Trading Update

The release of Australia’s inflation data for the June quarter yesterday has now provided the RBA with the confirmation it required to lower rates at its next meeting on August 12.

The headline inflation number fell from 2.4% to 2.1% between March and June its lowest point since March 2021 while the “trimmed mean” which is the Reserve Bank’s preferred measure of underlying inflation fell from 2.9% to 2.7%.

The question now is how much further will the RBA cut rates from here. With the unemployment holding steady at 4.1% and inflation now tamed market consensus is for the RBA to continue to cut rates further over the course of the year to 3.1% implying a further two cuts of 0.25% later this year which should assist in further boosting consumer confidence which is showing early signs of recovery.

Property market activity has also picked up pace, with capital city auction volumes and clearance rates both rising to their highest levels this year. While affordability challenges persist, tight supply and consistent demand are helping to underpin prices in many markets. With borrowing conditions easing, buyer sentiment is improving and we expect this to continue to improve as the RBA continues to cut rates.

In response, ASCF continues to see a strong pipeline of lending opportunities — particularly from borrowers seeking fast and flexible short term funding solutions. Our focus remains on disciplined loan selection and active risk management to help deliver consistent outcomes for our investors across all our funds.

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.00% | 7.50% | 7.10% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.00% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Managed Funds Under Management

as at 30th of June 2025

| June 2025 | |

|---|---|

| ASCF High Yield Fund | $178,124,399.93 |

| ASCF Select Income Fund | $50,202,536.22 |

| ASCF Premium Capital Fund | $28,241,390.82 |

| ASCF Private fund | $39,675,026.81 |

| Combined Funds under Management | $296,243,353.78 |

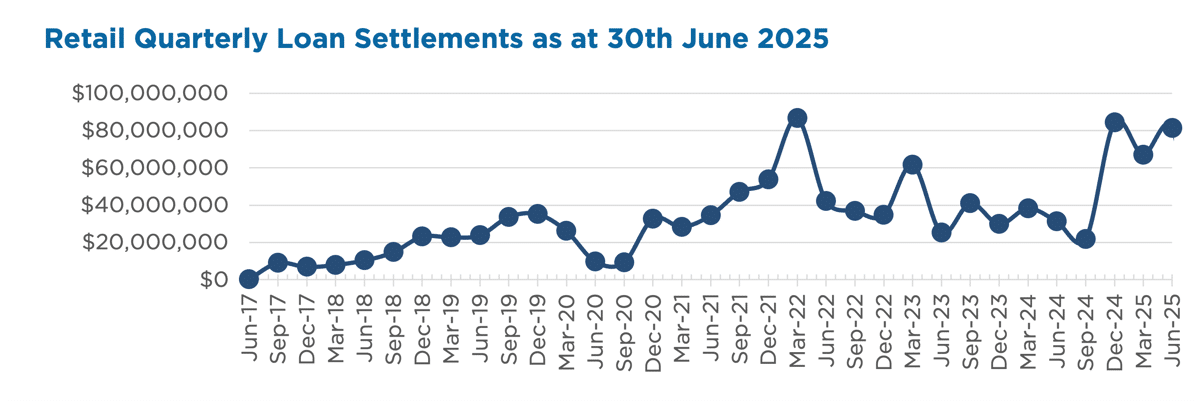

In June, loans and inquiry levels were steady, with $14,679,225.48 in loans settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of June.

Lending Activity Update

Quarterly Loan Settlements

as at 30th of June 2025

Current Loans by Fund Source

as at 30th of June 2025

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 73.62% | 100% | 100% |

| 2nd Mortgage Loans | 17.63% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 8.75% | 0% | 0% |

| Avg. Weighted LVR | 54.13% | 45.30% | 55.77% |

| Avg. Loan Size | $1,338,877.57 | $891,771.47 | $886,129.31 |

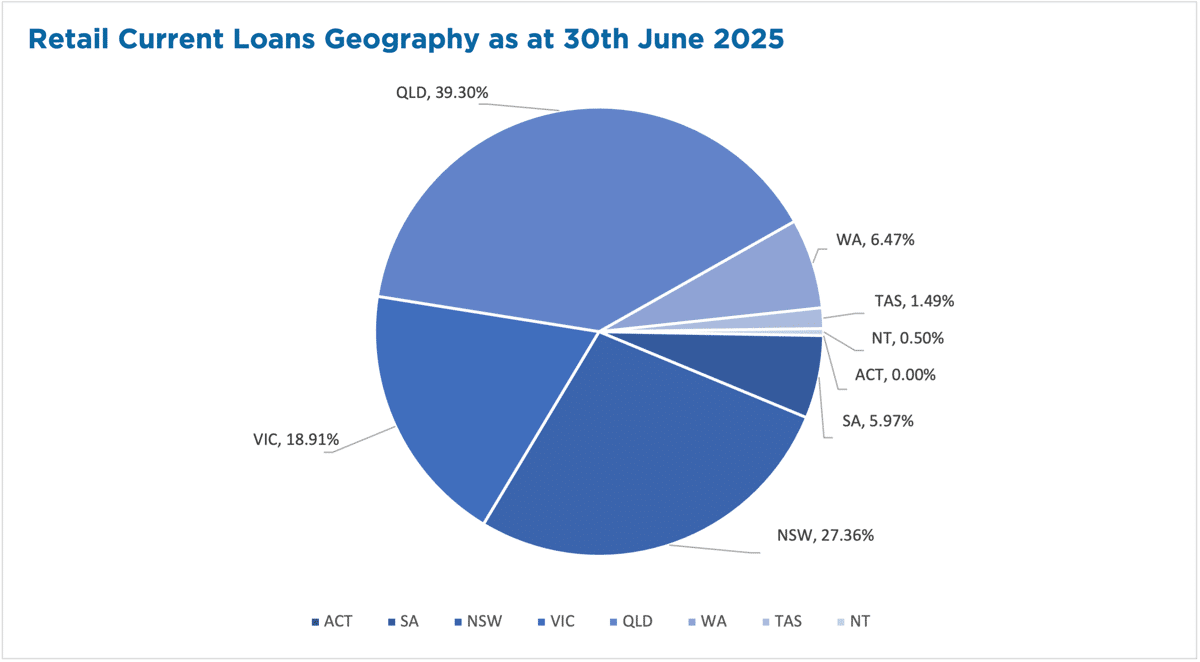

Current Loans Geography

as at 31st of June 2025

Why Invest with ASCF?

Why Sitting on Cash Could Be Costing You

When inflation rises, your savings may not go as far—because even if your balance stays the same, its buying power can shrink. If inflation is 5% and your money isn’t growing at a similar pace, you’re effectively losing value. That’s why many investors are exploring alternatives.

While no investment is without risk, certain options aim to deliver income above the inflation rate—helping preserve (and potentially grow) your wealth in real terms. The key is understanding your financial goals, risk appetite, and time horizon.

An Option to Consider: The ASCF High Yield Fund

Our High Yield Fund is currently targeting:

- 7.50% p.a. for a 12-month investment term, or

- 7.10% p.a. for a 24-month investment term

- With monthly income distributions

Target distribution rates apply for the full investment term you select. Minimum investment from $5,000. Terms from 3 to 24 months. Loans are backed by registered mortgages over real property.

Have questions? Our team is here to help.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A husband and wife running a cabinet-making business in Victoria faced cash flow challenges after a key client’s liquidation, resulting in missed home loan payments. With new contracts secured, they urgently needed capital to purchase materials and fulfil these commitments.

Solution:

ASCF delivered a tailored 2nd mortgage solution, enabling the business to address mortgage arrears and secure the inventory required for new contracts. Through a $256,000 loan, fully capitalised over 12 months at 16.95% p.a., we provided the certainty needed for the owners to resume growth with a view to refinancing. The facility was structured at a 63.92% loan-to-value ratio, validated by a panel valuation after consideration of ANZ’s primary mortgage.

What ASCF does differently

| ASCF understands that sometimes plans are impacted by unexpected events. But with the necessary timely financial support, businesses can again thrive and grow. |

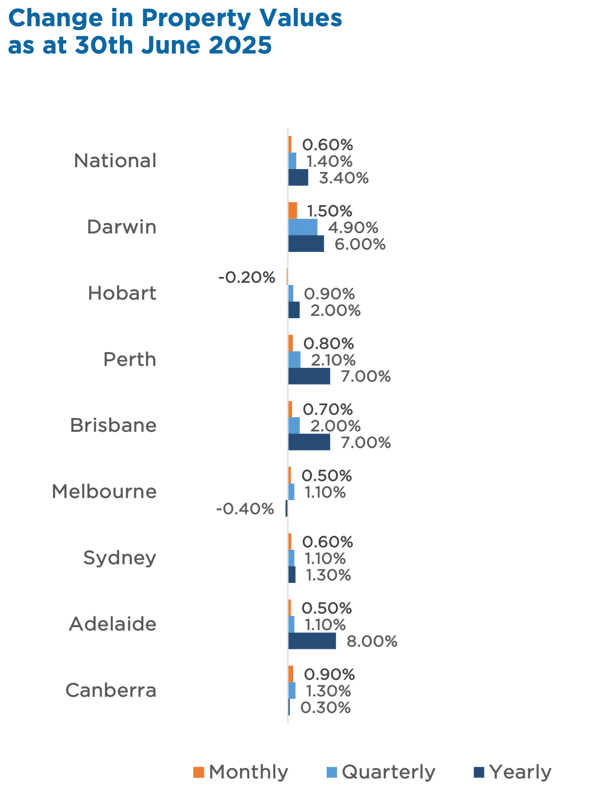

Market Update

Australian housing values rose 0.6% in June, marking five straight months of growth. The June quarter saw a 1.4% national increase, with gains across most capital cities – driven by falling interest rates and low advertised stock.

Key highlights:

- Brisbane (+2.0%), Perth (+2.1%) and Darwin (+4.9%) led quarterly capital city growth

- National dwelling values are up 3.4% year-on-year

- Buyer demand remains steady, while advertised supply is 5.8% lower than last year

- Consumer sentiment is improving alongside expectations of further rate cuts in 2025

Despite affordability constraints and economic uncertainty, tight supply and easing rates continue to support modest value growth across Australian markets.

Property Values

as at 30th of June 2025

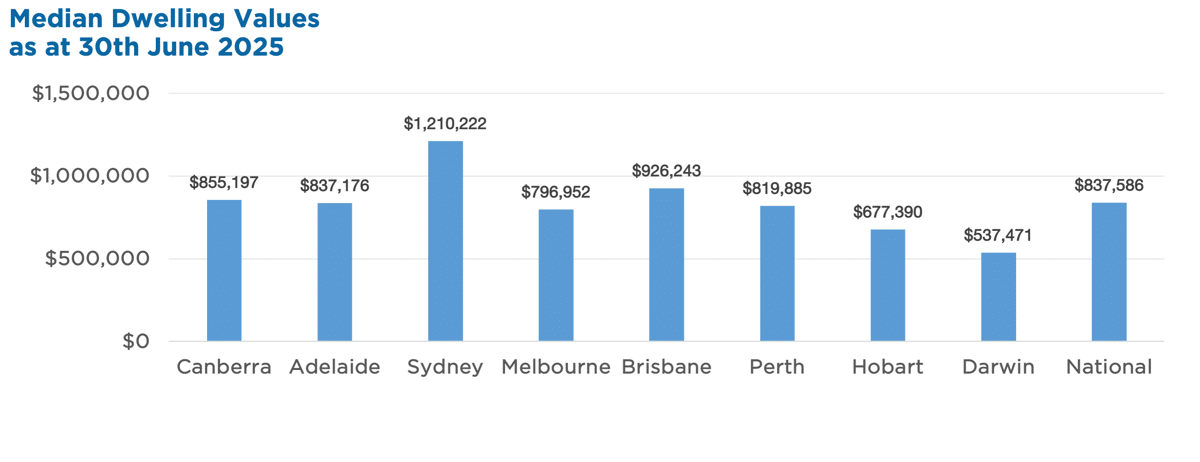

Median Dwelling Values

as at 30th of June 2025

Source: Cotality HVI, 1 July 2025