Trading Update

As expected, the RBA cut rates this month by 0.25% to 4.1%, with all the major banks passing on the rate cut in full.

Employment remains steady, with the jobless rate increasing slightly from 4% in December to 4.1% in January, while wage growth remained subdued, recording a modest 0.7% increase for the December quarter.

Core inflation is expected to ease further this quarter, from 3.2% in the December quarter to below 3%, leaving the burning question of how deep the RBA will cut rates in 2025.

With wage growth likely to return to historical averages of around 2.4% over the medium term, after peaking at 4.2% in 2023, this should provide the confidence the RBA needs to continue lowering rates.

Most economists expect the RBA to reduce rates by a further 0.25% by May, with the possibility of an earlier cut in April. Overall, rates are now expected to fall from their peak of 4.35% to 3.6% by year-end, a total decline of 0.75% from the peak.

Further rate cuts will be data-dependent, though some analysts are debating what the RBA’s neutral rate should be, particularly given pre-pandemic estimates placed it at around 2%.

Consumer confidence is likely to lift as interest rates come down, and residential property prices are expected to remain buoyant throughout 2025. Any downturn is likely to be shallow, with transaction volumes increasing.

While the RBA cash rate has dropped, our term investment rates remain unchanged, meaning investors considering one of our pooled fund investments may wish to act now to secure the targeted rates currently on offer.

Our ASCF High Yield Fund is currently paying a targeted distribution rate of 7.75% per annum on a 12-month fixed-term investment, meaning your targeted rate of return will not change during the investment term, with interest paid monthly.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Monthly Managed Fund Cumulative Growth & Performance

Managed Funds Under Management

as at 31st of January 2025

| January 2025 | |

|---|---|

| ASCF High Yield Fund | $155,184,275.33 |

| ASCF Select Income Fund | $50,828,275.22 |

| ASCF Premium Capital Fund | $23,845,523.53 |

| ASCF Private fund | $38,491,638.50 |

| Combined Funds under Management | $268,350,187.58 |

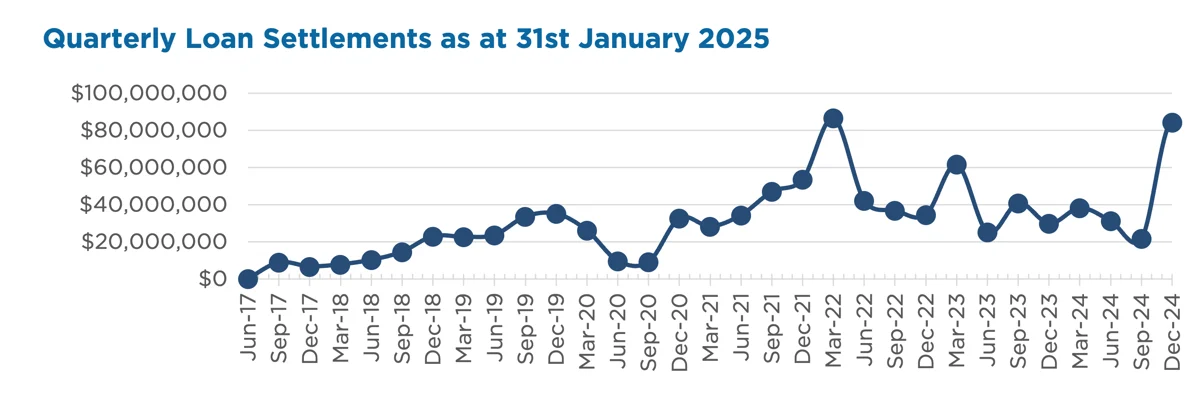

In January, loans and inquiry levels were steady, with $10,572,500.00 in new loans settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of January.

Lending Activity Update

Quarterly Loan Settlements

as at 31st of January 2025

Current Loans by Fund Source

as at 31st of January 2025

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 76.07% | 100% | 100% |

| 2nd Mortgage Loans | 19.28% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 4.65% | 0% | 0% |

| Avg. Weighted LVR | 53.35% | 44.75% | 46.35% |

| Avg. Loan Size | $1,209,454.44 | $927,961.00 | $875,827.53 |

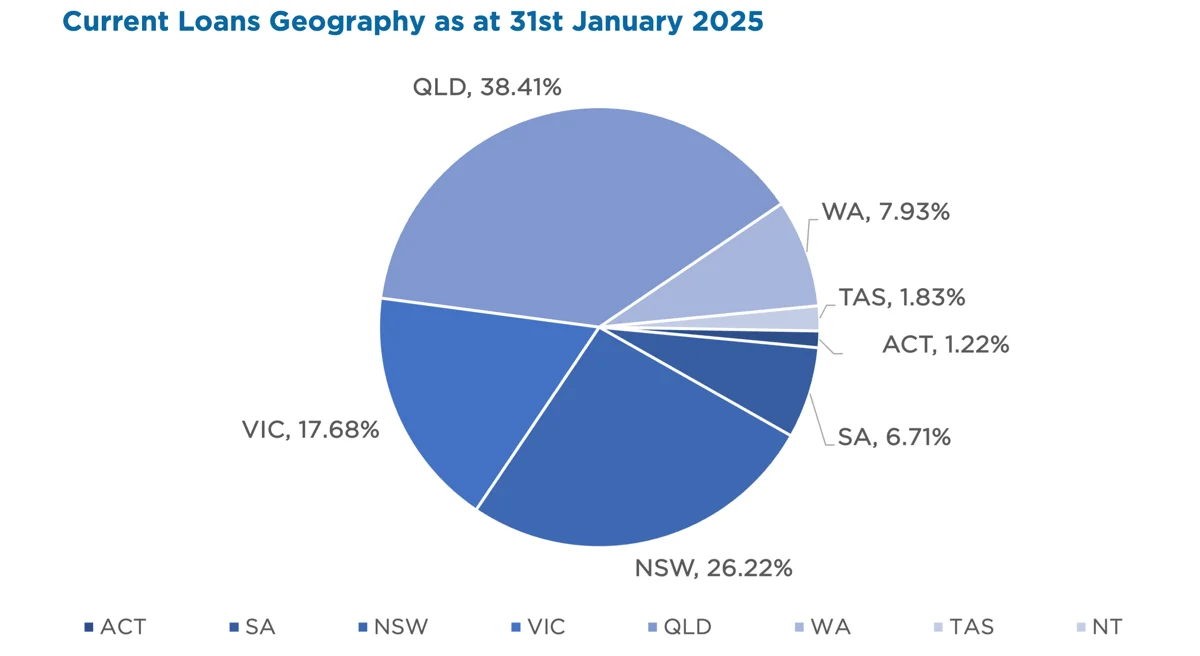

Current Loans Geography

as at 31st of January 2025

Why Invest with ASCF?

Maximise your investment potential with mortgage funds in 2025

Why Consider a Set-Rate Pooled Mortgage Fund?

With the RBA having now cut rates, it’s worth considering how set-rate investments compare to variable-rate options in a changing market.

Mortgage funds can provide a structured investment approach, but choosing between a set-rate pooled mortgage fund and a variable-rate investment can affect financial outcomes.

A set-rate pooled mortgage fund provides a fixed rate for the agreed term, offering more consistency than variable-rate products, which may fluctuate with market conditions.

Key Features of a Set-Rate Pooled Mortgage Fund:

✔ Fixed rate for stability – Your rate is set for the agreed term, providing clarity on expected earnings.*

✔ Less exposure to rate changes – Variable-rate investments fluctuate with interest rates, while set-rate funds are designed for consistency during the term.

✔ Predictable cash flow – Can be beneficial for investors seeking more certainty over their investment timeframe.

ASCF’s set-rate investment options are available for 3, 6, 12, or 24-month terms, designed to provide stability over the agreed period, subject to fund performance. Like all investments, mortgage funds carry risks that should be considered alongside potential benefits.

Want to learn more? Contact us to explore your investment options.

Important information: At ASCF, we’re here to help you invest on your terms. Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A valued AFG broker contacted ASCF seeking urgent funding for a client who needed to meet the settlement date for land purchased off the plan 12 months ago. The client believed he had finance approved, but his lender required several weeks to review the approval and finalise the transaction. With only seven days left to settle, the client risked losing his deposit and missing out on the valuation uplift of the land lot.

Solution:

The broker acted swiftly and provided ASCF with all the required documentation the very next day. ASCF issued a letter of offer that same day, which the borrower promptly executed, allowing us to order documents immediately. Given that the funds were for purchasing property under a company name and the borrower was experienced, ASCF agreed to waive legal advice.

The customer signed electronically via video link (acceptable in QLD, Victoria, and New South Wales) on the same day as settlement.

To facilitate the loan, the customer provided an existing unencumbered property in the company name. This allowed ASCF to rely on the contract price of the purchased land and a desktop valuation of the additional property, confirming an LVR of 48.55%.

ASCF provided a six-month loan of $385,000 at 10.26% p.a., enabling the customer to complete settlement on his property in Branyan instead of forfeiting his deposit and the valuation uplift.

What ASCF does differently

| ASCF specialises in urgent funding for a wide range of purposes. We have developed systems, procedures, and a strong network of partners to facilitate short-term loans efficiently while safeguarding our investors’ interests. |

Market Update

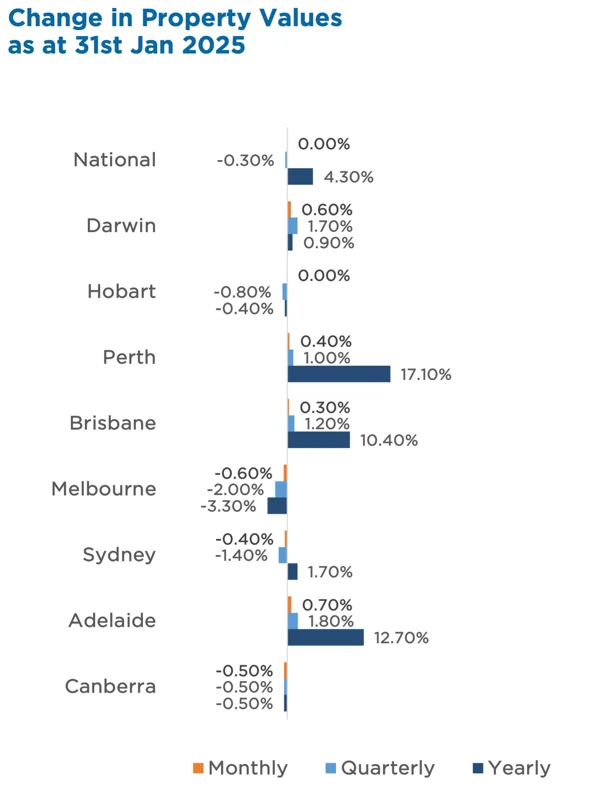

National home values remained steady in January, with capital cities dragging down the overall result. In contrast, regional markets hit new record highs, rising 0.4% – a key trend for investors looking at market resilience.

Melbourne (-0.6%), the ACT (-0.5%), and Sydney (-0.4%) led declines, while Brisbane and Perth maintained growth, though momentum is clearly slowing.

Adelaide continued its strong performance, leading capital city gains with 4.8% growth over the past six months. Perth, once the fastest-growing market, has cooled significantly, with growth slowing from 7.1% in mid-2024 to just 1.0% over the past three months.

Despite this, regional markets remain a bright spot, benefitting from migration trends, affordability, and evolving work patterns. While growth has softened, regional areas have consistently outperformed the capitals.

With the RBA’s recent rate cut, borrowing power may improve, but affordability constraints, slowing population growth, and housing supply shortages remain challenges. For investors, the outlook remains stable, with conditions pointing to measured market adjustments.

Property Values

as at 31st of January 2025

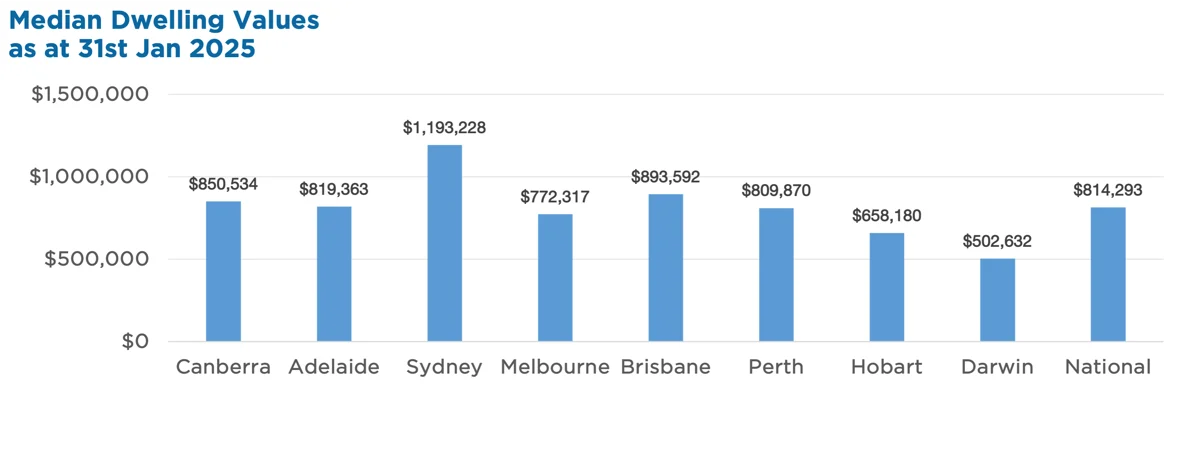

Median Dwelling Values

as at 31st of January 2025

Quick Insights

How the rate cut is shifting the market

The latest rate cut is already reshaping buyer demand, unlocking new suburbs and boosting auction results. But how long will this momentum last?

Source: Australian Financial Review

What’s shaking up the housing market in 2025? Rate relief: RBA cuts the cash rate by 25 basis points

After the most aggressive rate hiking cycle on record, the RBA has reduced the cash rate from a thirteen-year high of 4.35% to 4.1%.

Source: Corelogic