We’re back with another investor’s update covering February 2026, examining all the major economic and investment trends from the past month.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

Following last month’s decision to increase the official cash rate to 3.85%, RBA chief Michele Bullock has not ruled out further rises, noting that the board’s monetary policy meeting this week “will be a live meeting.”

Specifically, Bullock cautioned that although goods inflation has moderated, domestic capacity pressures mean services inflation remains high, with recent geopolitical tensions in the Middle East adding significant uncertainty to the situation, particularly regarding energy and oil prices.

Future Prospects

Accordingly, while the Big Four initially predicted a pause in March followed by a hike in May, they have now revised that forecast to predict another 0.25% rate rise at tomorrow’s board meeting after RBA deputy governor Andrew Hauser warned that inflation “is higher than the projection we published in February.”

As such, the Big Four are now forecasting rises in both March and May, bringing the peak rate to 4.35%. ANZ specifically blames the ongoing conflict in the Middle East, noting “the clearest and most immediate impact of the Middle East conflict on Australia is higher inflation“, while Westpac explains that the RBA “has not changed its pessimistic view of growth in supply capacity following the national accounts.”

These predictions are underpinned by the release of January’s CPI data, which remained at 3.8% in the 12 months to January 2026, with the trimmed mean coming in at 3.4%. In January, the CPI rose by 0.5% in seasonally adjusted terms, with housing (+6.8%) being the largest contributor.

Property Market

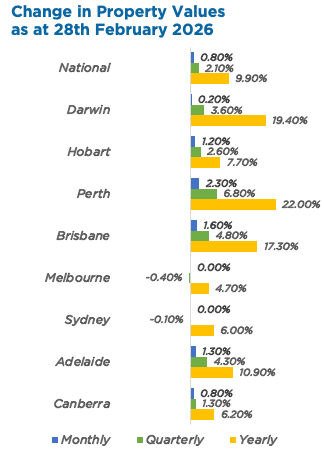

As a result, the Australian property market continues to be distinctly ‘two-speed’. In February, the midsized capitals again posted significant gains, whereas values in Sydney and Melbourne stagnated.

Perth experienced a second straight monthly rise of greater than 2%, while Brisbane (+1.6%), Adelaide (+1.3%), and Hobart (+1.2%) also posted monthly gains of greater than 1%. Conversely, values in Melbourne and Sydney remained flat, posting slight rolling quarterly decreases of -0.4% and -0.1%, respectively.

These figures are underpinned by a resilient labour market, with seasonally adjusted unemployment remaining at 4.1%, and the number of unemployed people falling to an eight-month low at 624,700.

How ASCF Helps

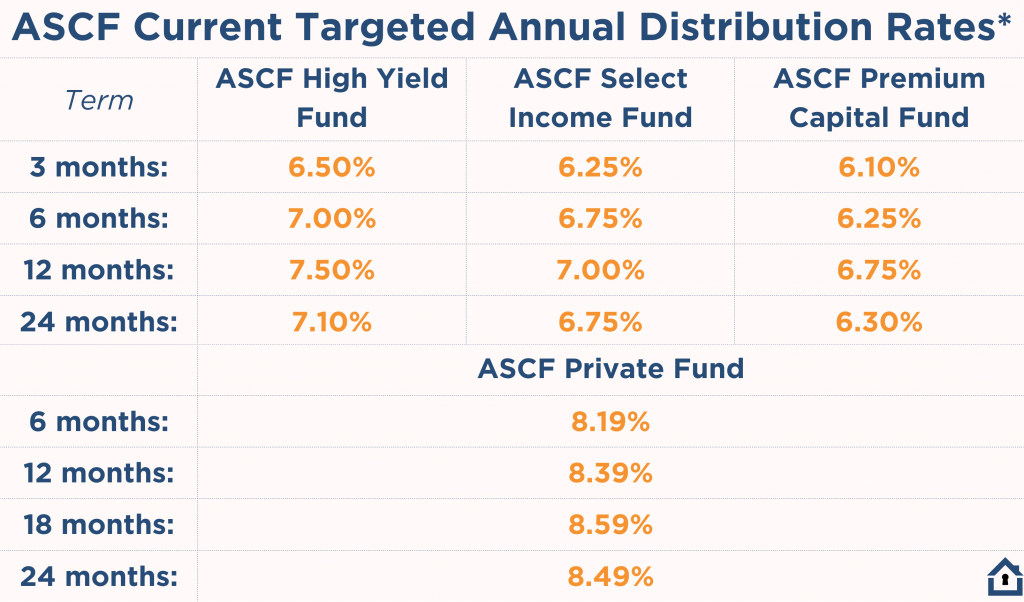

While global geopolitical tensions and the prospect of further domestic rate rises have increased market uncertainty, ASCF’s funds continue to provide an appealing alternative to the fluctuations of variable-rate assets. Our ASCF High Yield Fund offers a competitive targeted distribution rate of 7.50% per annum for a 12-month fixed term, with interest paid monthly.

Half-Yearly Financials Now Online

Our half-yearly audited financial statements for each of our retail funds, which cover the period ending December 31, 2025, are now available to view on our website or by clicking here. If you have any questions about these, please do not hesitate to contact our Investor Relations team at 1300 269 419.

Sources: Australian Fund Monitors, Bloomberg, Investing.com

Note 1: Premium Capital Fund began in February of 2020

Note 2: Past performance is not indicative of future performance.

To learn more, see our Investor FAQs.

Lending Activity Update

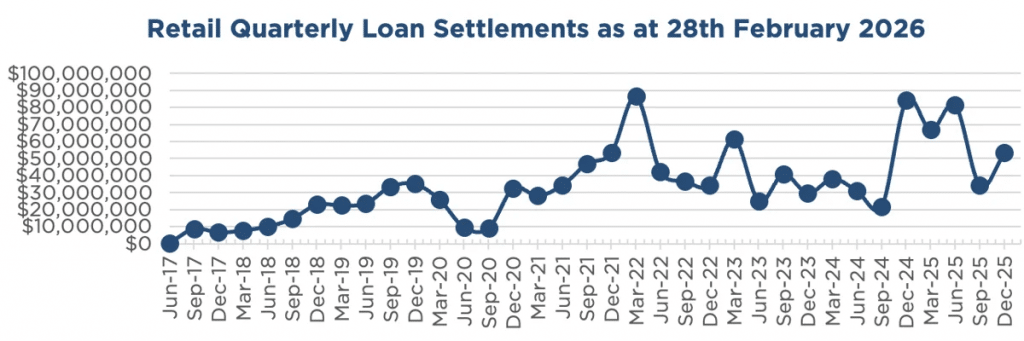

In February, inquiry levels were healthy, with $18,351,346.10 in loans settled.

The unit price across all three of our retail funds remains at $1.00 per unit.

All monthly distributions have been paid in full for February.

To learn more, see our Borrower FAQs.

Why Invest With ASCF?

Global Uncertainty & The Appeal of Australian Pooled Mortgage Funds

Between the conflict in the Middle East, the ongoing war in Ukraine, shifting geopolitical alliances, and energy market disruptions, there is a growing sense of uncertainty and distrust in the global markets.

Given recent events, we have already had investors reaching out to enquire about our pooled funds, looking for investment opportunities with a stronger domestic focus.

The Resilience of Pooled Mortgage Funds

In uncertain times like these, pooled mortgage funds can be an excellent investment option, as, rather than being priced daily on global sentiment, they are backed by real Australian property assets and governed by tailored lending agreements. Accordingly, returns are generated from managed interest payments, not share price movements.

What’s more, each loan is secured by registered mortgages over predominantly residential property, and, typically, short-coded loans provide a more manageable level of risk.

Backed By Australian Property

ASCF’s pooled funds are backed by Australian property only, which—as we see in the market update section below—continues to be a resilient asset. Additionally, each loan is assessed on its individual merits. It’s not simply about asset value—loan purpose, borrower character, location, and exit strategy are all critical factors too.

For many investors, property funds offer a more predictable return compared to the volatile global markets. This is especially true in Australia, given the demand on all levels of the property market, whether for residential or investment purposes. With the current lack of supply and a shortage of trades and materials, we expect these trends are likely to continue in the medium term.

ASCF’s Track Record

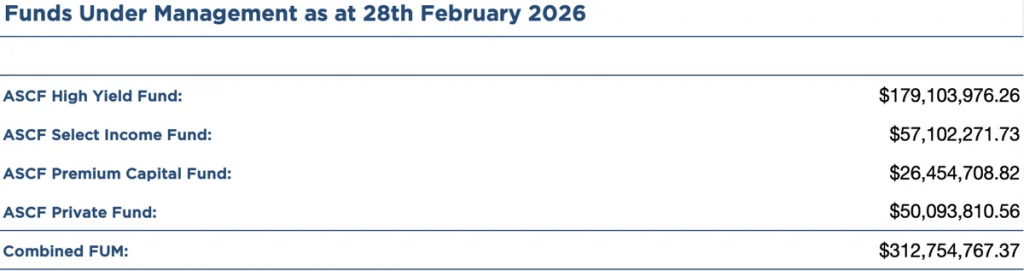

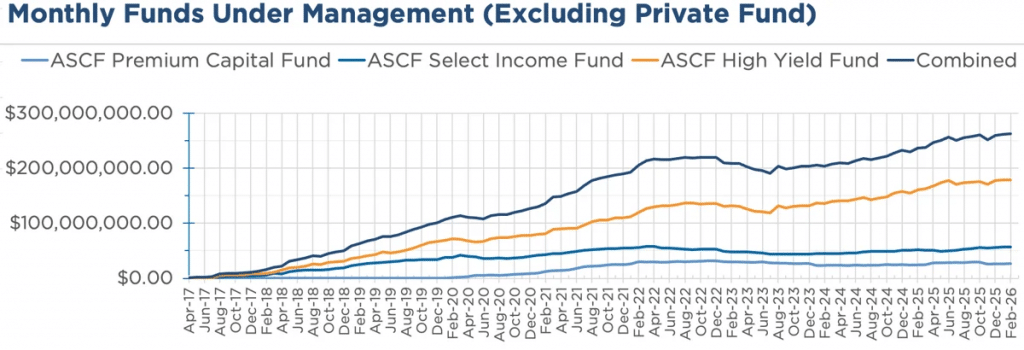

In our current times, finding peace of mind with your investment choices can be challenging. However, at ASCF, we feel that our funds have shown stability to date, with over $312 million in funds under management and growing.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

You can learn more about Our Funds here.

An Interesting Transaction

Problem:

An AFG broker presented us with a bridging transaction, wherein the customer had already purchased a unit in Noosa, which they were downsizing to. However, the customer urgently required additional funds to assist with the sale of their home and provide living expenses pending its sale.

Solution:

ASCF offered a 1st mortgage loan of $222,000 at 10.25% per annum over a six-month term against the newly purchased unit, which was unencumbered. Additionally, we also took a 2nd mortgage over their home as collateral security, allowing ASCF to control the sale proceeds when the property eventually settled.

Given the very low LVR of 7.34%, we were able to accept a Cotality desktop valuation to meet our requirements. We also confirmed the value of the 1st mortgage debt, given that the sale of the property is the exit strategy for our loan.

Ultimately, the loan was settled within 3 business days from the initial enquiry, pleasing both the customer and the broker.

What ASCF Does Differently:

ASCF remains one of the most responsive private lenders in the Australian market without compromising on credit quality, much to the delight of our customers and broker partners.

For more details about this transaction, see our Loan Summary.

Property Update

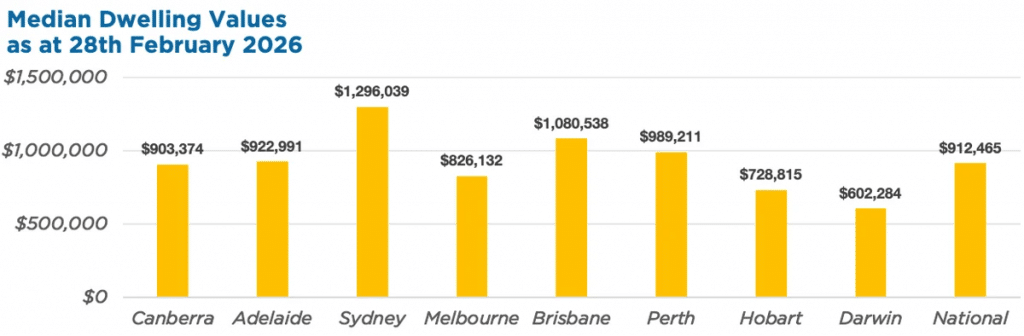

February was another strong month for Australian property values, posting a national rise of 0.8% for the second consecutive month. Perth (+2.3%) again led the way with a second straight monthly rise of greater than 2%, adding more than $22,500 to the median dwelling value over the month. Similarly, Brisbane (+1.6%) and Adelaide (+1.3%) again saw monthly increases of greater than 1%.

Conversely, values in Melbourne and Sydney were flat over February, with both cities notching slight rolling quarterly decreases of -0.4% and -0.1%, respectively. As a result, regional areas continue to outperform the capital cities, rising by 1.1% month-on-month, compared to 0.6% for the capitals. Nationally, rents increased 1.7% over the three months to February 2026, denoting the highest rolling quarterly increase since April 2025.

Source: Cotality HVI, 02 March 2026