Trading Update

The next RBA meeting is scheduled for the 5th and 6th August with tomorrows unemployment data and the quarterly CPI due to be released on the 31st July crucial in determining whether the RBA is likely to leave rates on hold or increase them.

Last weeks Westpac consumer sentiment index slipped 1.1% in July, with the reading of 82.7 showing pessimists far outnumbered optimists.

Whilst concerns of persistent inflation and further interest rate rises are weighing on the Australian consumer last weeks drop in US inflation for June which was down 0.1% has boosted equity markets and provided confidence to economists that interest rates across most developed countries should start coming down over the next several months.

Australian interest rate futures have come off considerably over the last few days and whilst the labour market has been tighter than expected there are signs that it will start to ease in line with the weak GDP numbers we have seen of late.

Whilst the RBA’s path to a soft landing remains narrow it is in our opinion still achievable without the need for a further rate rise with most indicators currently pointing to an economy that is continuing to slow and a consumer that has been battered by ongoing cost of living pressures and higher mortgage payments.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.25% | 7.75% | 7.30% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.25% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

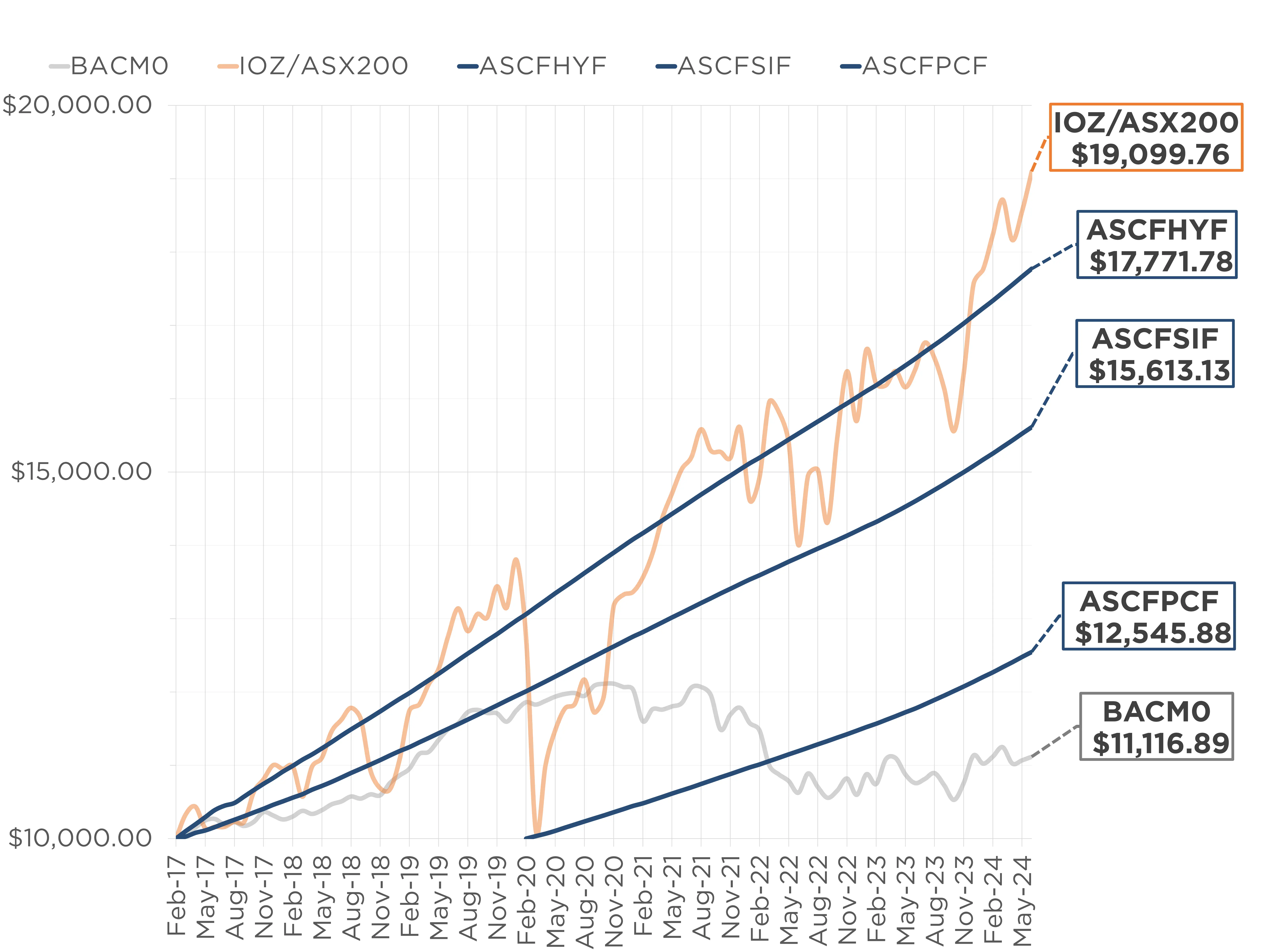

Monthly Managed Fund Cumulative Growth & Performance

Managed Funds Under Management

as at 30th of June 2024

| June 2024 | |

|---|---|

| ASCF High Yield Fund | $144,079,703.10 |

| ASCF Select Income Fund | $45,989,197.73 |

| ASCF Premium Capital Fund | $23,793,373.53 |

| Combined Funds under Management | $213,862,274.36 |

In June, loan originations and inquiry levels were strong, with $8,336,510 in new loan originations settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of June.

Lending Activity Update

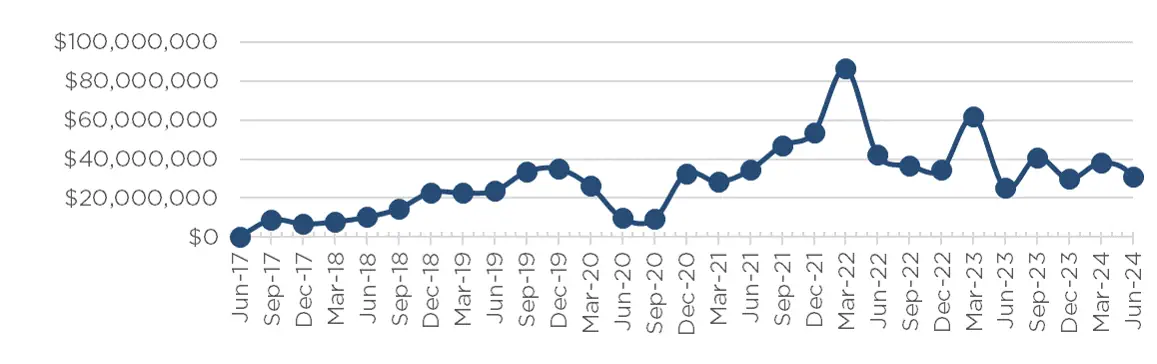

Quarterly Loan Settlements

as at 30th of June 2024

Current Loans by Fund Source

as at 30th of June 2024

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 81.37% | 100% | 100% |

| 2nd Mortgage Loans | 12.65% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 5.98% | 0% | 0% |

| Avg. Weighted LVR | 55.69% | 52.75% | 49.71% |

| Avg. Loan Size | $1,489,135.32 | $924,219.06 | $900,291.67 |

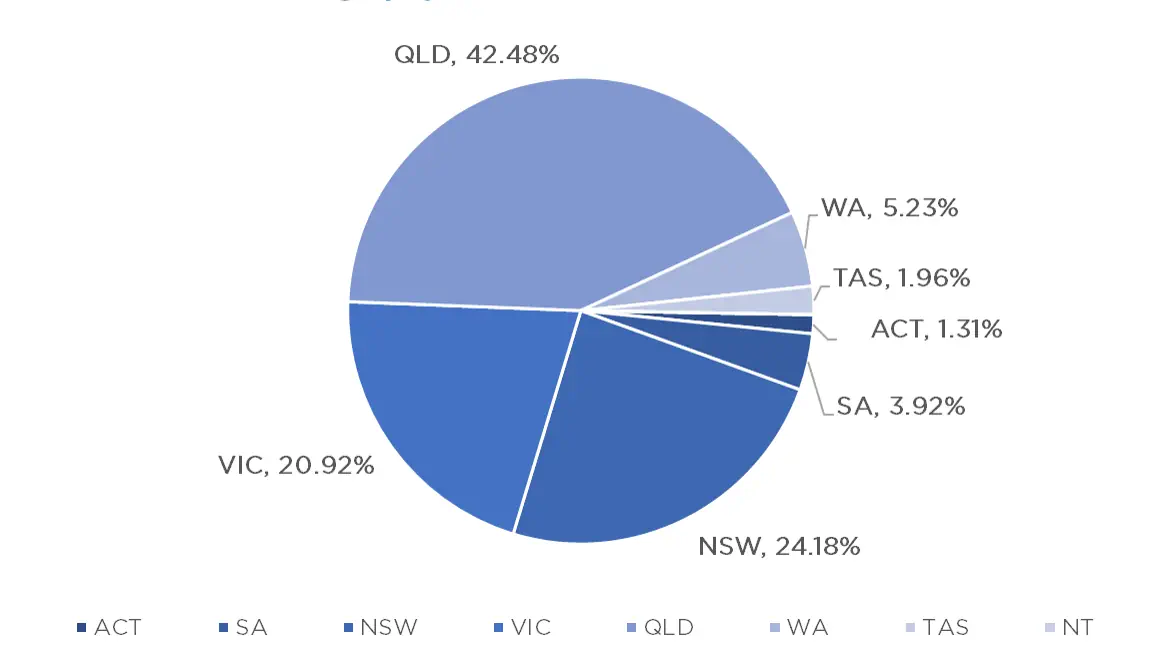

Current Loans Geography

as at 30th of June 2024

Why Invest with ASCF?

Why Pooled Mortgage Funds May Be a Better Choice Than Direct Property Investing

When considering real estate investment, individuals often choose between pooled mortgage funds and direct property investing. While both have their benefits, pooled mortgage funds offer several distinct advantages that make them appealing. Here, we’ll explore why pooled mortgage funds might be the better choice.

- Diversification

Pooled mortgage funds invest in a diversified portfolio of mortgages, spreading risk across multiple loans and properties. This reduces the impact of any single loan defaulting. In contrast, direct property investing ties an investor’s fortunes to the success of one or a few properties, leading to higher risk if those properties underperform. - Professional Management

Pooled mortgage funds are managed by experienced professionals who oversee the investments. This expertise leads to better risk management and improved returns, especially for investors lacking the time, knowledge, or resources to manage real estate investments effectively. - Lower Entry Barriers

Investing in a pooled mortgage fund generally requires a lower initial investment compared to purchasing a property outright. This makes pooled mortgage funds more accessible to a broader range of investors, including those without substantial capital. - Liquidity

Pooled mortgage funds typically offer higher liquidity compared to direct property investments. Investors can often redeem more easily, providing flexibility to access their capital when needed. In contrast, selling a property can be a lengthy process, tying up capital for an extended period. - Regular Income

Our pooled mortgage funds provide regular income distributions from the interest payments on the underlying mortgages. This steady income stream is attractive for those seeking consistent cash flow without managing rental properties. Direct property investing requires active management to ensure rental income. - Reduced Management Burden

Investing in pooled mortgage funds eliminates the hands-on management responsibilities associated with property ownership. Property investors must handle tasks like finding tenants, collecting rent, and maintenance. Pooled mortgage funds allow investors to benefit from real estate investments without the day-to-day management burden. - Risk Mitigation

Pooled mortgage funds offer risk mitigation through their structured investment approach. By spreading investments across multiple loans and properties, these funds cushion against localized market fluctuations and individual property issues. Direct property investing exposes investors to greater risk if a property loses value or incurs significant expenses.

Conclusion

Pooled mortgage funds offer numerous advantages over direct property investing, as shown in these previous points.

These benefits make pooled mortgage funds an attractive option for investors seeking a more hands-off, diversified, and flexible approach to real estate investment. While direct property investing has its own set of advantages, pooled mortgage funds provide a compelling alternative that can align better with the needs and preferences of many investors.

If you would like to know more about what we offer or want further information then please reach out to me on 0459 835 335.

An Interesting Transaction

Problem:

A borrower had purchased a large 87-acre parcel of land on Tambourine Mountain and commenced construction of a large, luxury home. He had a 1st mortgage to another private lender which was due to expire and required further funds to complete the construction.

Solution:

ASCF obtained a valuation report that provided an ‘as is’ figure and an ‘as if complete’ figure. Based on the ‘as is’ figure, ASCF was able to lend the borrower $1.97m to complete construction at a 70% LVR at 11.95% per annum on a six-month term. Funds were drawn in stages to help the borrower save on the overall interest expense.

The borrower then sought to vary the loan agreement to extend for a further six months due to delays and to provide additional funds as they wanted to vary some of the finishes to the dwelling and add some features to the property.

ASCF was able to obtain an updated valuation that provided an increased ‘as is’ figure due to the majority of construction now being completed. An additional $162,000 was advanced to the borrower at a reduced LVR of 33% based on the updated ‘as is’ valuation figure.

Upon completion, the property was marketed and taken to auction. The property was sold at auction with settlement due to take place in August 2024. Our very satisfied customer will realise a significant profit from the transaction.

What ASCF Does Differently:

ASCF is able to work with borrowers on their projects throughout the entire process to facilitate funding and completion. ASCF recognises that construction projects often change mid-way but with updated valuation reports and communication with the borrowers an optimal outcome can still be achieved.

Market Update

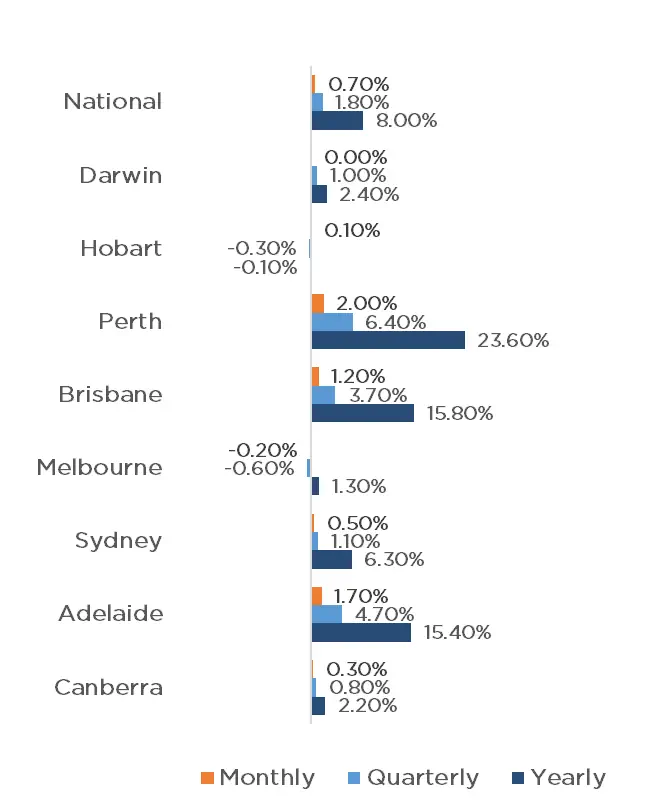

Property prices across the capital cities have risen yet again, bringing the 17th consecutive month of price growth with June’s 0.7% increase, taking growth to 8% across the nation for the 2023-24 Financial year. Yet again, Perth has experienced the largest growth with a further 2% increase, followed closely by Adelaide with 1.7% and Brisbane with a 1.2% increase.

Sydney, Canberra and Hobart also experienced growth, albeit it to a lesser degree, with 0.5%, 0.3% and 0.1% respectively. Property prices in Darwin remained stable, whilst Melbourne saw a reduction of 0.2%.

The financial year data is nearly all positive, with all capital cities experiencing growth, excluding Hobart which received a small reduction of 0.1% for the year. Perth, Brisbane and Adelaide all experienced growth well into the double digits, with Perth leading the way with a mammoth 23.6% increase, followed by Brisbane and Adelaide with 15.8% and 15.4% respectively. Sydney, Darwin, Canberra and Melbourne also finished the year in the positive, with 6.3%, 2.4%, 2.2% and 1.3% respectively. Growth wasn’t just experienced in the capitals, with the regions also increasing by 7%.

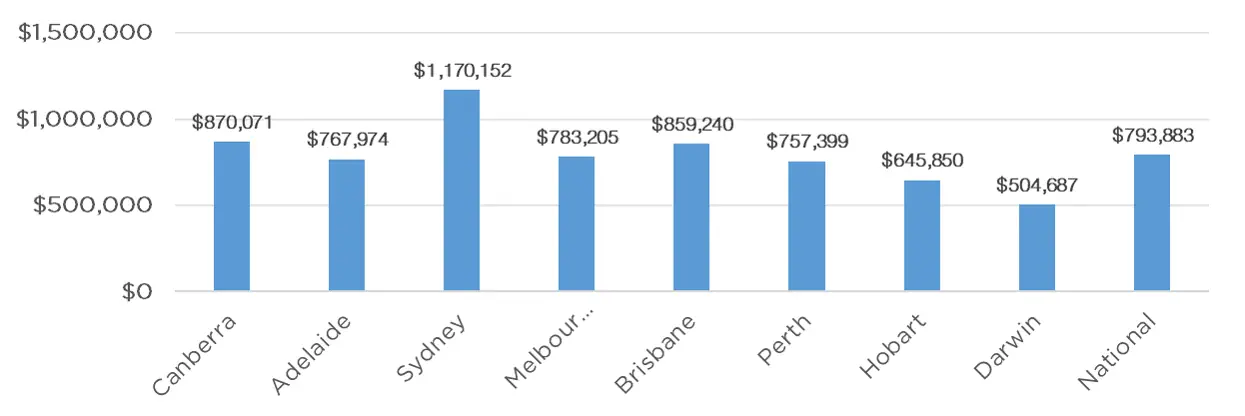

Property Values

as at 30th of June 2024

Median Dwelling Values

as at 30th of June 2024

Quick Insights

Larger Loans

The average new owner-occupier home loan is at $626,055 nationally, hitting a record high, as the growth housing markets of Perth, Brisbane and Adelaide surge higher, according the latest official lending figures.

“It’s astounding to think owner-occupiers are, on average, taking out larger loans than ever before despite the fact the cash rate is sitting at a 12-year-high.”, said Sally Tindall, research director at comparison website, RateCity.com.au.

Source: Australian Financial Review

Construction Costs & Increasing Interest Rates

High interest rates and construction costs are now choking off the supply of new housing.

High construction costs in particular are being singled out amid a complex mix of factors that have pushed up the cost of building in most capital cities.

“There has been some relief in access to inputs and labour, and in the prices of some early-stage inputs, but labour costs remain elevated and the regulatory burden high.”, investment banking firm Barrenjoey’s chief economist Jo Masters said.

Source: Australian Financial Review