Trading Update

This months RBA meeting left interest rates on hold as expected based on underlying inflation falling in the June quarter from an annual rate of 4% to 3.9%.

Whilst RBA governor Michele Bullock believes it is still “premature” for the board to consider cutting rates this year the release of unemployment data last week showing unemployment increasing to 4.2% up 0.1% from a month prior indicates the impact of rate rises are starting to filter through to economic data and will continue to do so.

As a consequence there is much debate amongst economists as to whether the first of several rate cuts will eventuate late this year or early next year.

Despite this the consensus is that there there are likely to be no further interest rate increases with rates now expected to drop by between 0.5% and 0.75% over the next 6 to 9 months with the first of these rate reductions likely to occur as early as November or December.

The latest numbers on building activity released last month have confirmed that the undersupply of housing across the country is unlikely to get better any time soon. The total number of new home builds including apartments hit 158,798 in the year to March 24 which is the lowest since 2012.

The impact of high interest rates, a lack of labour in the construction industry and the substantial increases in the cost of materials are all working against the sector and certainly while migration levels remain at elevated levels the structural undersupply in housing looks set to underpin housing prices for some time yet particularly with multiple rate cuts not far away now.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

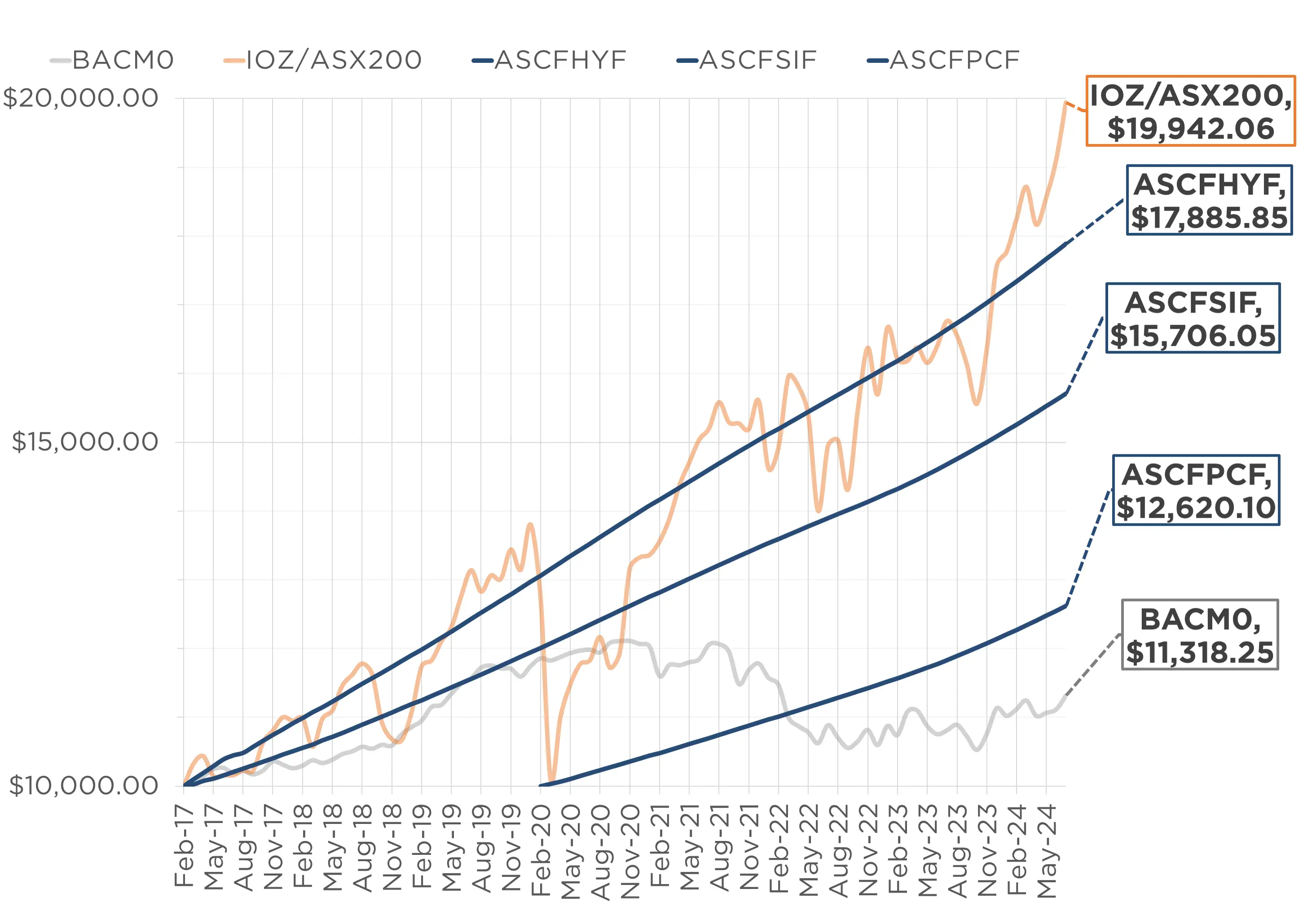

Monthly Managed Fund Cumulative Growth & Performance

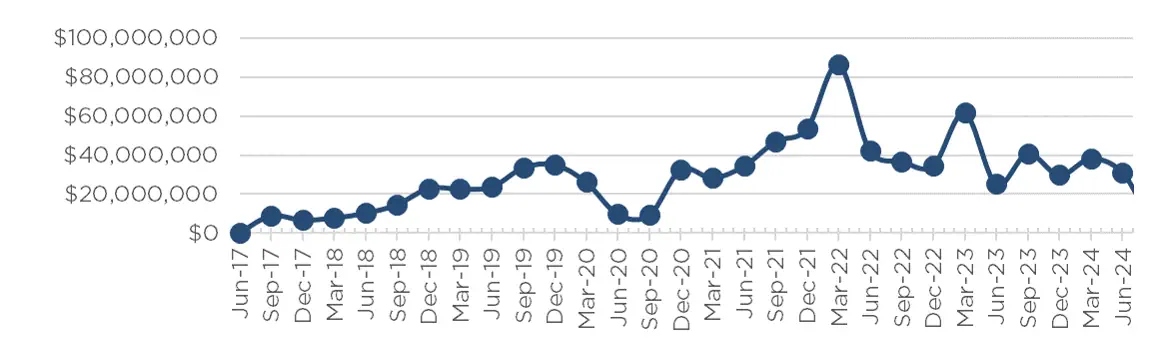

Managed Funds Under Management

as at 31st of July 2024

| July 2024 | |

|---|---|

| ASCF High Yield Fund | $146,831,302.44 |

| ASCF Select Income Fund | $47,857,803.73 |

| ASCF Premium Capital Fund | $23,264,023.53 |

| Combined Funds under Management | $217,953,129.70 |

In July, loan originations and inquiry levels were strong, with $6,846,000 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of July.

Lending Activity Update

Quarterly Loan Settlements

as at 31st of July 2024

Current Loans by Fund Source

as at 31st of July 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 81.27% | 100% | 100% |

| 2nd Mortgage Loans | 12.58% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 6.15% | 0% | 0% |

| Avg. Weighted LVR | 55.33% | 51.80% | 50.28% |

| Avg. Loan Size | $1,556,824.63 | $885,875.46 | $910,708.33 |

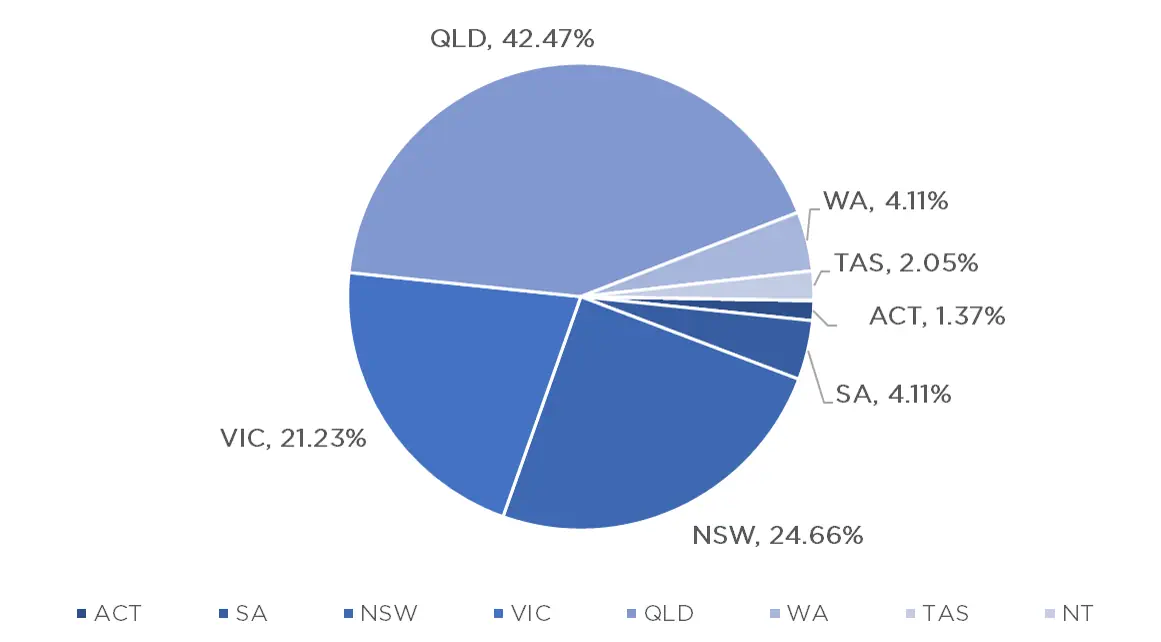

Current Loans Geography

as at 31st of July 2024

Why Invest with ASCF?

One of the questions I am often asked is what types of loans we typically originate with our investment funds. Simple answer, bridging finance! Let’s have a look into why these short-term loans are popular with us and how they also benefit both investors and borrowers.

- Strong asset type so better security

Typically a borrower requires a bridge where they have purchased a new property but are yet to sell their existing property. As there are two properties involved with this type of loan we secure the loan against both and fund the purchase of the new property. We undertake valuations on both properties and take into account the existing loan and costs involved in the new purchase plus what the end debt if any will remain. Having two properties involved also gives us better financial recourse if it was to be required. - Higher Returns for Investors

Bridging loans typically come with higher interest rates, offering better returns for investors. The urgency often associated with these loans allows lenders to charge a premium, further enhancing the potential returns. - Flexible Loan Structures

Bridging finance can be tailored to meet specific borrower needs, such as capitalised interest, which can be paid on the conclusion of the loan. With only valuation costs required upfront ASCF offers a convenient choice for borrowers. - Stability Amid Market Fluctuations

Bridging finance tends to be less affected by market volatility than long-term loans due to its short-term nature, this makes any market fluctuations a lot less likely to have an effect on the asset values and again having two assets makes the recovery of the funds much more achievable if required. - Efficient Capital Deployment

ASCF pooled mortgage funds aim to keep capital constantly deployed to achieve our targeted returns. The short-term nature of bridging loans allows these funds to quickly reinvest repaid capital into new loans, ensuring effective capital management. - Rapid Funding Process

Bridging finance often requires fast decision-making and funding, which our pooled mortgage funds can provide through our streamlined processes. This quick turnaround is often crucial for borrowers needing immediate access to funds, which gives more clarity and urgency to their decision process. - Risk Diversification

Having multiple properties helps to diversify the risk to our funds, and in most circumstances these loans are used for owner occupied properties so the need and motivation to see the contract through is strong. We maintain good communication with the clients to monitor their process through to the sale of the original property, so that we can assist borrowers if required.

Conclusion

Bridging finance is well-suited to pooled mortgage funds due to its short-term nature, potential for higher returns, strong asset value, flexibility, and quick capital deployment. These factors make it a popular and effective choice for both investors and borrowers.

If you would like to know more about what we offer or want further information then please reach out to me on 0459 835 335.

.

An Interesting Transaction

Problem:

A borrower came to us this month seeking short term funding for the purchase of a new home in St Kilda, Melbourne. He had paid the deposit but had insufficient funds to pay the full balance due to a delay in payment from a matrimonial settlement. Unfortunately his ex-wife decided to dispute a very small portion of the distribution and as such, the entire proceeds from the sale that he was expecting to receive were held up.

Solution:

ASCF obtained a valuation report which confirmed the contracted purchase price at $2.53m and also sought a letter from the borrower’s solicitor to confirm the amount held in trust, the amount that our borrower was entitled to under the property orders and the amount under dispute. We ascertained that even without the monies under dispute, there was sufficient funds held in trust for the benefit of our borrower to repay the loan amount sought to complete the purchase of the St Kilda property.

Hence, ASCF provided a 6 month loan at an LVR of 65.42% for $1.655m at 11.95% pa to allow the customer to complete the settlement on his St Kilda purchase rather than forego his deposit and lose the property.

What ASCF Does Differently:

ASCF is able to take a more pragmatic approach in a assessing our borrowers circumstances so that we can assist our clients with their diverse financial needs.

Market Update

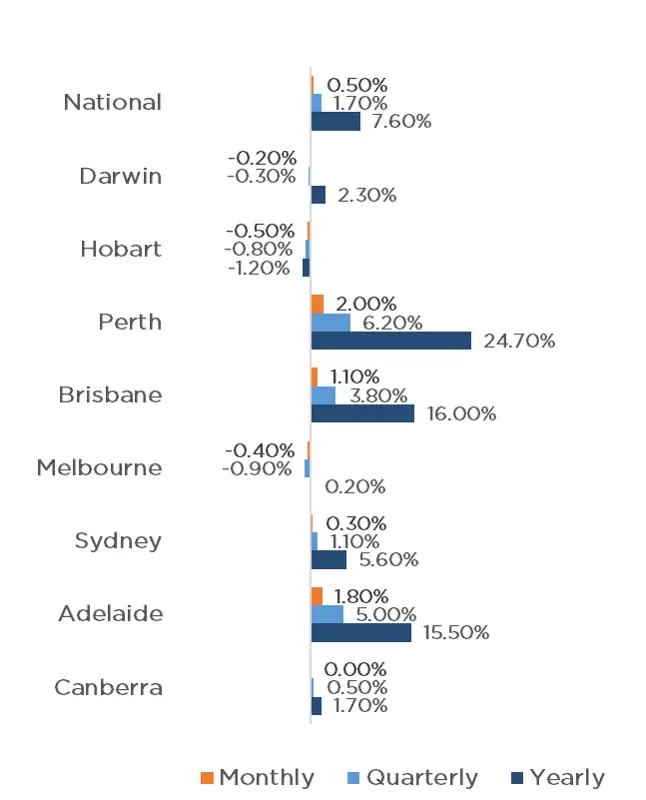

The headline growth rate for residential property values for the combined capital cities remains positive, at 0.5% for July bringing the 18th consecutive monthly increase in home values nationally, however it was not all roses, as three capital cities, Melbourne (0.4%), Hobart (0.5%) and Darwin (0.2%) all recorded a fall in property prices. Perth once again led the way with the strongest growth, increasing by 2% for the month, Adelaide and Brisbane also performed strongly with a 1.8% and 1.1% increase respectively, followed by Sydney with 0.3%.

Whilst property price growth appears to be easing, the annual growth for the combined capitals is at 7.9%, with all cities excluding Hobart receiving some level of growth for the year, headlined by Perth with a whopping 24.7% increase, and Brisbane and Adelaide also in double digit growth with 16 and 15.5% growth respectively. This level of growth has also extended to the regions, with a combined regional growth of 6.9%, contributing to a national average of 7.60%.

Property Values

as at 31st of July 2024

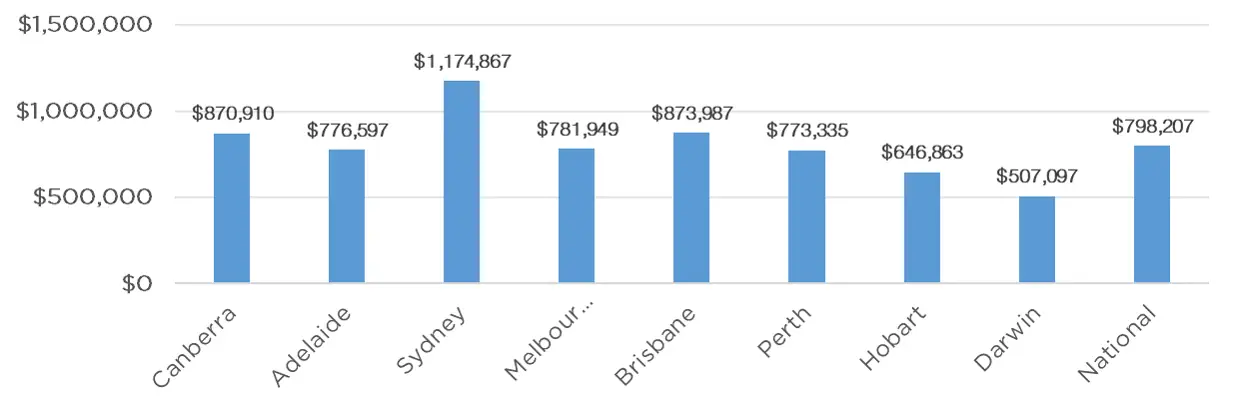

Median Dwelling Values

as at 31st of July 2024

Quick Insights

Golden Opportunities

Despite challenging conditions, millions of dollars in luxury apartment sales have been made in the past two months on the Gold Coast.

“It’s a flight to quality,” said Paul Gedoun of S&S Projects.

Most of the apartment buyers have been owner-occupiers and downsizers. The average price of an apartment has more than doubled since 2021 to almost $1.8 million as the Gold Coast has become a more cosmopolitan and sophisticated lifestyle destination.

Source: Australian Financial Review

Confidence and Construction

As Australia gears up for its next home-building boom to meet a supply shortage that has only worsened with the post-COVID-19 pandemic surge in costs, builders want to ensure a smooth pipeline of land supply.

Metricon, the country’s largest detached home builder, has seen the opportunity and is looking to expand its pipeline, in a bid to attempt to build consumer confidence in the home-building industry.

Source: Australian Financial Review