Trading Update

As we wrap up 2024, the Australian economy shows signs of progress but remains delicately balanced. Inflation is easing, growth is slowing, and the labour market remains steady – all key factors shaping the financial landscape as we head into 2025.

The RBA maintained the cash rate at 4.35% last week and while headline inflation has fallen sharply, underlying inflation remains elevated at 3.5%, indicating persistent price pressures. GDP growth continues to be slow, registering only 0.3% for the September quarter, and the December quarter is expected to be similar or even lower.

Economic growth remains subdued, with household spending recovering more slowly than expected. However, the labour market continues to show resilience, with unemployment steady at 3.9% and wage growth easing.

We expect the RBA is now likely to lower rates at its next meeting in February by 0.25%, with rates likely to fall by 0.5% to 0.75% by mid 2025. The inflation data for the December quarter, which is set to be released at the end of January, will be crucial in determining the pace of these reductions.

The housing market, which started the year strong, has slowed its pace. While national home values have risen 5.5% over the last 12 months, affordability challenges, cost-of-living pressures, and elevated interest rates are now cooling the momentum. With more properties hitting the market and demand softening, 2025 presents an interesting mix of possibilities. Easing inflation and potential rate cuts is however expected to rejuvenate buyer confidence.

In this evolving environment, ASCF remains committed to offering tailored opportunities to help you achieve your financial goals. For more insights, contact our team today.

As this is our final newsletter for 2024, we want to thank you for being part of our year and wish you a Merry Christmas and Happy New Year.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Monthly Managed Fund Cumulative Growth & Performance

Managed Funds Under Management

as at 30th of November 2024

| November 2024 | |

|---|---|

| ASCF High Yield Fund | $154,411,895.33 |

| ASCF Select Income Fund | $48,875,750.22 |

| ASCF Premium Capital Fund | $24,114,523.53 |

| ASCF Private fund | $37,098,095.33 |

| Combined Funds under Management | $227,402,169.08 |

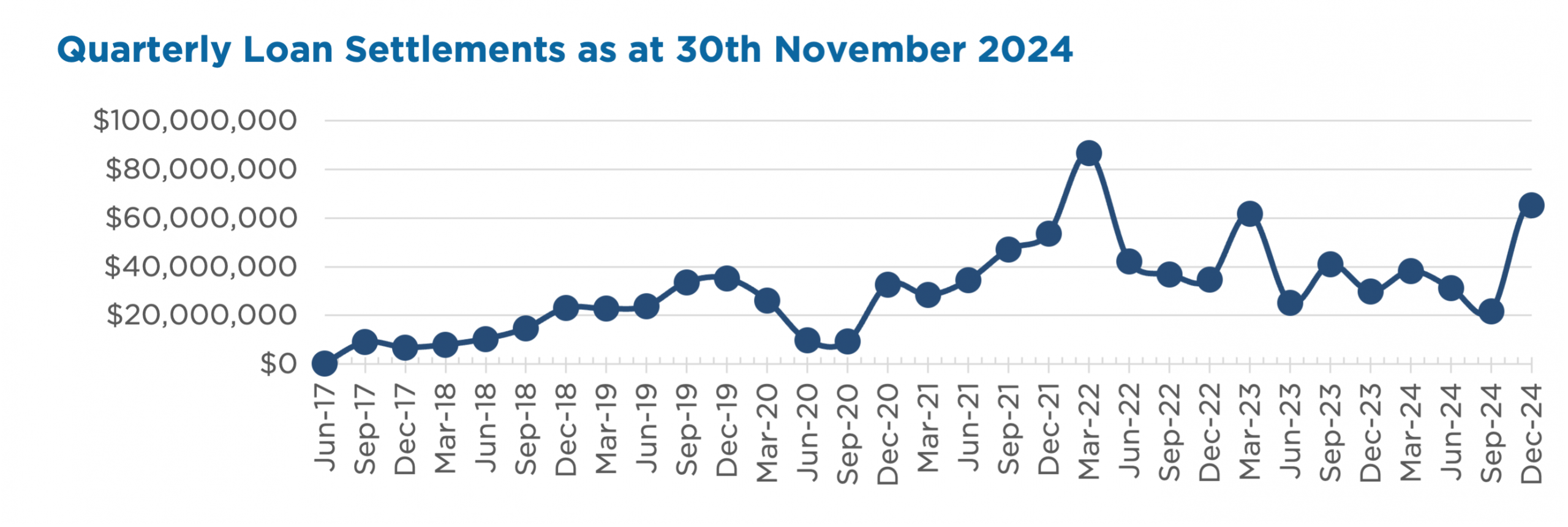

In October, loans and inquiry levels were extremely strong, with $56,653,600.00 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of November.

Lending Activity Update

Quarterly Loan Settlements

as at 30th of November 2024

Current Loans by Fund Source

as at 30th of November 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 78.08% | 100% | 100% |

| 2nd Mortgage Loans | 17.39% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 4.53% | 0% | 0% |

| Avg. Weighted LVR | 50.79% | 40.93% | 45.38% |

| Avg. Loan Size | $1,281,077.93 | $984,595.57 | $935,406.35 |

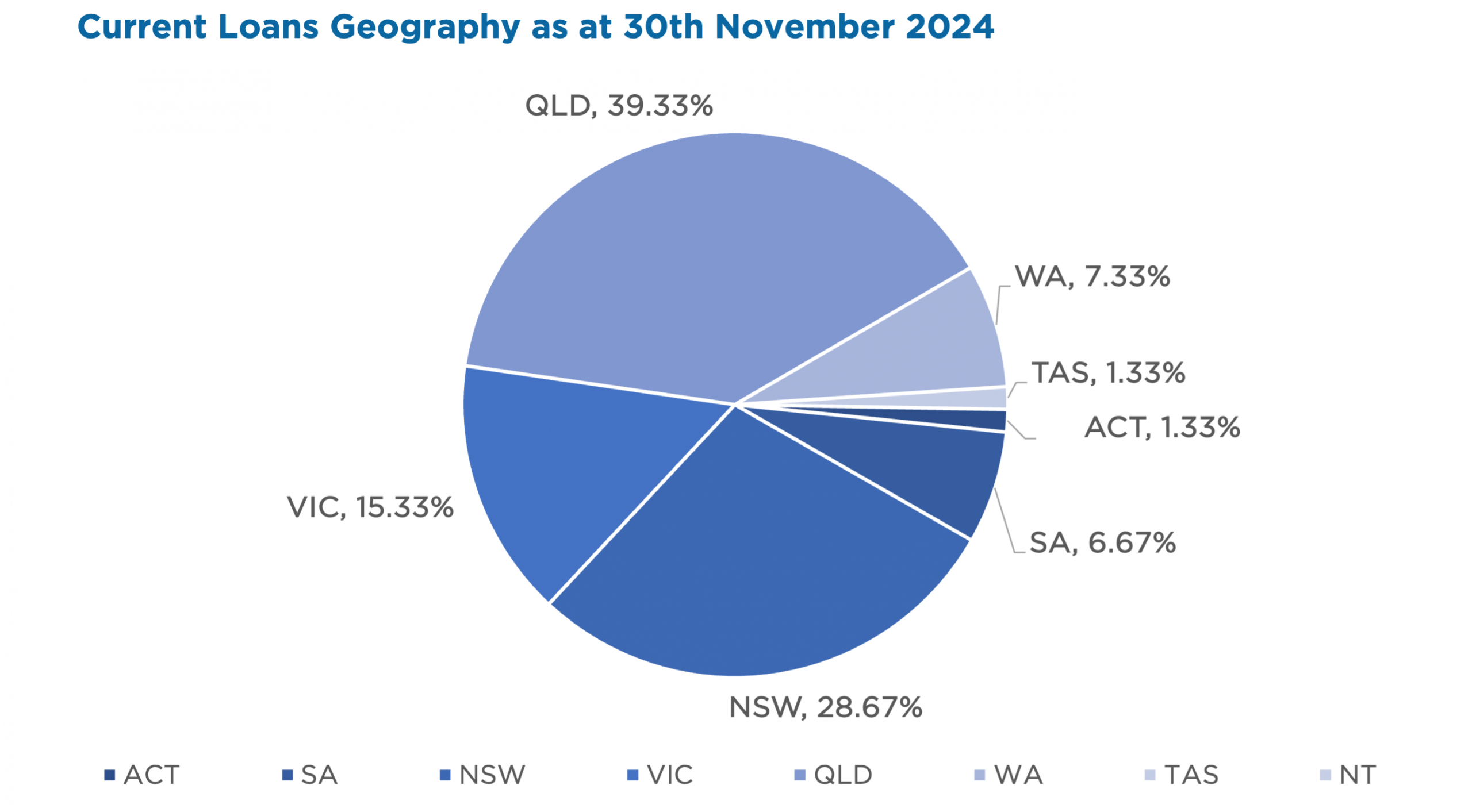

Current Loans Geography

as at 30th of November 2024

Why Invest with ASCF?

Why a pooled mortgage fund might be your perfect investment

Recently, I’ve noticed increased interest from property investors who are either disappointed with their net returns or seeking alternatives to the challenges associated with managing investment properties.

Investing in property can be a pathway to growing wealth, but it comes with significant demands. From large deposits to managing tenants, property ownership requires time, effort, and capital. A pooled mortgage fund offers a streamlined alternative. Here’s why:

Steady and predictable returns

Pooled mortgage funds are designed to deliver consistent returns. Unlike direct property investment, which is influenced by market fluctuations and vacancies, pooled funds diversify risk and aim for stability.

No property management hassles

Rental properties often come with the need to handle tenants, maintenance issues, and management costs. Pooled mortgage funds eliminate these responsibilities, letting you enjoy potential returns without the associated stress.

No large deposit required

Property purchases often require a significant deposit, making them less accessible for many investors. Pooled funds typically allow you to invest with a much lower upfront commitment, offering access to the property market without the need for substantial capital.

Diversified investment risk

Investing in a single property concentrates your risk in one asset. Pooled mortgage funds spread your investment across multiple loans secured by property, helping to reduce the impact of any market downturns.

Improved liquidity

Unlike property, which can take time to sell and may depend on market conditions, pooled mortgage funds often provide greater liquidity, enabling you to access your funds at the end of a specified term.

Professional fund management

ASCF pooled mortgage funds are managed by an experienced team that oversees loan assessments, approvals, and repayments. Their expertise ensures the portfolio is managed prudently, letting you focus on your financial goals.

Investing should be simple, transparent, and effective. Our pooled mortgage funds provide access to the benefits of property-related investments while addressing the challenges associated with direct ownership. If you’d like to learn more, feel free to contact us.

Disclaimer: At ASCF, we’re here to help you invest on your terms. Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A couple from Burpengary, QLD, was struggling under the weight of the escalating cost-of-living crisis. Falling behind on mortgage payments, council rates, and water bills, they had turned to multiple consumer credit providers to supplement their income, which only exacerbated their financial difficulties.

Ultimately, they decided to list their home for sale, aiming to downsize to a more manageable mortgage and achieve a less stressful, sustainable lifestyle.

Solution:

ASCF provided a debt consolidation solution, along with additional funds, enabling the couple to prepare their property for sale and maximise its sale price. This proactive approach prevented their lender from foreclosing and auctioning the property under mortgagee-in-possession conditions. We offered a 5-month term at 11.95% p.a., giving the customer sufficient time to secure a sale and settle the contract. An external valuation confirmed the LVR at 64.10%.

By consolidating all debts, the customer satisfied their credit obligations and ended the harassment from multiple creditors, allowing them to focus on preparing the property for sale. Shortly after our drawdown, the customer secured a buyer, but had to wait 90 days for settlement to complete. This month, the sale settlement was finalised, and ASCF rebated the customer 2 months of retained interest at settlement.

What ASCF does differently

By taking the time to understand what is important to customers, ASCF can structure a financing solution that meets the customers goals and objectives even when that goal is alleviating mental anguish.

Market Update

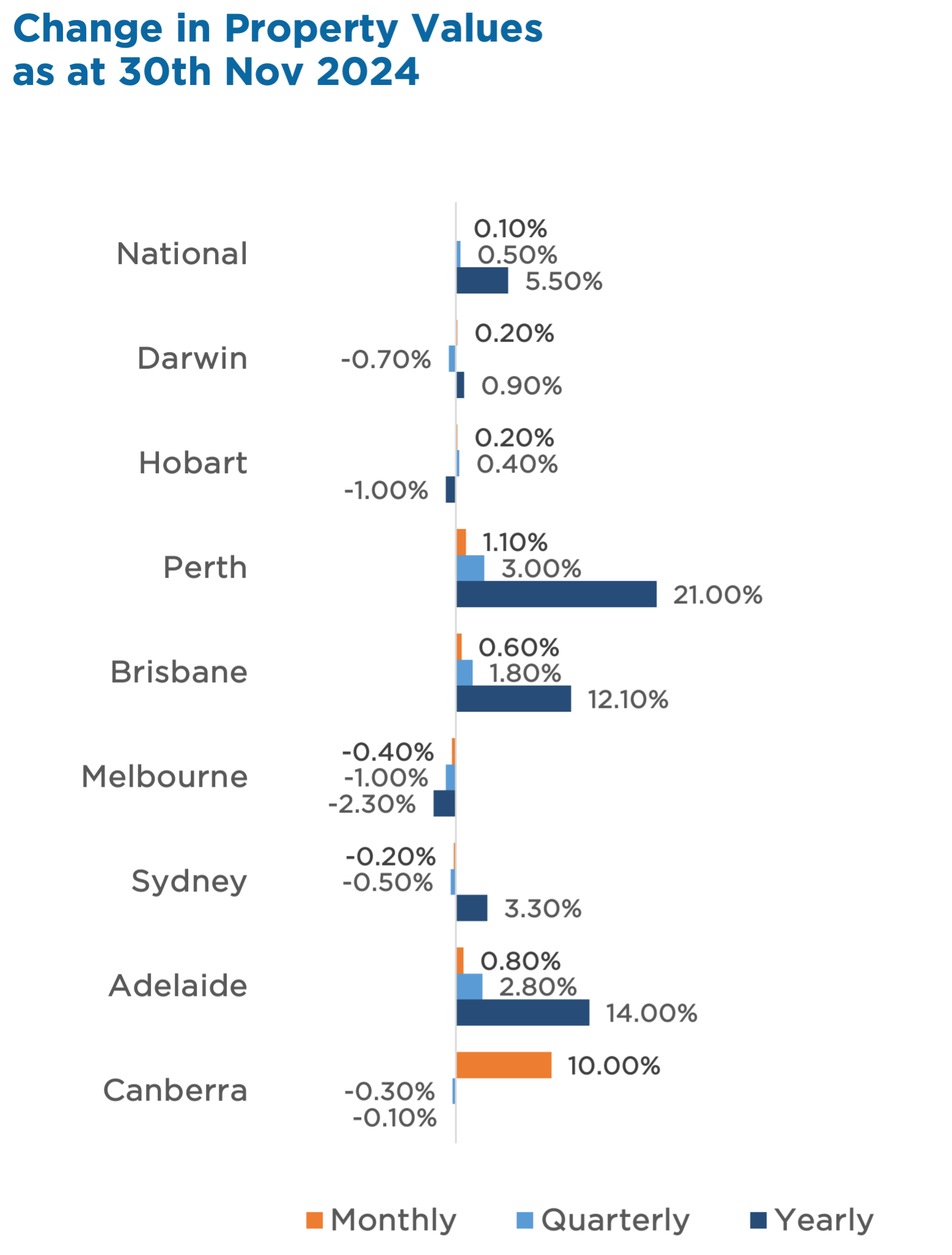

November marked the 22nd consecutive month of growth for CoreLogic’s national Home Value Index, increasing by just 0.1%. This was largely driven by the continued strong performance of Perth, Adelaide and Brisbane, increasing by 1.1%, 0.8% and 0.6% respectively. Darwin and Canberra were the only other capital cities to see growth for the month, increasing by 0.2% and 0.1% respectively, whilst Melbourne, Sydney and Hobart all experienced reductions in property values, of 0.4%, 0.2% and 0.1% respectively.

Whilst monthly data is suggesting that the property market is starting to cool, the annual data remains positive, with all capital cities except for Melbourne (-2.3%), Hobart (-1.0%) and Canberra (-0.1%) achieving growth over the previous 12 months. Perth recorded an astonishing 21% increase over the past 12 months, followed by Adelaide and Brisbane with 14% and 12.1% respectively, whilst Sydney and Darwin also saw growth of 3.3% and 0.9% respectively, resulting in a 5.4% increase across the combined capitals, and a 6.0% increase across the combined regions for the year.

With the RBA opting to once again keep the cash rate on hold, expectations of when the first rate cut may occur continues to drift out. This will likely result in continued weakening of the property market in Melbourne, Sydney and Hobart, whilst the undersupply in Brisbane, Adelaide and Perth may continue to prop up national averages in the early parts of 2025.

Property Values

as at 4th of Nov 2024

Median Dwelling Values

as at 31st of October 2024

Quick Insights

Housing market at a turning point

Australia’s housing market is reaching a turning point, with high borrowing costs and affordability challenges dampening demand. National house prices are expected to decline for the first time in two years, with previously strong markets like Brisbane, Perth, and Adelaide also slowing. Economists anticipate further softening through early 2025, presenting opportunities for buyers as affordability improves.

Source: Australian Financial Review

2024: A year of waning demand, rising supply and waiting for interest rates to fall

In the face of elevated interest rates and global uncertainty, the Australian housing market demonstrated surprising resilience throughout 2024 with the number of home sales increasing 8% on the previous year, according to CoreLogic’s Best of the Best report for 2024.

Source: Corelogic