Trading Update

Investors had plenty to unpack in October, from key economic updates to global market shifts.

Domestically, the Reserve Bank of Australia (RBA) continues its focus on reducing inflation, holding rates steady at 4.35% in November. Inflation for services remains high at 5%, and the RBA is now unlikely to cut rates until early 2025. The December meeting will provide further insights into how the RBA views the economic outlook however at this stage we expect the February meeting of the RBA to be in play in terms of a 0.25% reduction to the official cash rate.

Globally, central banks are easing monetary policies, with rate cuts from the US Federal Reserve and European Central Bank. These changes, alongside the US election, may influence trade, currencies, and markets — factors Australian investors should monitor heading into 2025.

Australia’s labour market remains robust, with unemployment steady at 4.1%. Employment and hours worked increased slightly, reflecting resilience despite rising living costs. Consumer spending held firm, with the CBA Household Spending Insights Index rising 0.8% in October, supported by recreation and household goods.

In the housing market, CoreLogic reported a 0.3% rise in national property values for October, marking 21 consecutive months of growth. However, Sydney and Melbourne recorded slight declines, while Perth and Adelaide led with strong gains.

As 2024 draws to a close, Australia’s “higher for longer” interest rate environment presents both challenges and opportunities. Investors may want to assess how these dynamics align with their strategies for the year ahead.

For more insights on current market trends or ASCF’s investment offerings, reach out to our team today.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

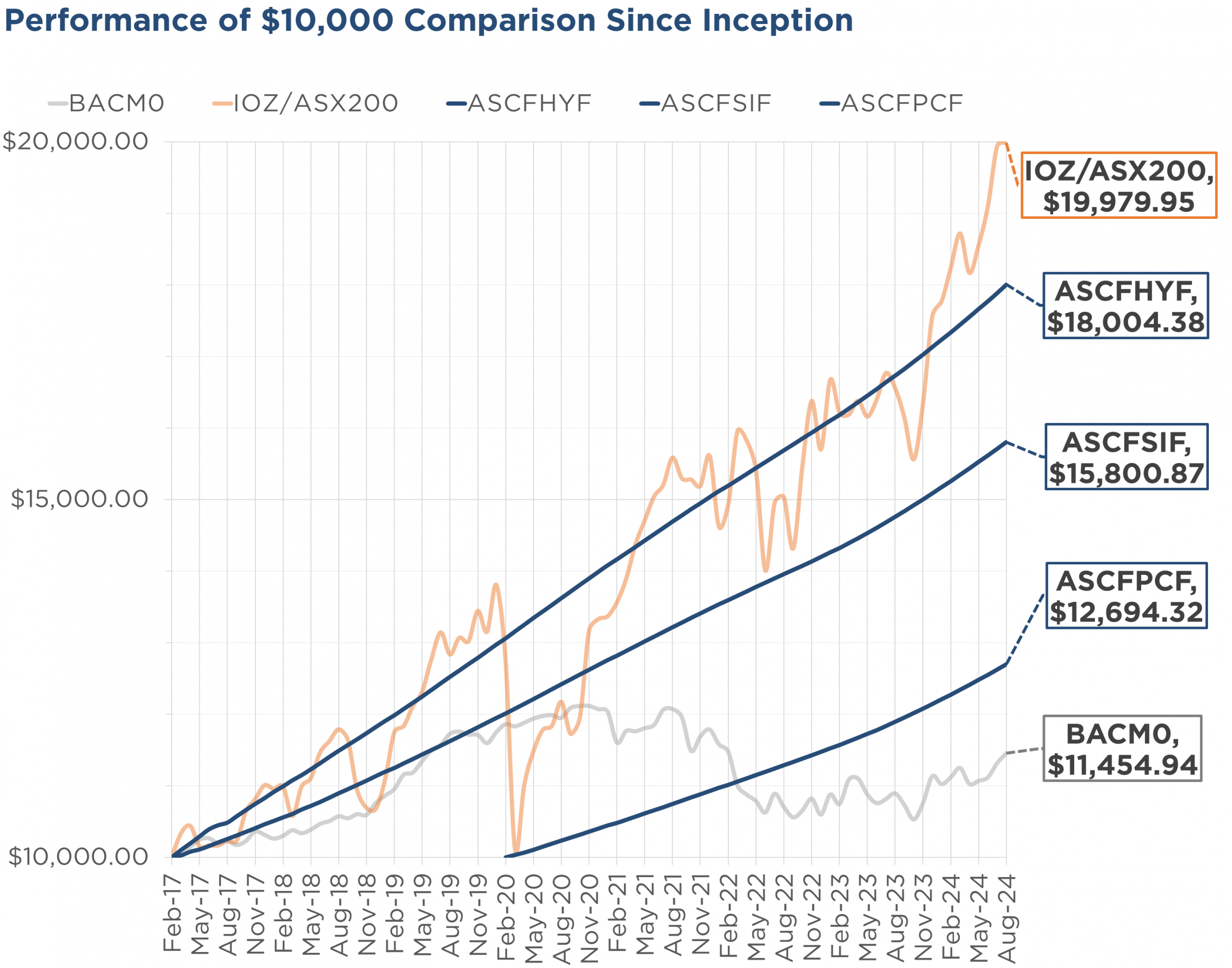

Monthly Managed Fund Cumulative Growth & Performance

Managed Funds Under Management

as at 31st of October 2024

| October 2024 | |

|---|---|

| ASCF High Yield Fund | $148,123,690.95 |

| ASCF Select Income Fund | $48,941,750.22 |

| ASCF Premium Capital Fund | $24,724,523.53 |

| Combined Funds under Management | $221,789,964.70 |

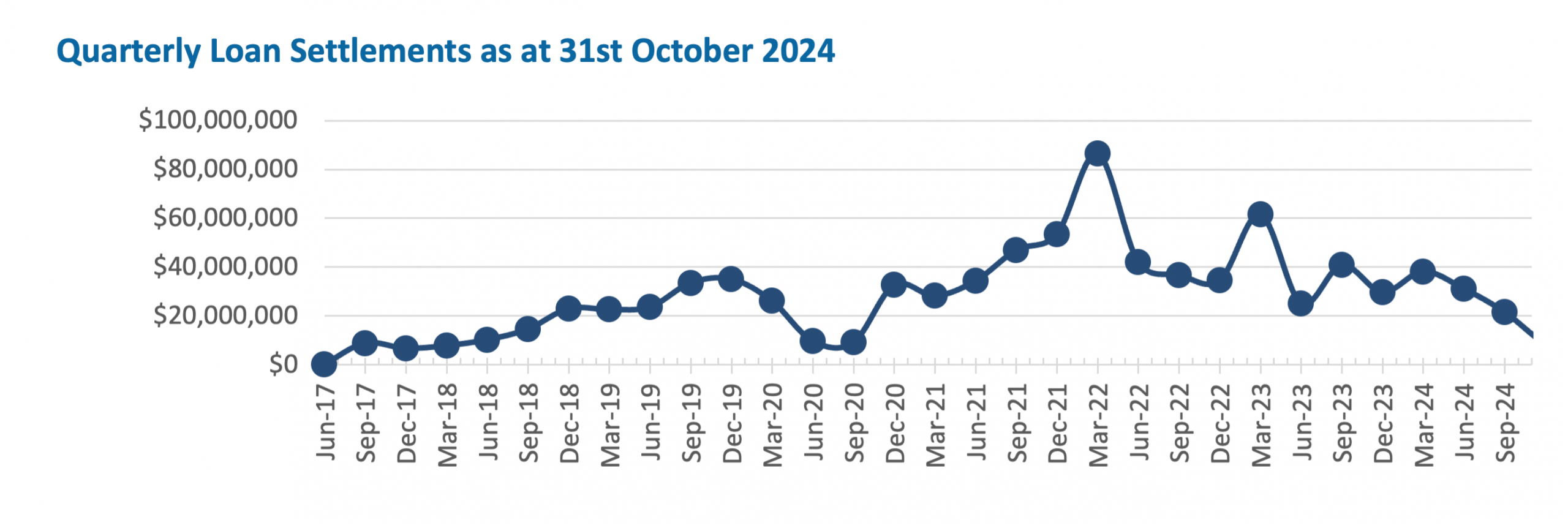

In October, loans and inquiry levels were steady, with $8,430,678.00 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of October.

Lending Activity Update

Quarterly Loan Settlements

as at 31st of October 2024

Current Loans by Fund Source

as at 31st of October 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 73.29% | 100% | 100% |

| 2nd Mortgage Loans | 18.70% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 8.01% | 0% | 0% |

| Avg. Weighted LVR | 48.32% | 46.21% | 41.48% |

| Avg. Loan Size | $1,222,351.63 | $926,161.69 | $808,970.59 |

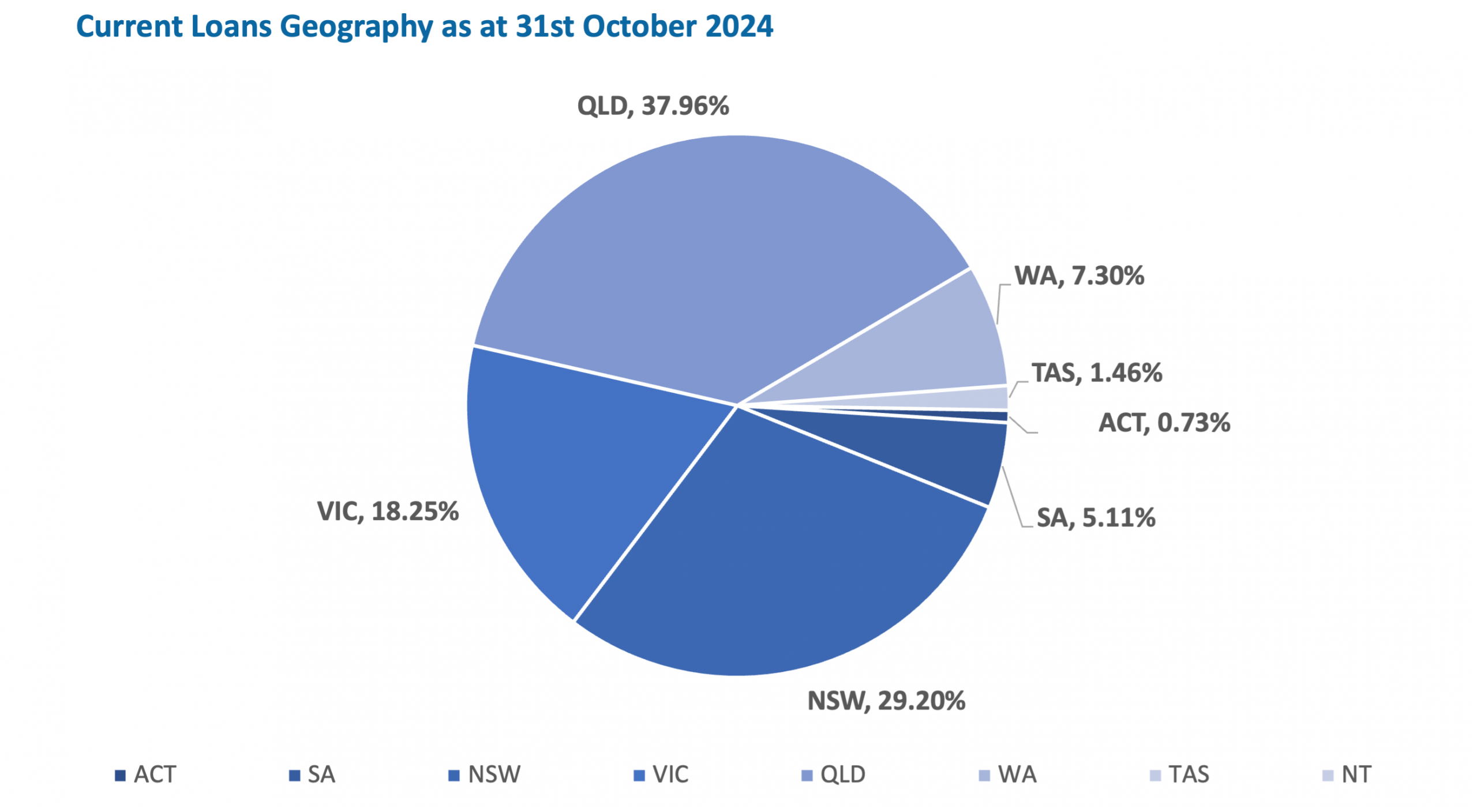

Current Loans Geography

as at 31st of October 2024

Why Invest with ASCF?

Flexible investment options with ASCF mortgage funds

At ASCF, we provide flexible mortgage funds tailored to meet diverse investment needs, whether you’re investing personally, through a company, or within an SMSF. Choose from three fund options and four commitment terms to match your goals.

Three mortgage funds for your needs

Our funds vary by risk tolerance, returns, and investment term, with options like spread protection and second mortgages. Each fund is audited yearly with all fund assets held by an independent custodian.

Flexible terms for every investor

Pick a term that fits your timeline:

- 3 Months – Great for those testing the waters in investing or seeking short-term returns without a long commitment.

- 6 Months – A middle ground for investors who want to a better return but may still need access in the medium term.

- 12 Months – Ideal for investors who can commit a full year and prefer a higher potential return for locking in their funds. This is our current highest paying term.

- 24 Months – Lock in today’s rates for longer-term stability.

Need extra flexibility? Mix and match terms and funds across accounts. Reach out to learn more today!

At ASCF, we’re here to help you invest on your terms. Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker approached ASCF for urgent financing to help his client settle on the purchase of a real estate rent roll business. Just 48 hours before settlement, the client’s initial financier backed out, leaving him in need of funds to complete the transaction.

Solution:

To meet this urgent need, the client offered his primary residence as collateral to access the required $1,000,000. ASCF’s team moved quickly, conducting thorough due diligence based on a real estate agent’s appraisal of the property, which was purchased for $5,200,000 in 2018.

With an assessed LVR of 9.09%, ASCF provided a 1st mortgage 3-month term loan at an interest rate of 8.75% per annum, allowing the client to meet his funding commitment in time.

What ASCF Does Differently:

When the client informed the broker of his need for financing within 48 hours, the broker immediately thought of ASCF. Why? Because of our three core differentiators:

Transparency in delivery – We offer clear communication and straightforward processes.

Confidence in delivery – We provide a reliable service when time is critical.

Speed of delivery – Our team understands the importance of a quick turnaround.

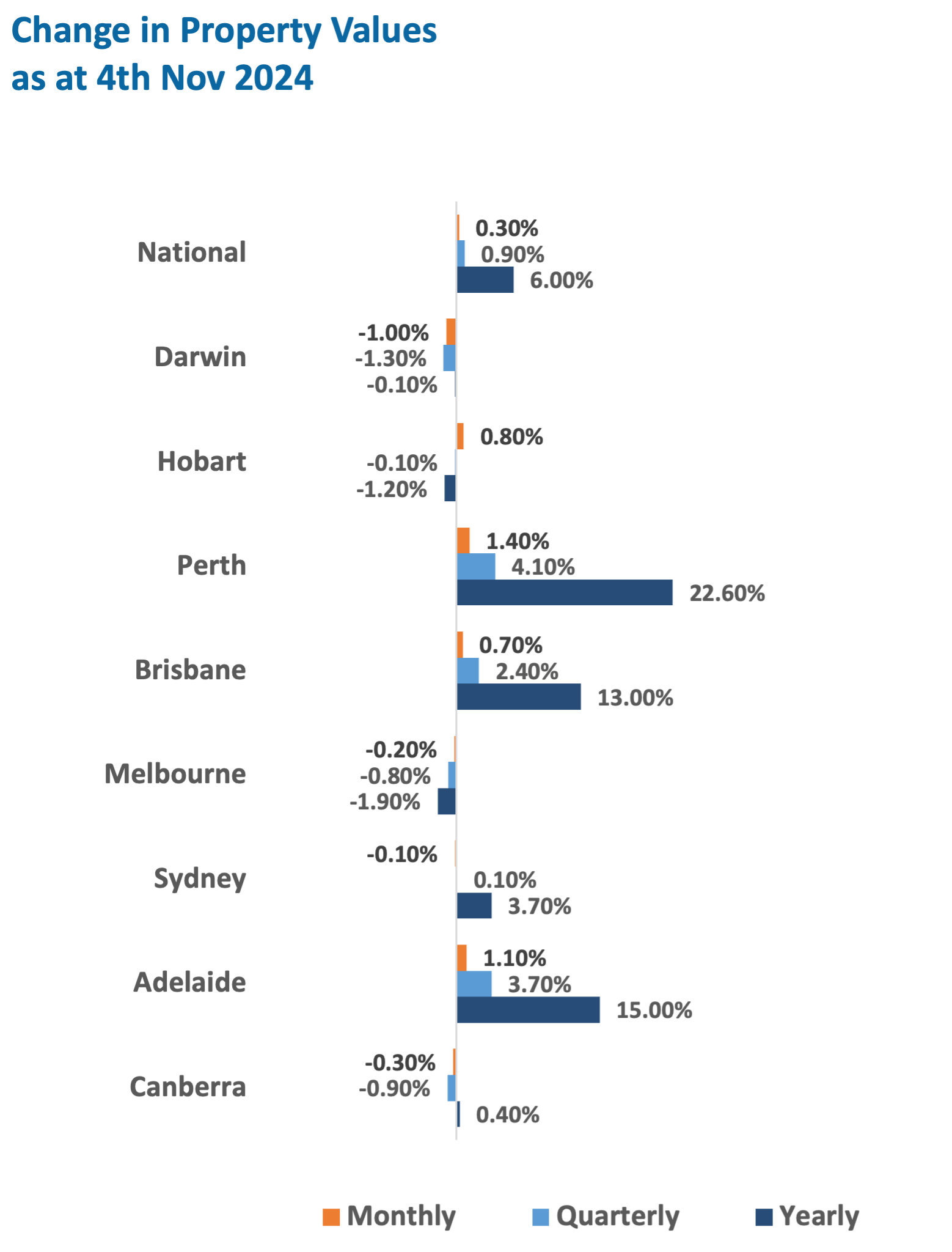

Market Update

Australian residential property prices continued to rise for the 21st consecutive month with a 0.3% increase, but signs of easing continue with Darwin, Canberra, Melbourne and now Sydney all experiencing a decline in value according to CoreLogic’s National Home Value Index, with losses of 1%, 0.3%, 0.2% and 0.1% respectively. Whilst this demonstrates that it is not all smooth sailing in the Australian property market, Brisbane, Hobart, Adelaide and especially Perth continued to perform strongly with further monthly increases of 0.7%, 0.8%, 1.1% and 1.4% respectively. Whilst the national capitals only saw a 0.2% increase for the month, the combined regionals are still performing strongly with a 0.6% monthly increase.

This new monthly data with more capitals and regions beginning to see a reduction or easing in prices, has impacted quarterly data now showing that Darwin, Canberra, Melbourne and Hobart have experienced losses for the quarter (1.3%, 0.9%, 0.8% and 0.1% respectively) whilst Sydney has now only seen 0.1% quarterly growth. Brisbane, Adelaide and Perth have however continued to see significant growth for the quarter, with 2.4%, 3.7% and 4.1% respectively.

As we head into the holiday season, and with the RBA remaining hesitant to reduce interest rates, it is expected to continue to see easing amongst the Sydney, Melbourne, Canberra, Hobart and Darwin markets, however the undersupply of property within Brisbane, Adelaide and Perth is likely going to see continued growth despite interest rate pressure.

Property Values

as at 4th of Nov 2024

Median Dwelling Values

as at 31st of October 2024

Quick Insights

Housing market on the cusp of another boom

Australia’s housing market shows signs of potential growth as experts anticipate that rate cuts in 2025 could drive higher demand, especially in Sydney, Brisbane, Adelaide, and Perth. Melbourne’s market remains relatively affordable, but with possible rate changes, investor interest may increase across major cities. Keep a close watch — 2025 could open up new opportunities in the property market.

Source: Australian Financial Review

One year on – cash rate holds at 4.35%

The RBA has held the cash rate steady at 4.35% for another month, citing high underlying inflation as the reason for not yet reducing rates. Despite headline inflation falling within target, the RBA remains cautious, aiming to ensure inflation returns to the midpoint of the target range.

While borrowers might be eager for a rate cut, experts suggest patience, with potential rate reductions anticipated in early 2025.

Source: Broker Daily