We’re kicking off the year in style with another monthly investor’s update, analysing the major trends from January 2026.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

Last week’s RBA meeting resulted in a notable recalibration of domestic monetary policy. After a period of easing throughout 2025, the RBA decisively shifted its policy stance and increased the official cash rate by 25 basis points to 3.85%.

This increase marks the Board’s first tightening of policy since November 2023, as the RBA recalibrates to a higher-for-longer environment, noting that domestic capacity pressures are greater than previously assessed. This resulted in a revised forecast, with inflation now not expected to return to the 2.5% target midpoint until June 2028.

This move was precipitated by a resurgence in inflationary pressures over the second half of 2025, with the annual CPI for the December quarter rising to 3.8%, and the trimmed mean climbing to 3.3%. A key driver of this was the 21.5% annual increase in electricity prices, although headline figures were somewhat skewed by the unwinding of state-based energy subsidies, among other temporary factors.

Future Prospects

So, what does this mean as we navigate 2026?

Consensus among the Big Four diverges regarding the path ahead. NAB has adopted a hawkish stance, predicting another increase in May, whereas CBA, Westpac, and ANZ currently anticipate a period of stability.

Property Market

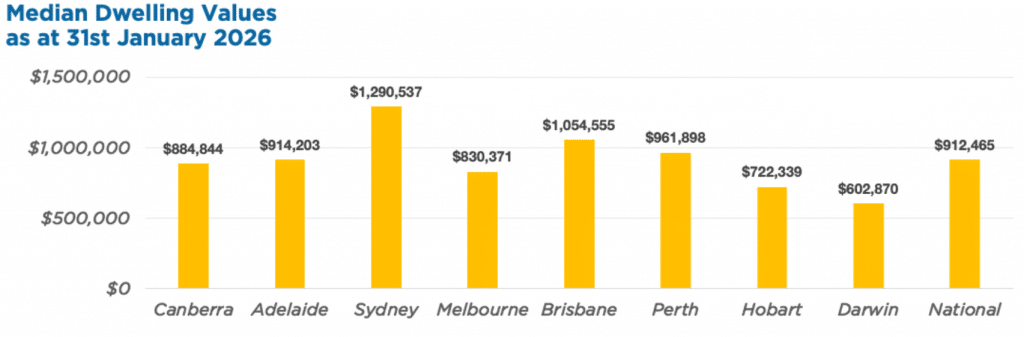

Despite this return to a tightening bias, the Australian residential property market continues to show resilience. CoreLogic’s national Home Value Index rose by 0.8% in January, while national annual growth accelerated to 10.2% as of January 2026—more than double the 4.9% recorded across 2024.

Perth and Adelaide led the way with monthly gains of 1.9%, while Sydney and Melbourne rebounded after slight declines in December.

Residential property prices continue to be underpinned by a shortage of new housing supply, rental price growth (+3.9%), and a robust labour market, with ABS data for December revealing the unemployment rate fell to 4.1% as the economy added 65,200 jobs.

How ASCF Helps

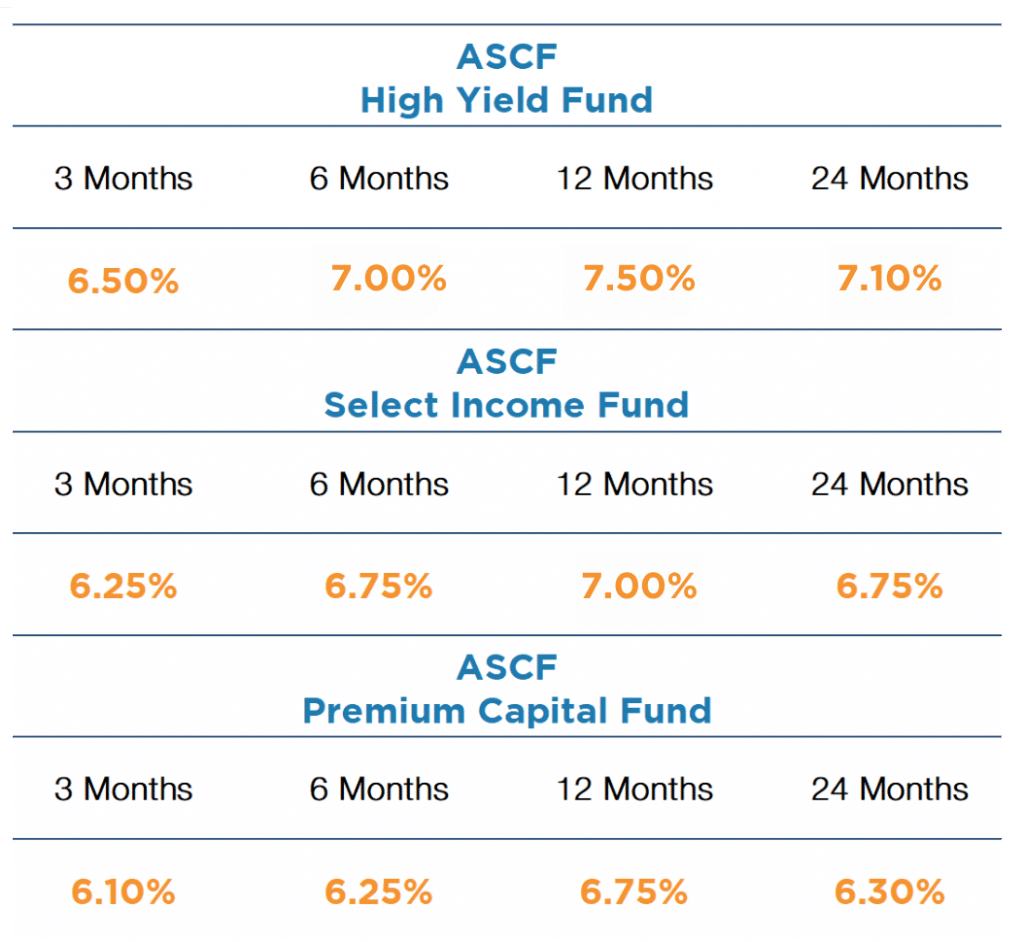

As the RBA continues to navigate these complexities, ASCF’s targeted distribution rates provide an alternative to the volatility of variable-rate markets. Our ASCF High Yield Fund offers a competitive targeted distribution rate of 7.50% per annum for a 12-month fixed term, with interest paid monthly.

We hope your year has gotten off to a fantastic start, and we look forward to staying in touch throughout 2026!

To learn more, see our Investor FAQs.

Lending Activity Update

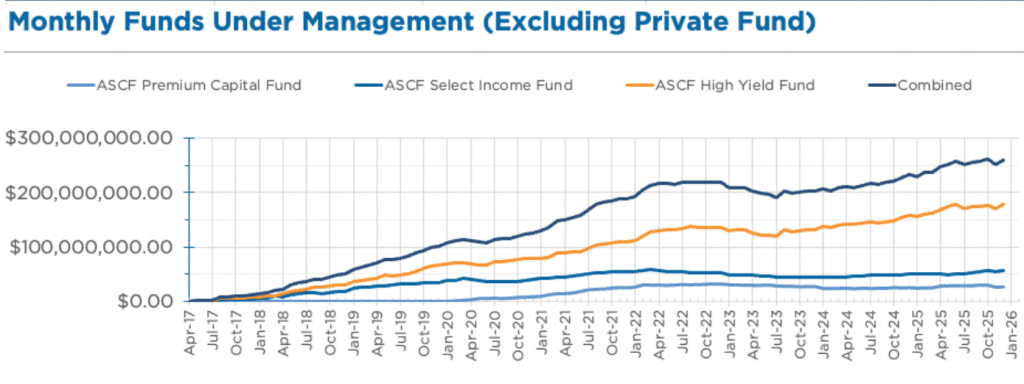

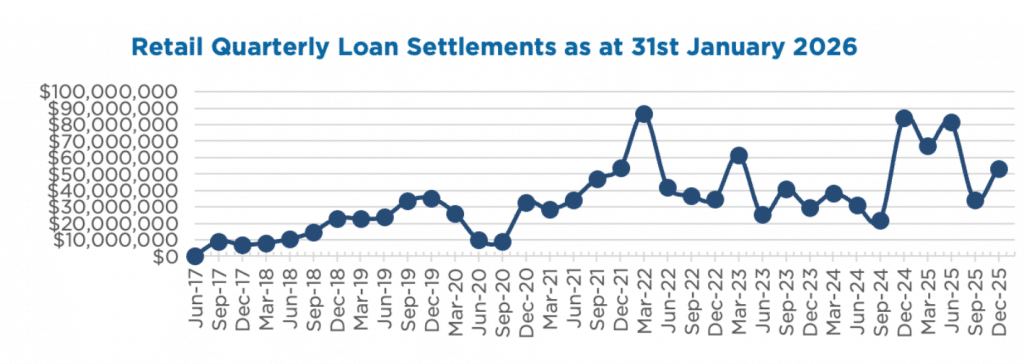

In January, loan originations and inquiry levels were encouraging, with $4,699,952.83 in loans settled.

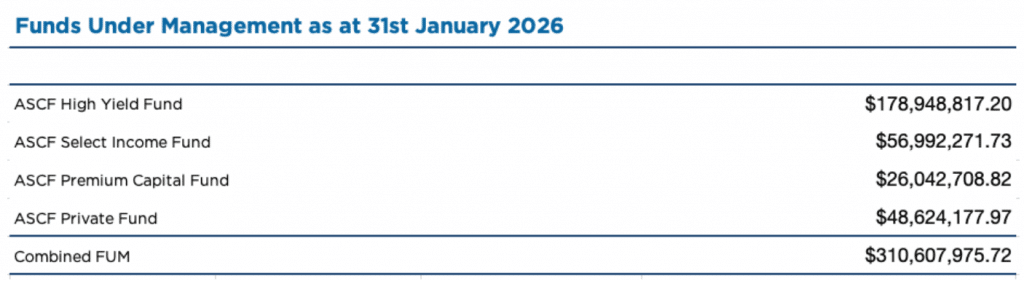

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for January.

To learn more, see our Borrower FAQs.

Why Invest With ASCF?

Explained: Income and Return Potential in Pooled Mortgage Funds

Pooled mortgage funds provide investors with access to income generated from loans secured by property or vacant land.

How Do Pooled Mortgage Funds Work?

Rather than relying on market timing or capital growth of these assets, pooled mortgage funds generate returns primarily from mortgage interest payments, creating a more predictable income stream.

This is because each loan is secured against property assets, which can be assessed on their individual merits, whether that be the asset type, location, LVR, loan purpose, or the term required.

Accordingly, the risks can be managed within our parameters and tolerances. If a borrower defaults, the underlying property can be used to recover the funds, adding an important layer of protection.

Value Assessment

Assessing the value of an asset is vital to this process. Whether we utilise our network or conduct a full qualified valuation, we can factor in any potential forecasted market drift. Then again, as most of our loans are short-term (less than 12 months), we have an advantage that normal long-term mortgage providers don’t have.

Diversification

Another key strength of ASCF’s funds is diversification. Put simply, a single investment is spread across many loans, thereby reducing the potential impact of any one borrower experiencing difficulty, and helping to smooth overall returns and maintain a stable unit value.

With the volatility of the share market, pooled mortgage funds can offer a calmer, more predictable investment option to diversify into.

Pooled Mortgage Funds vs Property Investments

For some, investing in property can offer good returns. However, it can also introduce a host of issues, such as bad tenants or difficult property managers.

At ASCF, we have served many investors who have chosen to go down the path of pooled mortgage funds after losing confidence in their property investment journey. Ultimately, for investors seeking lower volatility and a simpler alternative to owning an investment property, pooled mortgage funds can be a highly attractive income generation option.

Want to learn more? Contact us to explore your investment options.

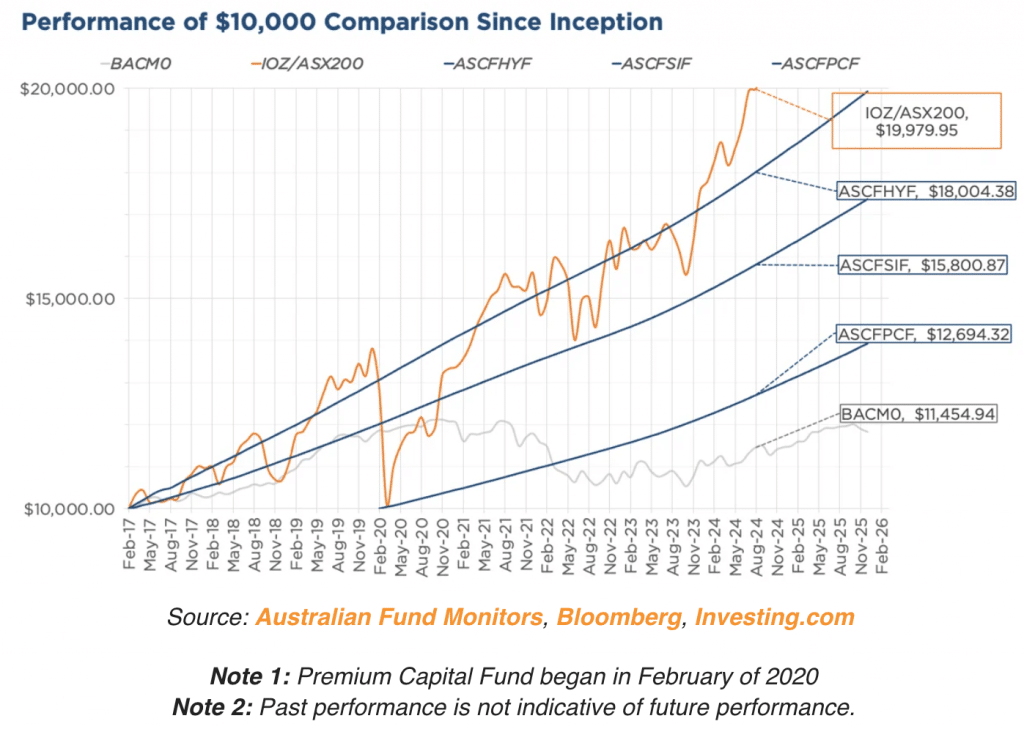

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker approached ASCF with a borrower who was at risk of losing his principal place of residence to their existing lender, a major bank.

The borrower had separated from his wife and lost his job within a short timeframe, resulting in the existing mortgage falling into arrears.

At the time of the application, the borrower had secured a new job with income that was more than sufficient to service the ASCF loan on a monthly basis and confirm his ability to refinance at the end of the 12-month term.

Solution:

ASCF approved and settled the loan in time to avoid the existing major bank taking enforcement action and selling the property as the mortgagee-in-possession.

Based on a full valuation from a panel valuer, the LVR on the security was 61.27%.

ASCF provided a total loan of $435,000 at a rate of 12.25% over a 12-month term.

Despite having a 12-month term, the broker was able to refinance the borrower to a long-term solution within just 7 months.

What ASCF Does Differently:

ASCF was able to assist a borrower where most other lenders could not. Despite the poor repayment history on his existing loan, ASCF was able to recognise that a one-off life event had caused the issue.

With a new job providing a strong income stream, the borrower ensured that they made repayments on time with ASCF each month, before successfully exiting the loan to a long-term solution.

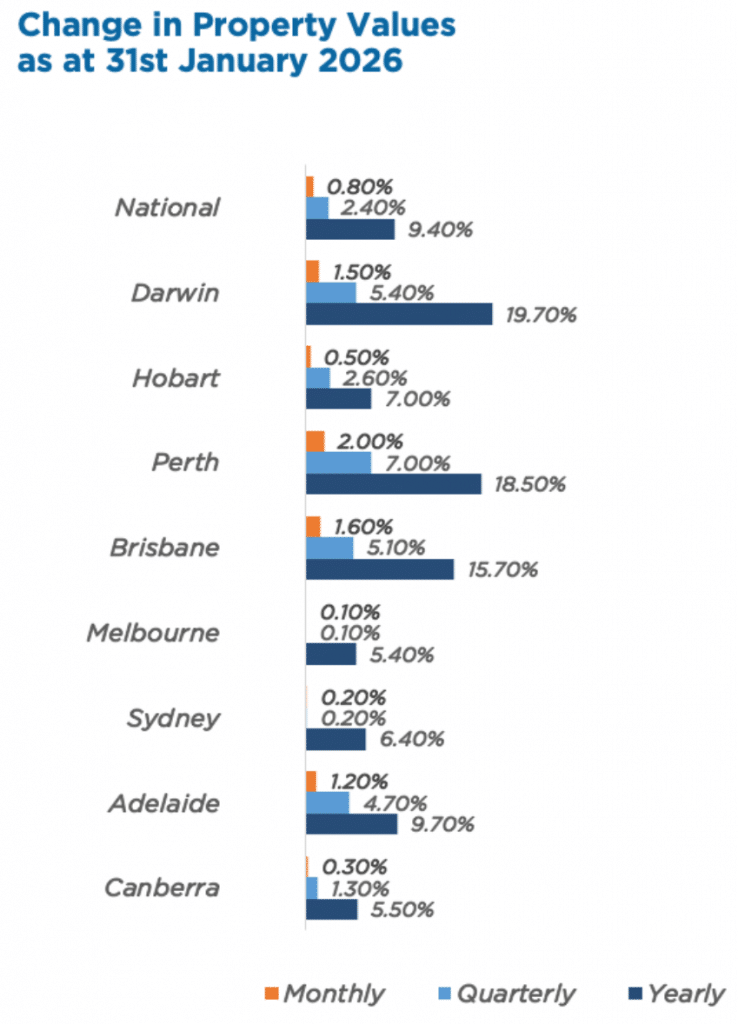

Property Update

House prices bounced back in January after a slower December, rising by 0.8% nationally. After slight falls last month, values in Melbourne and Sydney rebounded, while Brisbane, Adelaide, Perth, and Darwin all saw increases of 1.2% or greater.

More broadly, the national median dwelling value surged by 9.4% over 2025—almost double the 4.9% national rise seen in 2024. Regional markets outperformed capital cities with a 10.3% annual rise and 1% monthly rise, compared to 9.2% and 0.7% rises, respectively, for the capitals.

Across the capital cities, house values in the lower quartile increased by 1.3% in January, compared to a 0.3% rise in the upper quartile.

Source: Cotality HVI, 02 Feb 2026