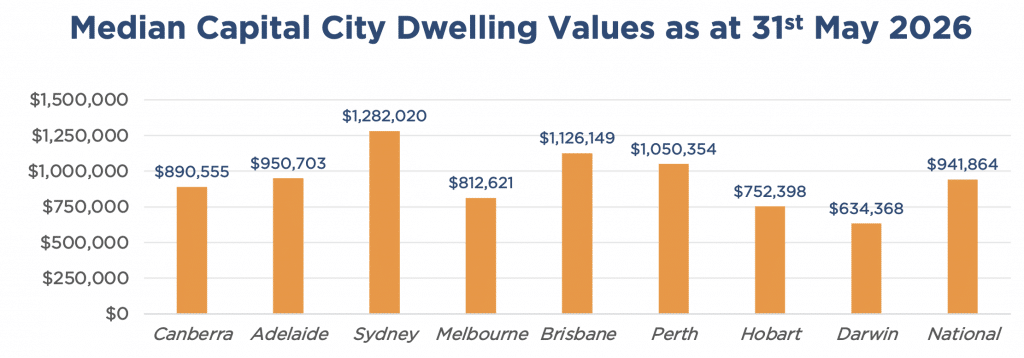

Australian property values fell in June for the first time since December 2024, posting a national decline of -0.4%. Regional areas have been more resilient in the face of this slowdown, posting a combined 0.3% monthly increase, compared to a -0.6% decline across the combined capital cities.

We expect Sydney and Melbourne to decline slightly further, but are not expecting any significant falls over the remainder of the year. Instead, our expectation is a decline in the national median house price of circa 4% from peak to trough, as the full impact of the budget changes to housing investment are absorbed.

To put this into perspective, the national median house price increased by 7.3% over the last 12 months, and the structural undersupply of housing is an ongoing issue which will continue to support house prices nationally, as we believe that the recent budget policy changes will have minimal impact on increasing the supply of new housing.

2026 Tax Certificates Now Available

Tax Certificates for the financial year ending 30th June 2026 are now available to download through our Online Portal, under the Annual Statements tab.

If you are not registered for the portal, please contact us on 07 3506 3690, and our friendly team will assist you with the registration process.

How ASCF Helps

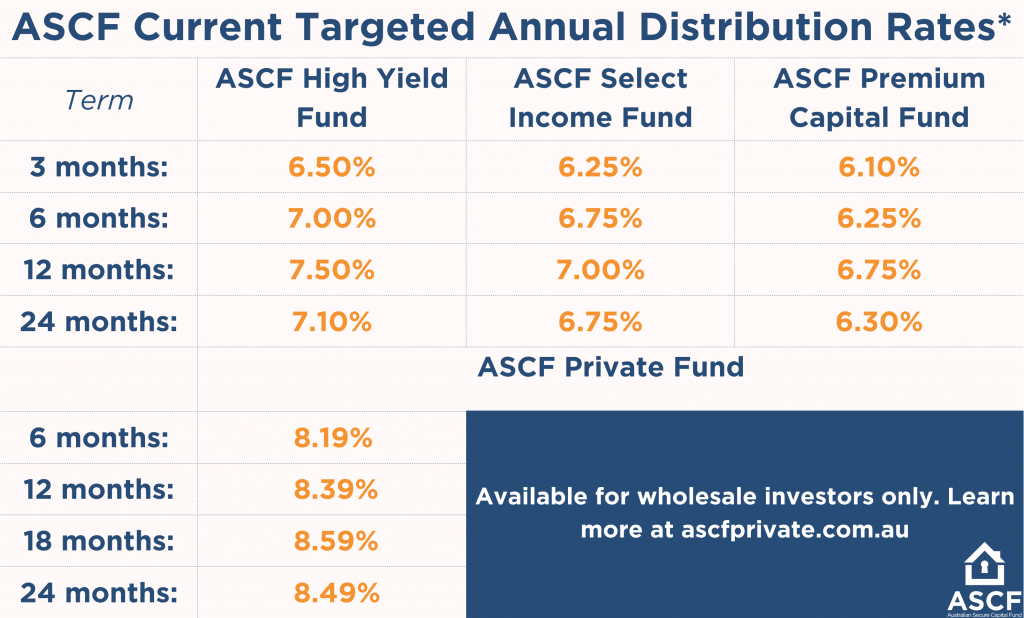

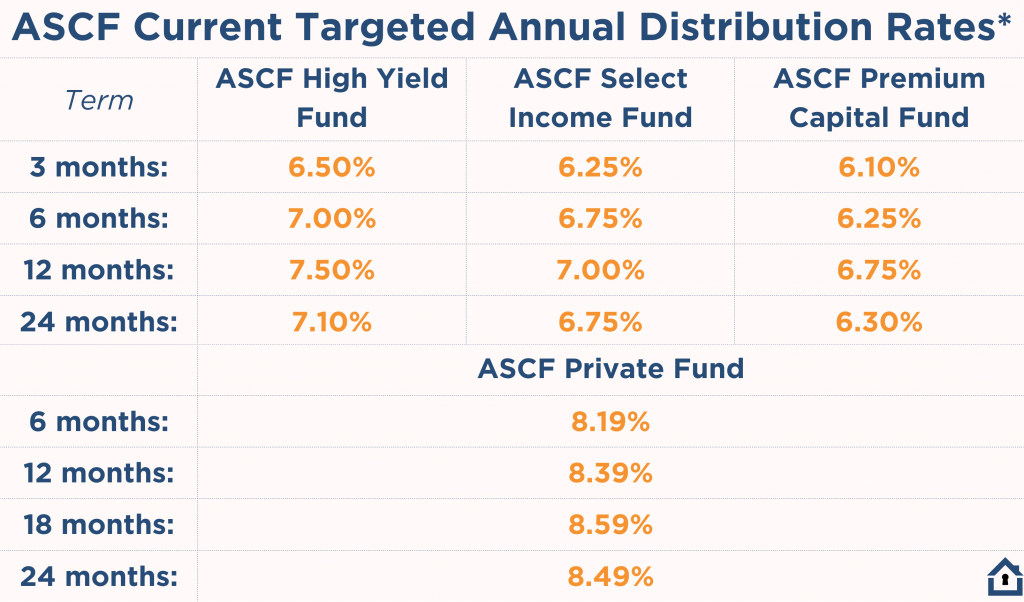

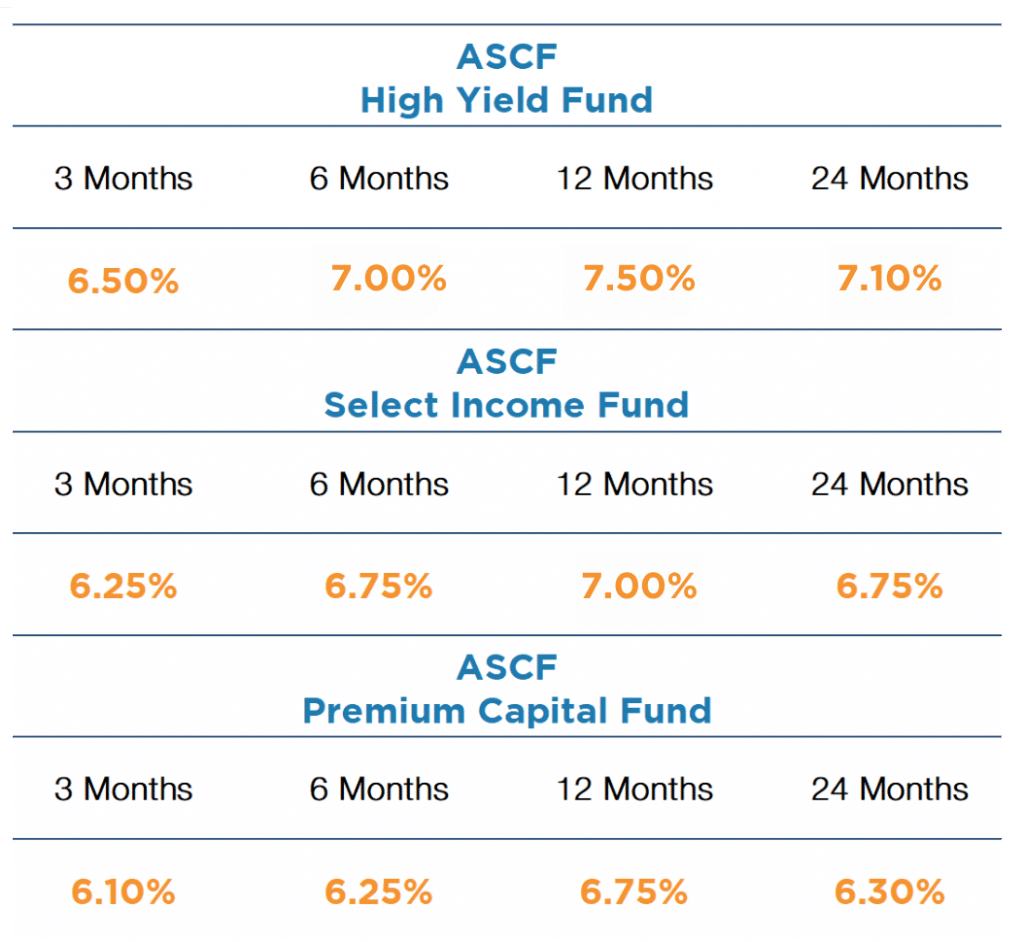

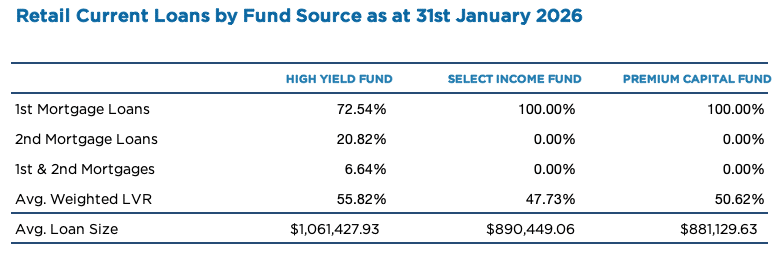

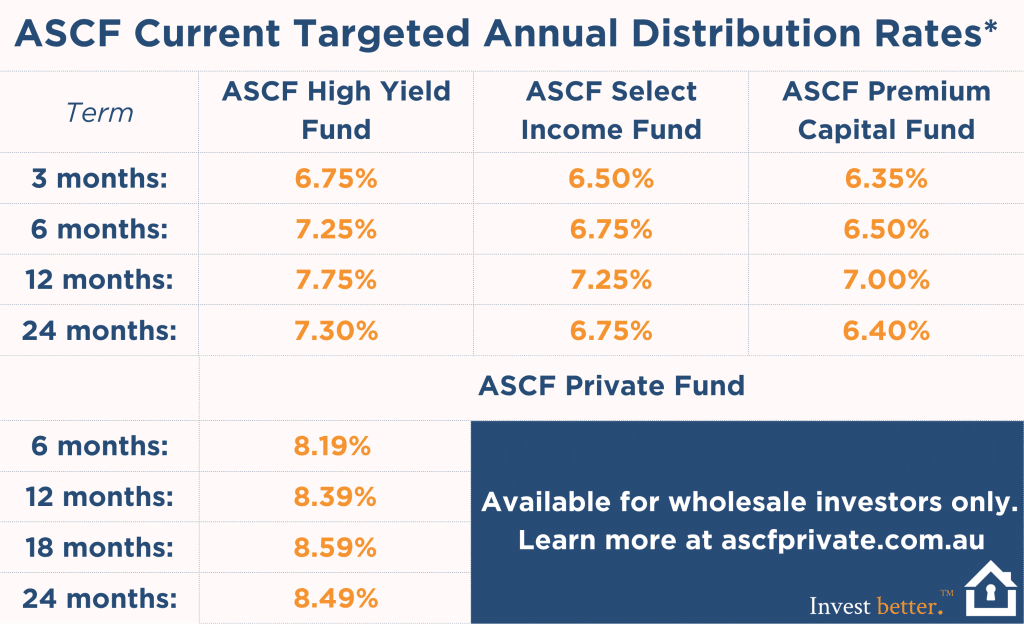

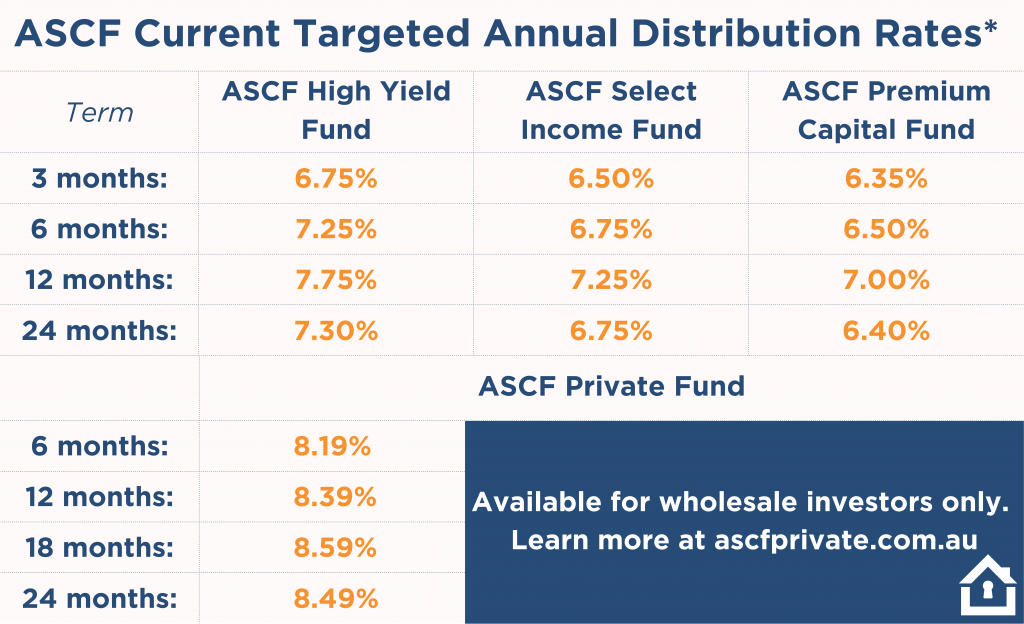

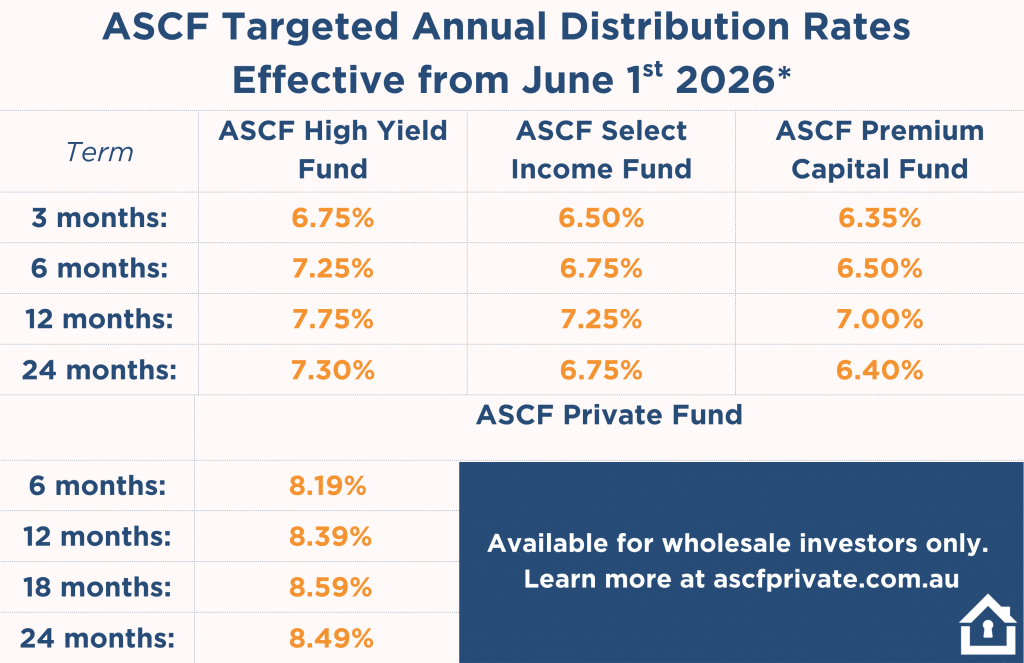

Despite shifting RBA forecasts and rising inflation, ASCF’s funds provide an appealing alternative to fluctuating variable-rate assets. Our ASCF High Yield Fund offers a targeted distribution rate of 7.75% per annum for a 12-month fixed term, with interest paid monthly, and is worth considering as part of any diversified investment portfolio.*

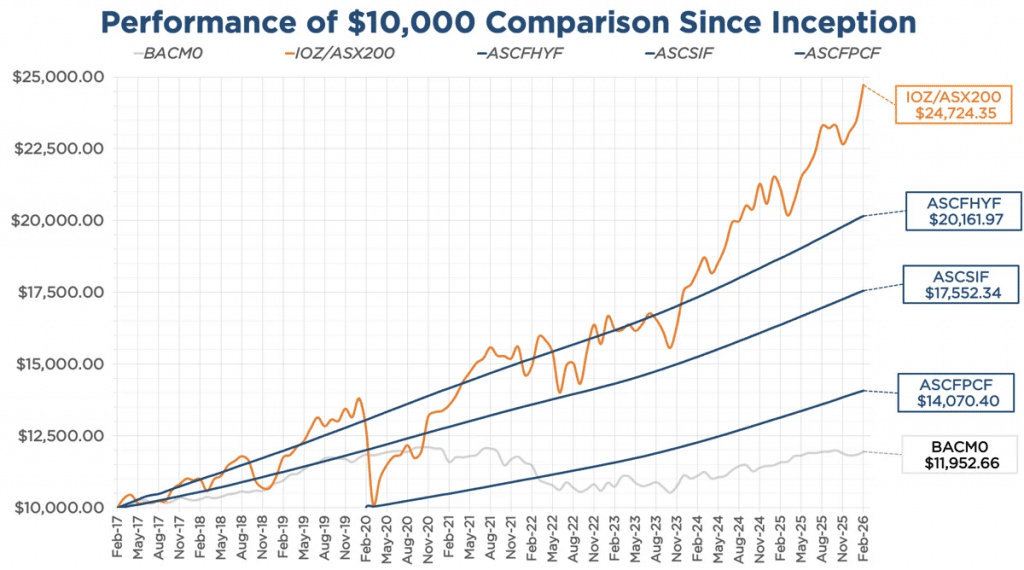

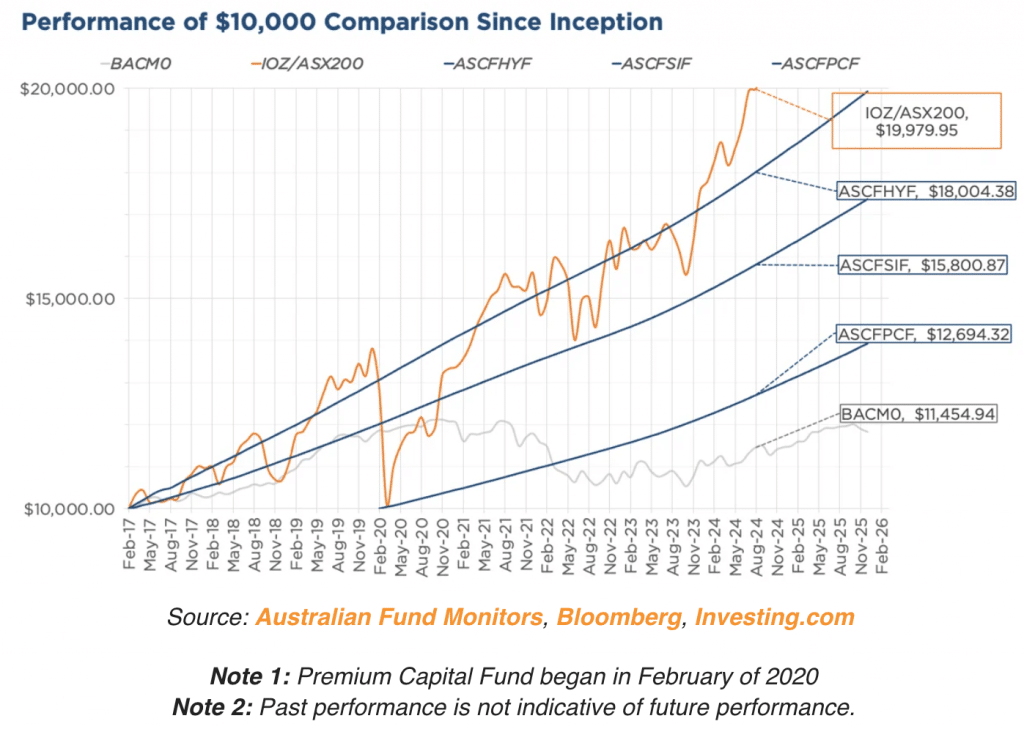

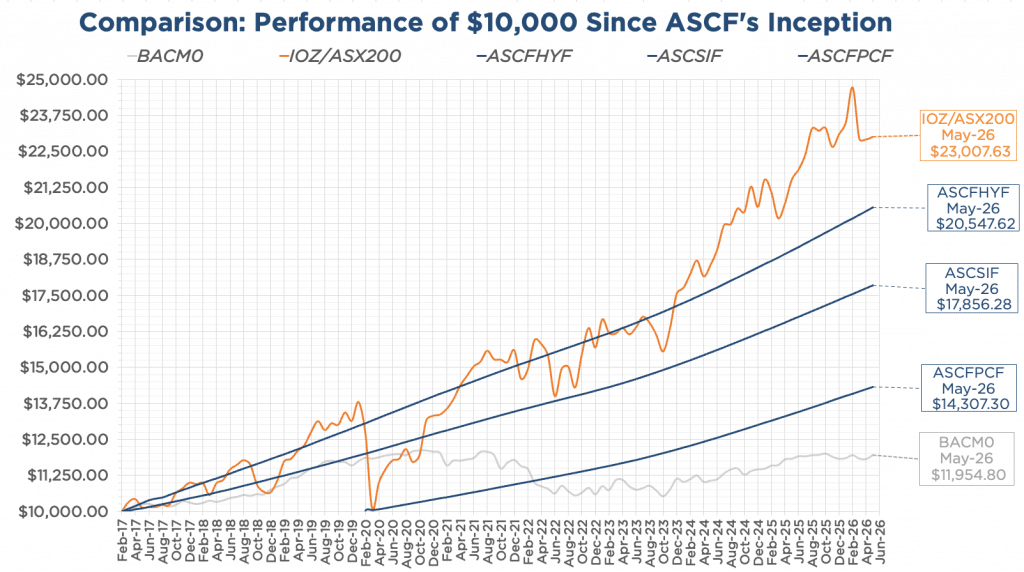

Sources: Australian Fund Monitors, Bloomberg, Investing.com

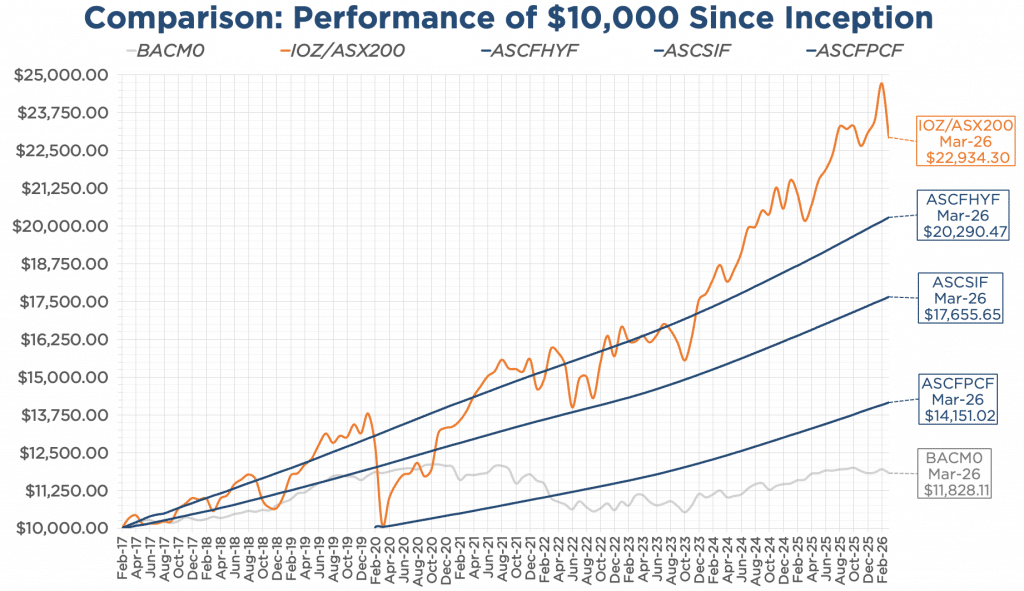

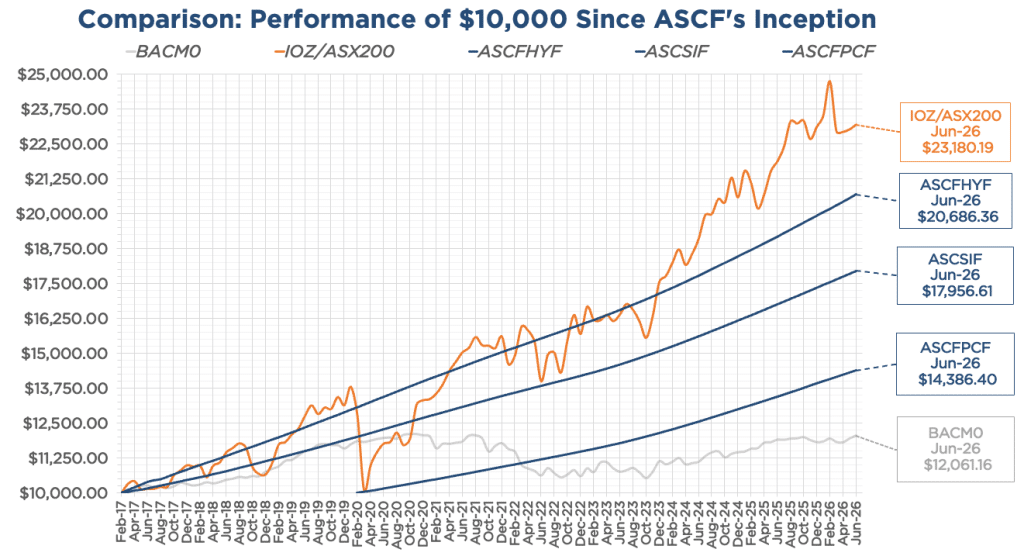

Note 1: Premium Capital Fund began in February of 2020

Note 2: Past performance is not indicative of future performance.

To learn more, see our Investor FAQs.

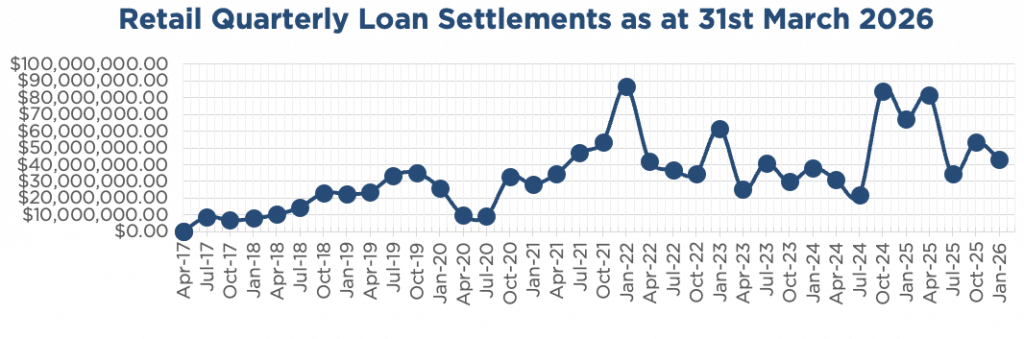

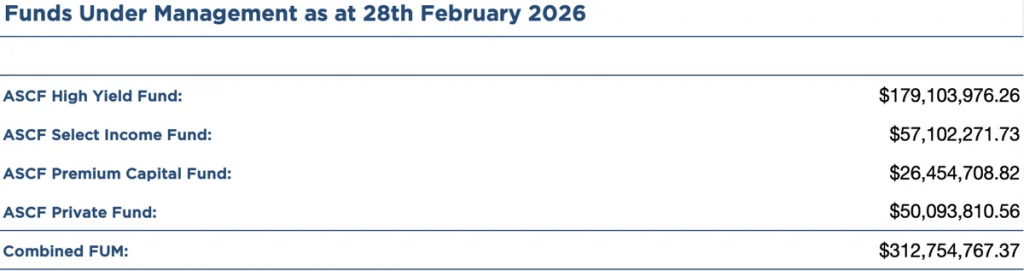

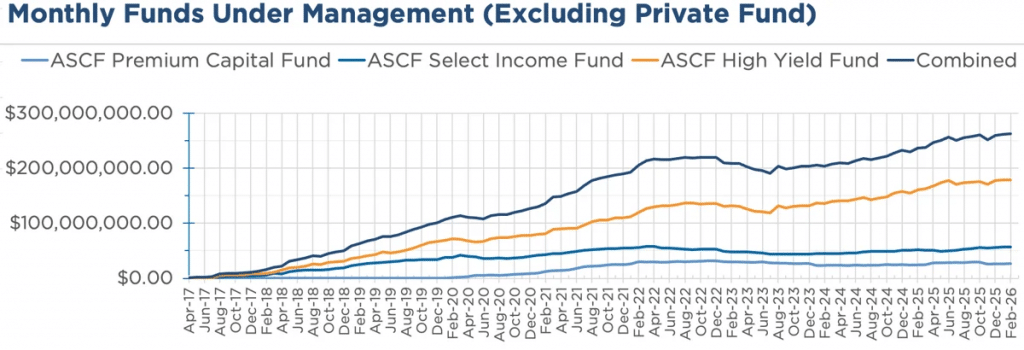

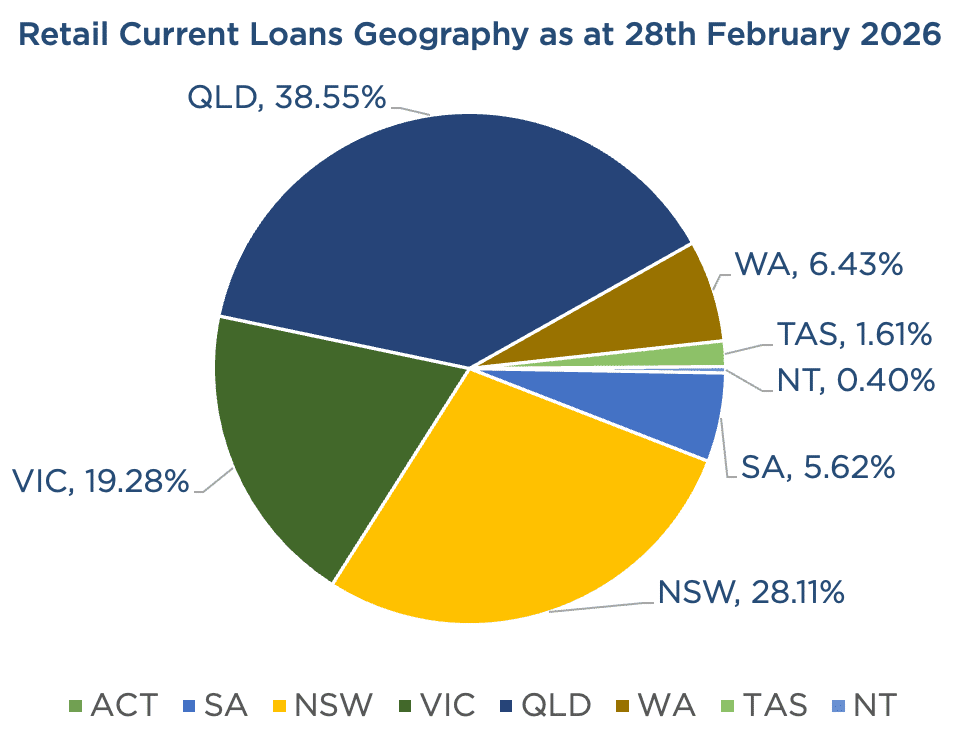

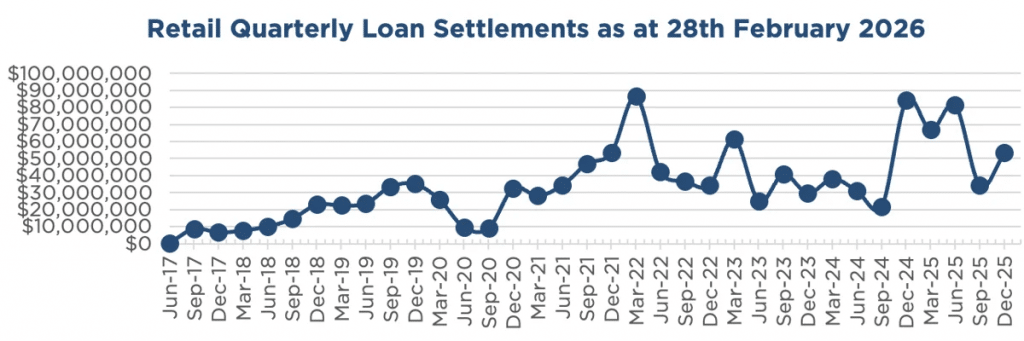

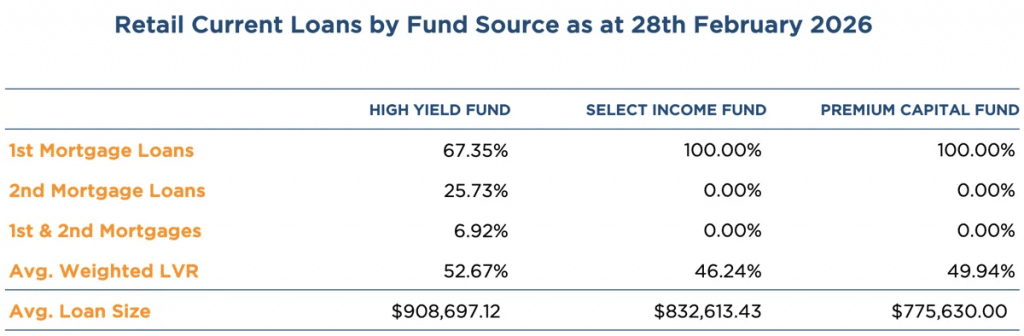

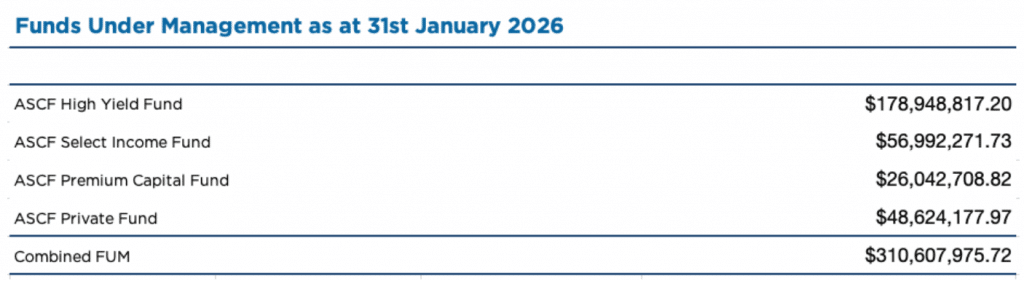

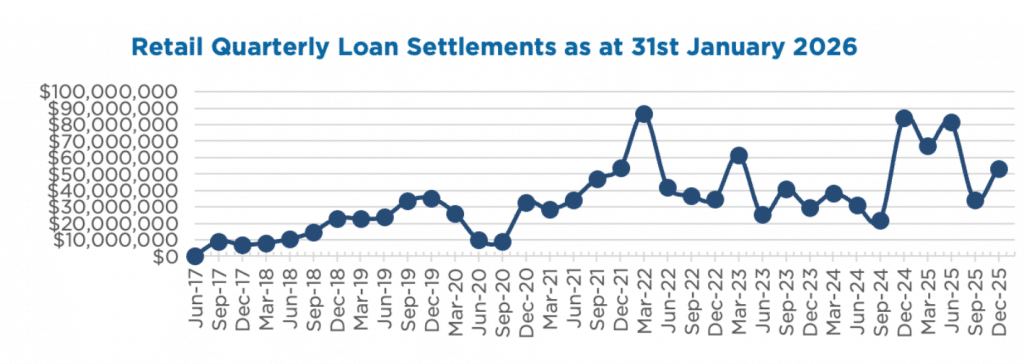

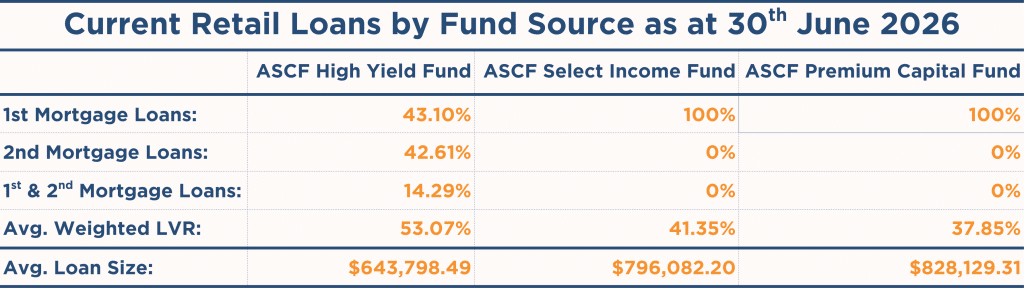

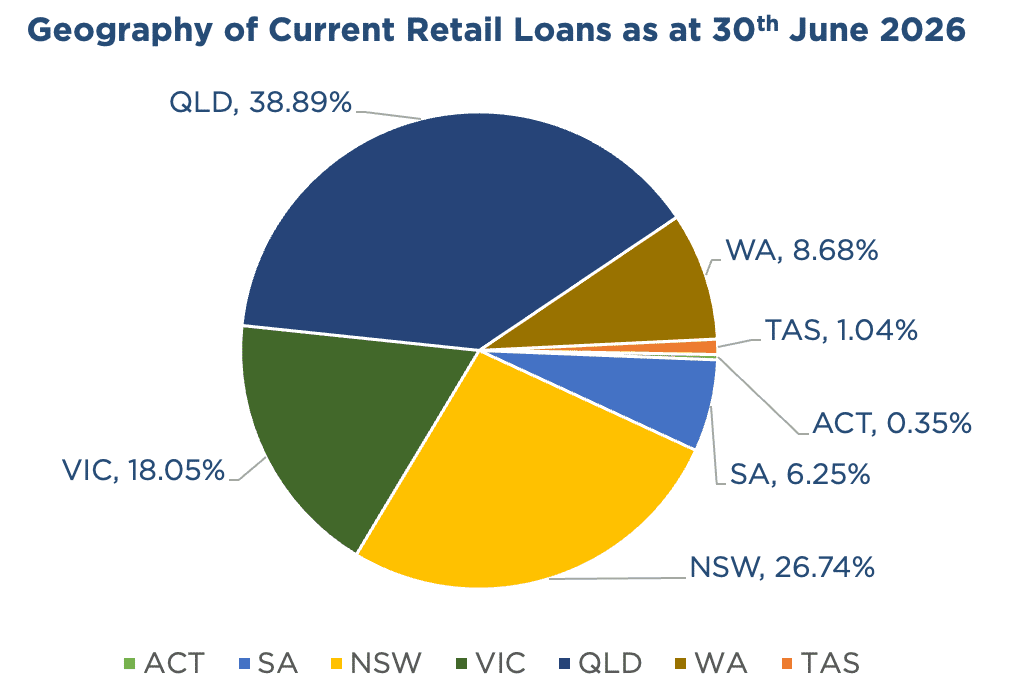

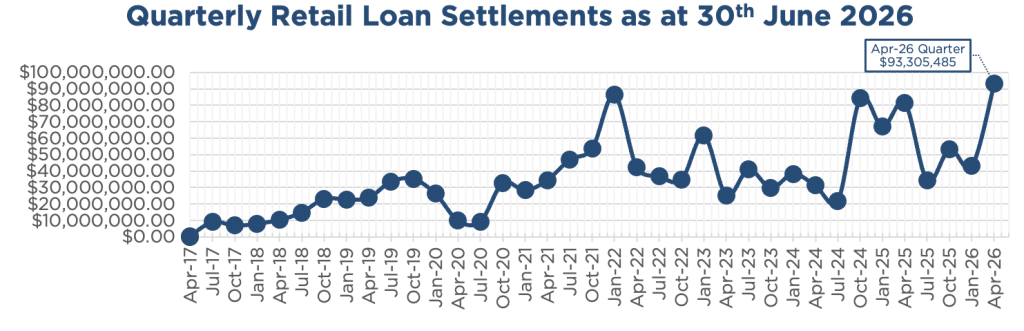

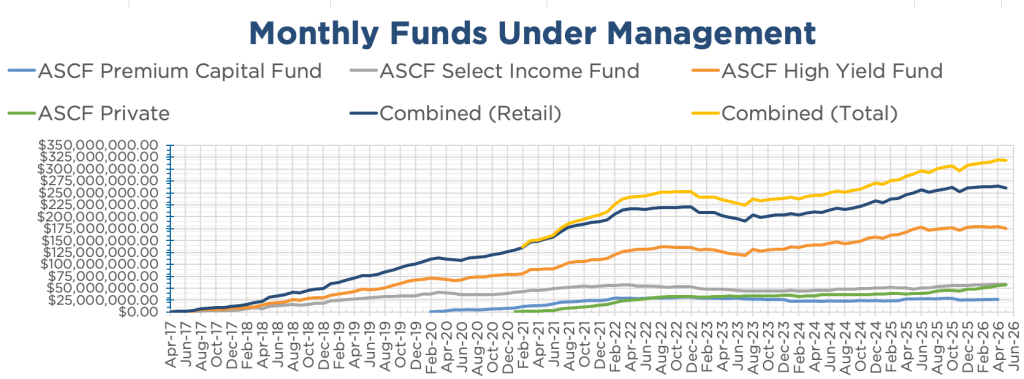

Lending Activity Update

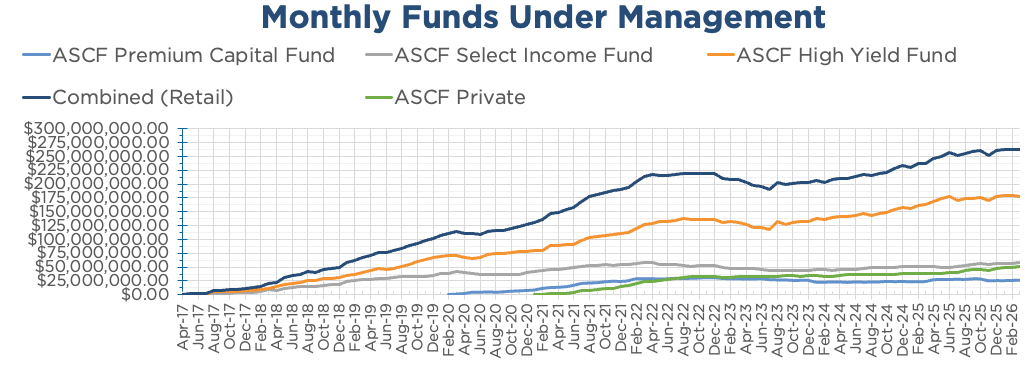

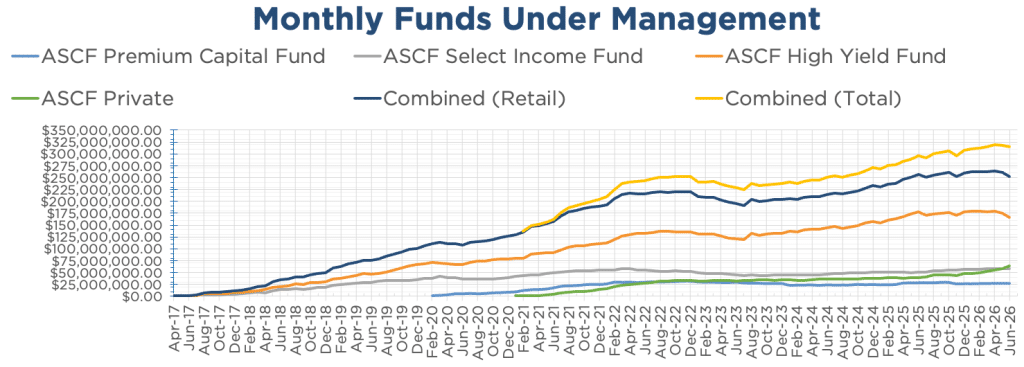

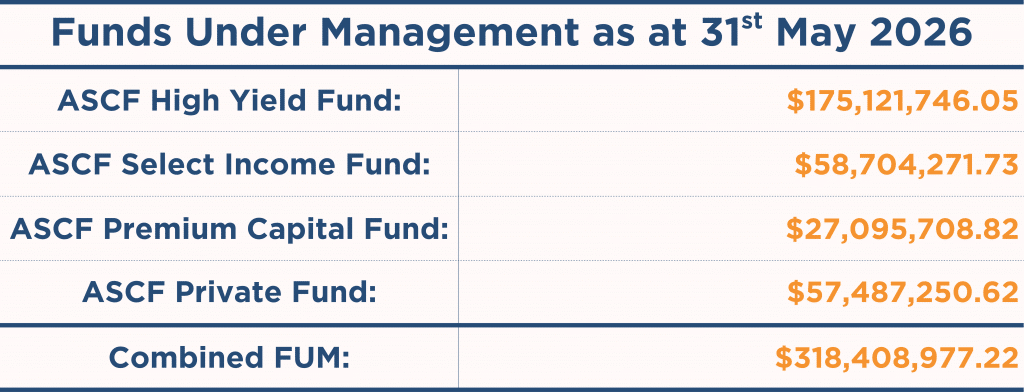

In June, inquiry levels were strong, with $23,778,899.47 in loans settled.

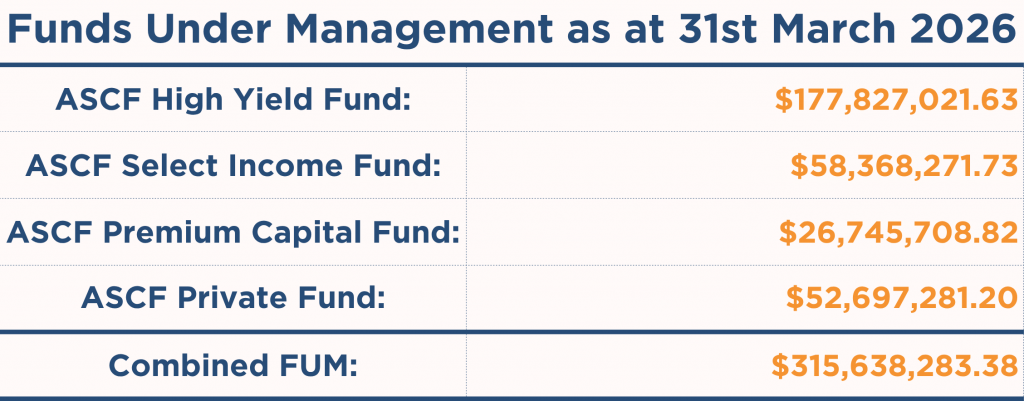

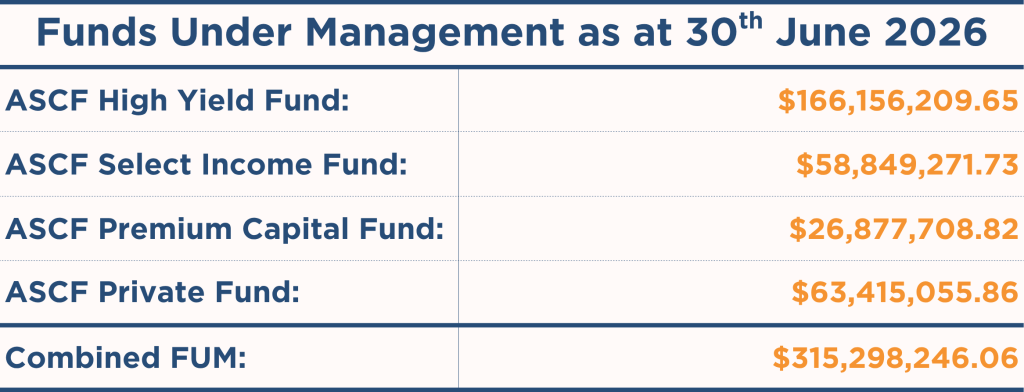

The unit price across all three of our retail funds remains at $1.00 per unit, and all monthly distributions have been paid in full for June.

To learn more, see our Borrower FAQs or visit our Loan Summary as at 30th June 2026.

Why Risk Controls Are Important in an Inflationary Environment

Recently, inflation has been a major topic of discussion with a number of our investors. Rising living costs, higher fuel prices, and RBA interest rate increases have understandably led some investors to question whether these factors create additional risks within a mortgage fund portfolio.

Economic conditions inevitably fluctuate over time, making it important to recognise that these types of risks are not unique to periods of higher inflation. Every lending environment presents distinct challenges, whether it be rising interest rates, falling interest rates, changing property values, economic slowdowns, or shifts in borrower confidence.

While these risks are present, it is important to assess how they are managed on a day-to-day basis when determining whether an investment aligns with your risk profile.

Loan Assessment

At ASCF, risk management begins long before a loan is settled. Specifically, each lending opportunity undergoes a thorough assessment process to help structure loans appropriately from the outset.

Portfolio Management

Once a loan is advanced, the focus shifts to ongoing portfolio management. Among other things, this means that mortgage repayments are actively monitored, and our team maintains regular oversight of the loan book to identify potential issues at an early stage. Applying this process wherever possible means we work collaboratively with the borrower to proactively work towards solutions before minor issues can potentially develop into more significant concerns.

Diversification

Each fund’s investments are pooled across a broad range of borrowers and property securities rather than being concentrated in a small number of loans. This diversification helps mitigate the impact that any single loan may have on the overall portfolio.

Strategic Measures

Additionally, strategic measures, such as reducing the maximum loan exposure to any given mortgage and lowering the average LVR across each fund, are intended to provide additional capacity when managing repayment issues or recovery timeframes.

In periods of higher inflation, some borrowers may experience increased financial pressure. However, this is why active loan management, established lending parameters, and ongoing monitoring are crucial. These principles are not solely implemented during difficult economic periods—they form a core part of our lending philosophy throughout all stages of the economic cycle.

Economic conditions will continue to change, as they always have. However, at ASCF, our focus remains on what we can control: prudent lending, active management of mortgage repayments, and maintaining a diversified portfolio with the aim of generating monthly income distributions.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly, and all redemption requests have been paid on time and in full. However, past performance is not indicative of future performance. Distributions are not guaranteed, nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit, and investors risk losing some or all of their capital. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

An AFG broker approached ASCF with a client who had substantial arrears across their commercial facilities, as well as ATO debts. Their goal was to consolidate all of their lending facilities with their current lender so that they could refinance with another major bank.

The borrower’s businesses were running profitably, but they were unable to clear their arrears and pay out the ATO debts without significantly impacting operational cash flow.

Solution:

With full valuations across all securities, ASCF was able to take a 2nd mortgage across three commercial properties and the borrower’s principal place of residence. Because there was sufficient equity in the properties to pay out all of the arrears and ATO debt, ASCF provided a 6-month, 2nd mortgage loan of $1,400,000 at an LVR of 71.28% at 14.25% p.a., which the borrowers repaid in full within 4 months via refinancing.

The ASCF Advantage:

By recognising the benefit that a 2nd mortgage would provide to the borrower and their businesses, ASCF was able to solve a problem that traditional lenders often cannot.

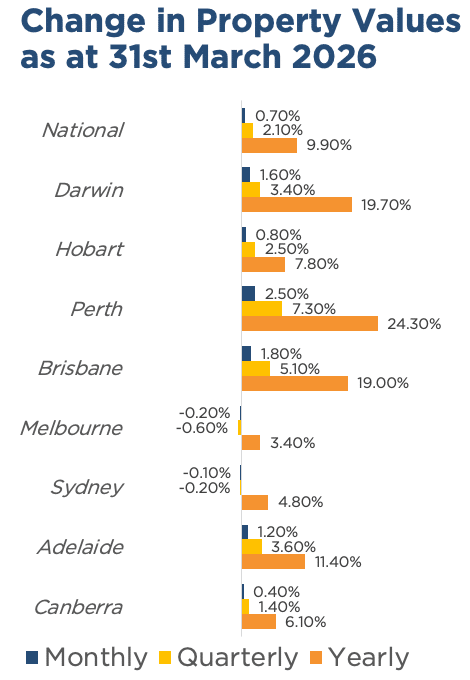

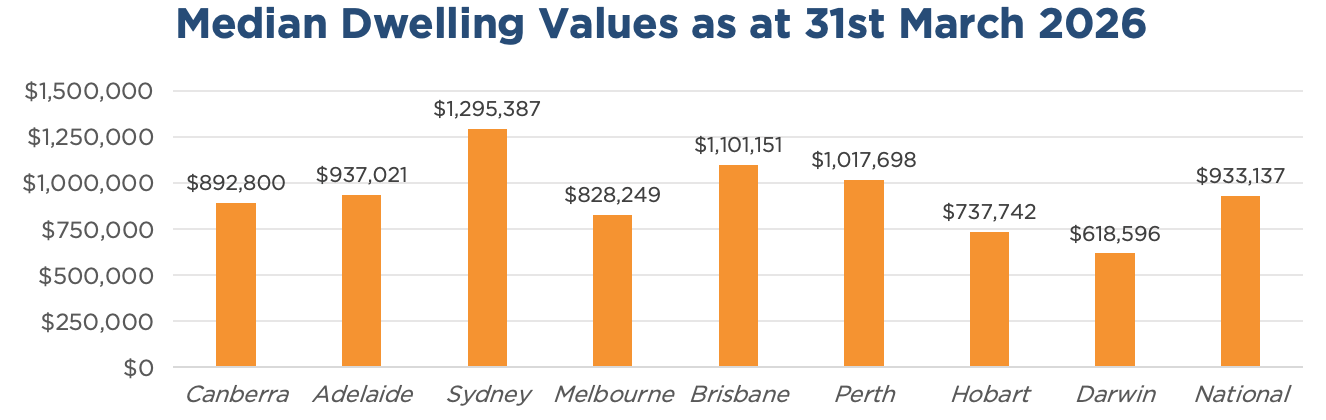

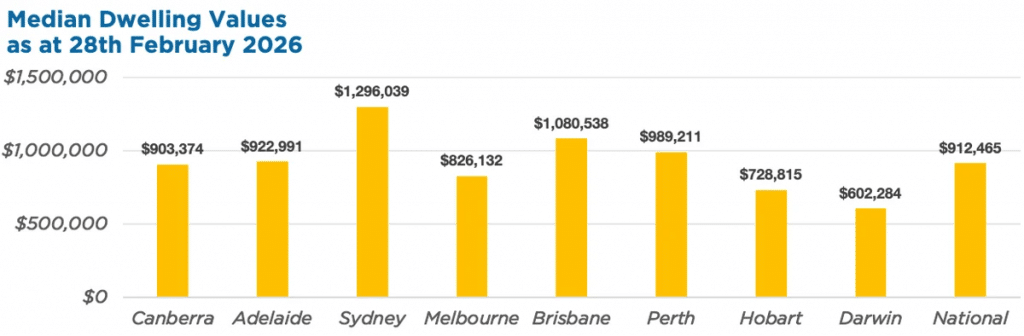

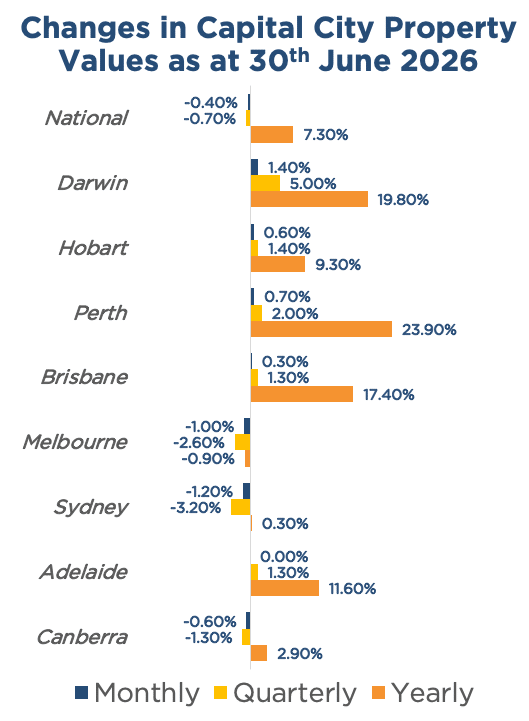

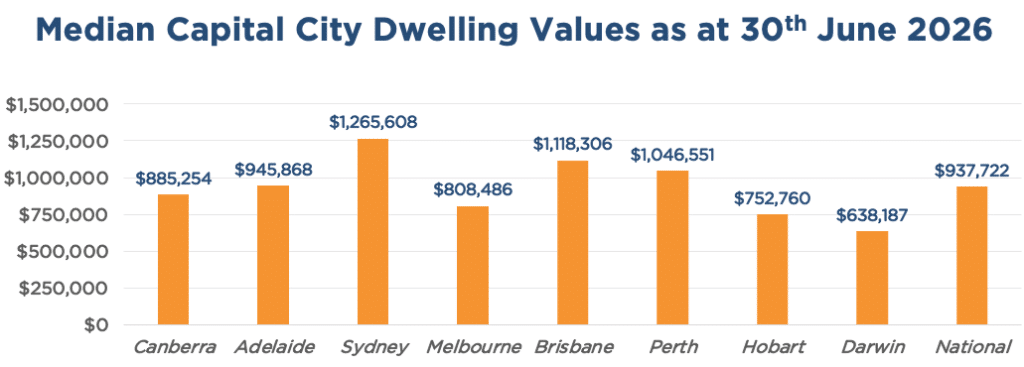

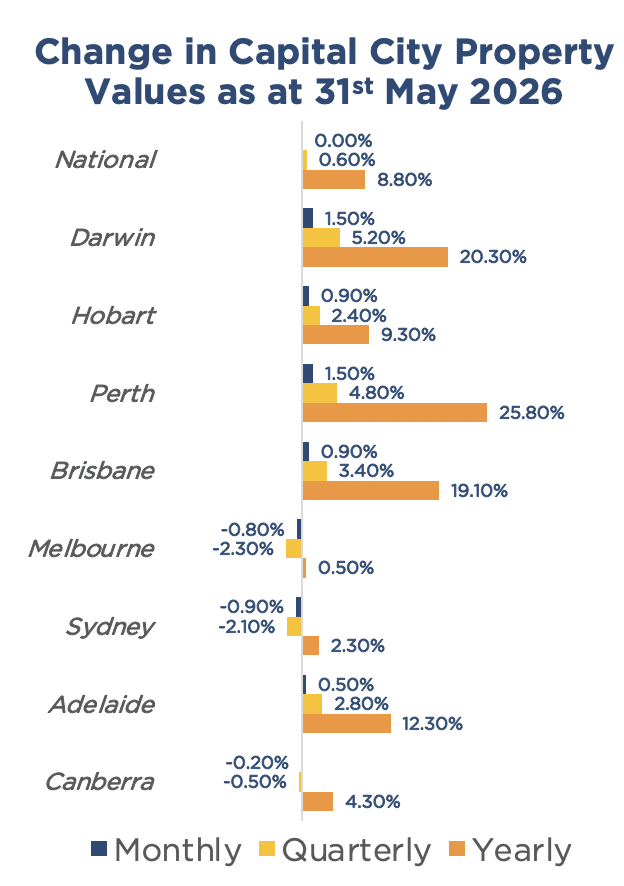

Property Update

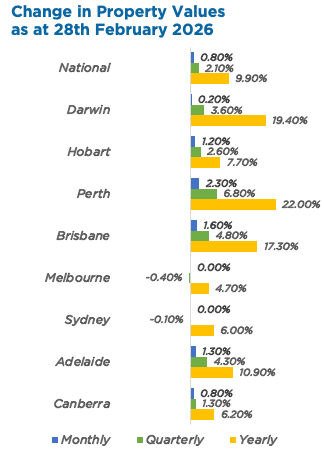

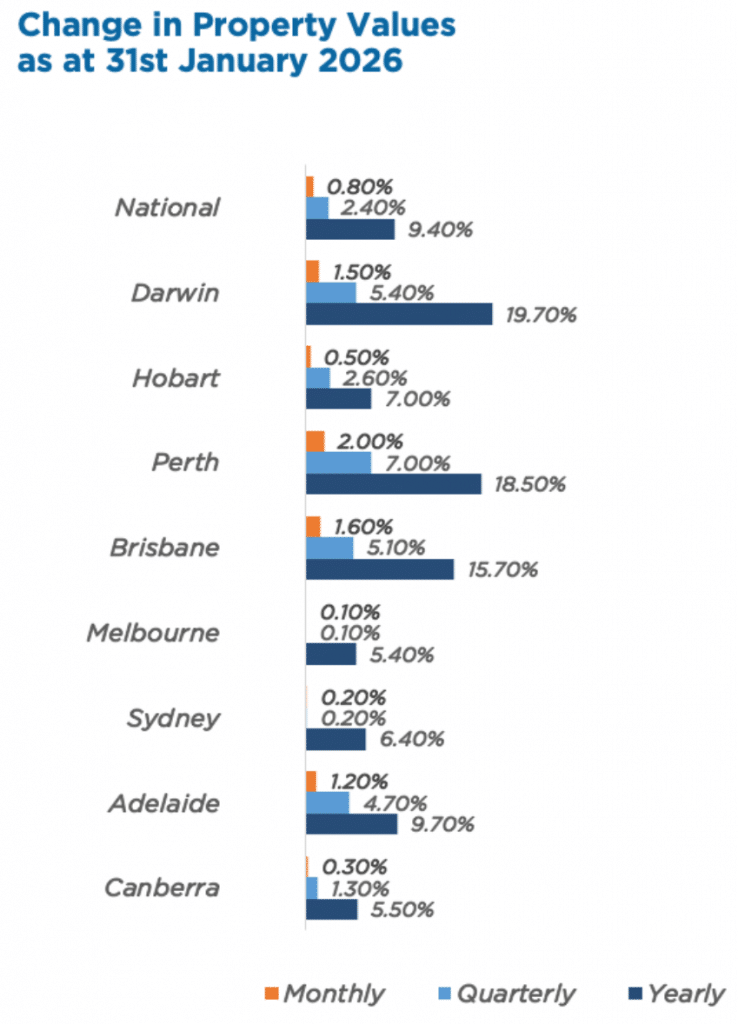

June was a slower month for Australian property values, posting a -0.4% decline. This constitutes the largest month-on-month fall in Australian property values since December 2022, when they declined by -1.1%, and the first month-on-month decline since December 2024.

Sydney continues to lead the slide, posting a -1.2% monthly decline, with values in Melbourne (-1.0%) and Canberra (-0.6%) also going backwards and Adelaide (0.0%) remaining flat. Even so, the market remains somewhat two-speed, with values in Darwin (+1.5%) increasing by more than 1% for the fourth consecutive month. Perth (+0.7%), Hobart (+0.6%), and Brisbane (+0.3%) also added value in June, though at a slower rate than in Q1.

As a result, capital city home sales over the three months to June are approximately 16.2% lower than at the equivalent time last year, while advertised supply across the capital cities is 11% higher than at this point last year.

Source: Cotality HVI, 01 June 2026

.png?width=1200&upscale=true&name=Newsletter%20Stats%20Graphics%202026%20(2).png)

.png?width=1200&upscale=true&name=Newsletter%20Stats%20Graphics%202026%20(3).png)