We’re back with another investor’s update for March 2026, analysing all the key economic and investment trends from the past month.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

As forecasted in our last update, the RBA again increased the official cash rate by 25 basis points in March, bringing the cash rate to 4.1%. Unlike February’s unanimous decision, the board’s March decision passed with a 5-4 majority, marking the narrowest margin since the RBA started publishing unattributed votes in July 2025.

With events in the Middle East continuing to add volatility to the situation, all eyes now turn to the ABS Q1 CPI data release next Wednesday. This will be crucial ahead of the RBA’s next meeting on the 4th of May, a week before the Federal Budget release on the 12th of May, with experts divided in their forecasts.

Future Prospects

Currently, market consensus among the Big Four banks forecasts a further 0.25% rate rise in May. However, the tone of these forecasts differs, with CommBank noting that the decision is “a line ball” and NAB stating “there is considerable uncertainty around any point forecast at this time.”

In contrast, Westpac has adopted the most hawkish stance, predicting three further 0.25% rises in May, June, and August, bringing their expected peak cash rate to 4.85%. If this comes to fruition, it would mark the highest cash rate since November 2008. Westpac’s prediction is underpinned by “the surprisingly rapid pass‑through of higher fuel and other oil‑derived product prices into other prices in Australia.”

Property & Employment Markets

The Australian property market continued to be notably ‘two-speed’ in March. Values in Melbourne and Sydney decreased slightly for the second straight month, whereas Perth posted a third consecutive monthly gain of greater than 2%, with Brisbane, Adelaide, and Darwin also posting monthly gains of greater than 1%.

There are also some early indicators of an ease in purchasing demand, with Cotality’s estimated quarterly home sales down 5.6% on the five-year average in February.

Additionally, unemployment increased by 0.2% in seasonally adjusted terms, rising from 4.1% in January to 4.3%. The CPI also rose by 0.2% month-on-month in seasonally adjusted terms in February, with housing (+0.7% seasonally adjusted) being the largest contributor, and the trimmed mean remaining at 3.3%.

How ASCF Helps

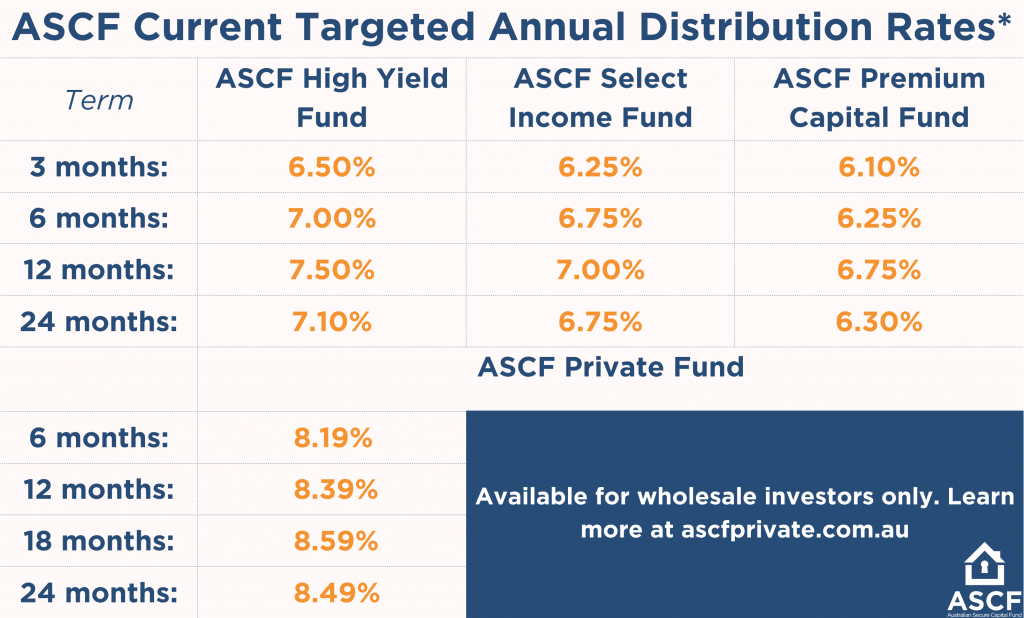

Despite shifting RBA forecasts and geopolitical volatility, ASCF’s funds provide an appealing alternative to fluctuating variable-rate assets. Our ASCF High Yield Fund offers a targeted distribution rate of 7.50% per annum for a 12-month fixed term, with interest paid monthly.

Sources: Australian Fund Monitors, Bloomberg, Investing.com

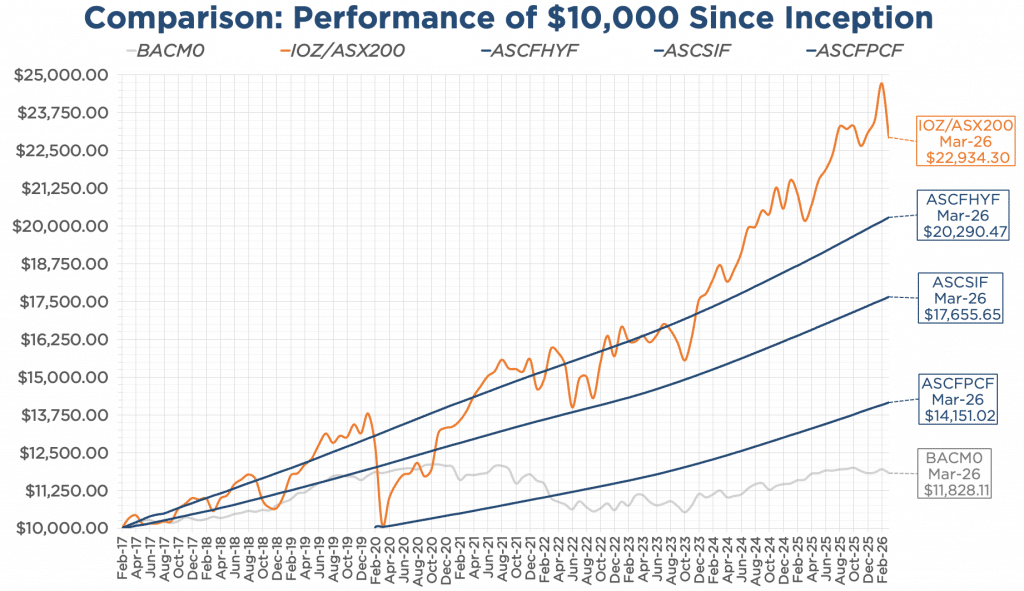

Note 1: Premium Capital Fund began in February of 2020

Note 2: Past performance is not indicative of future performance.

To learn more, see our Investor FAQs.

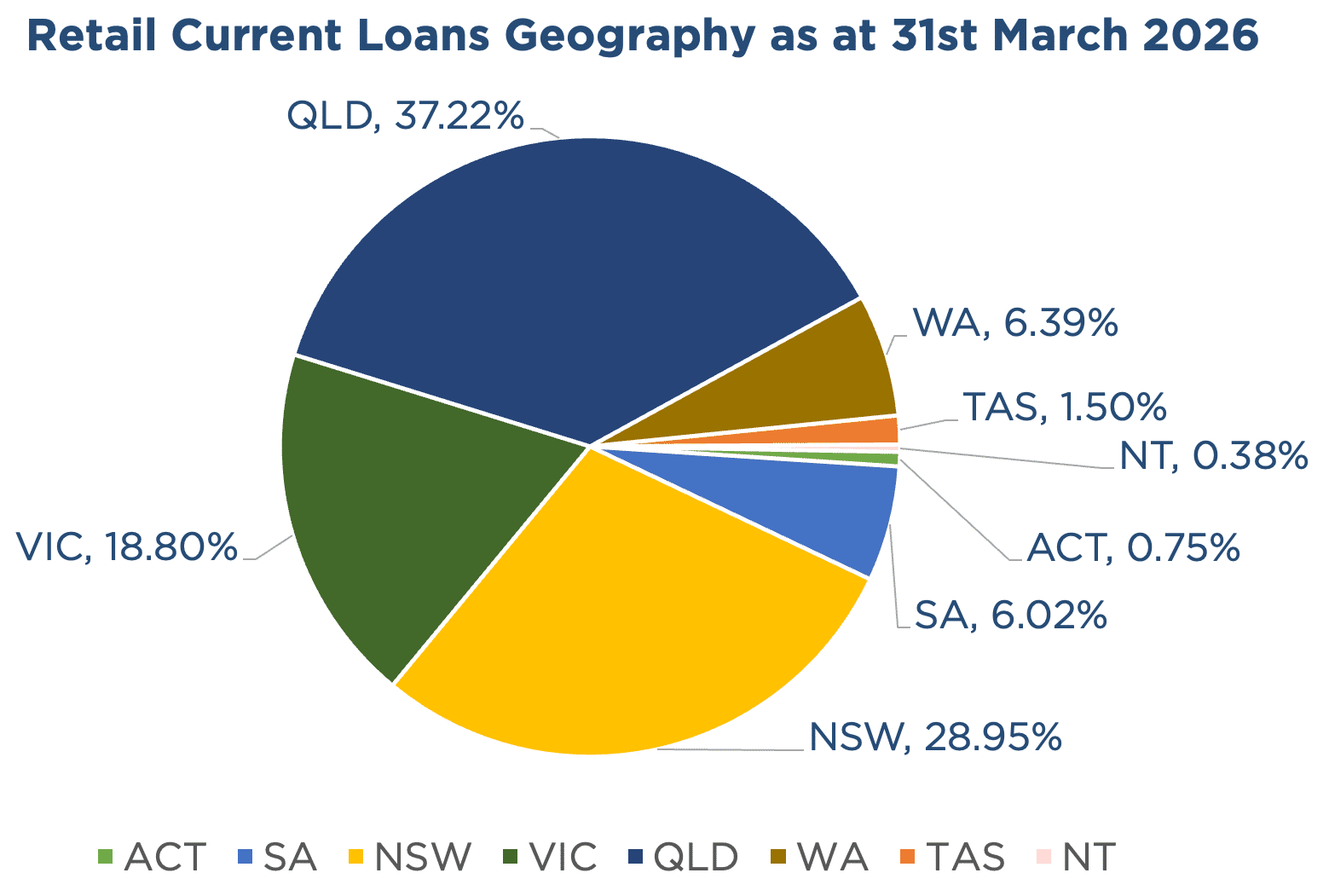

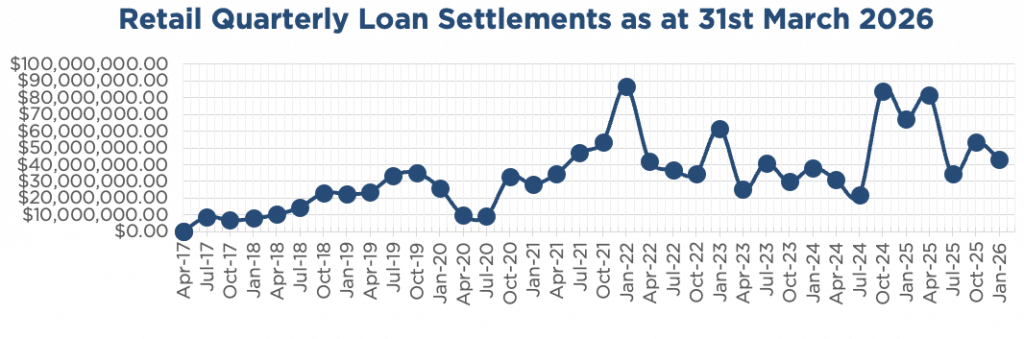

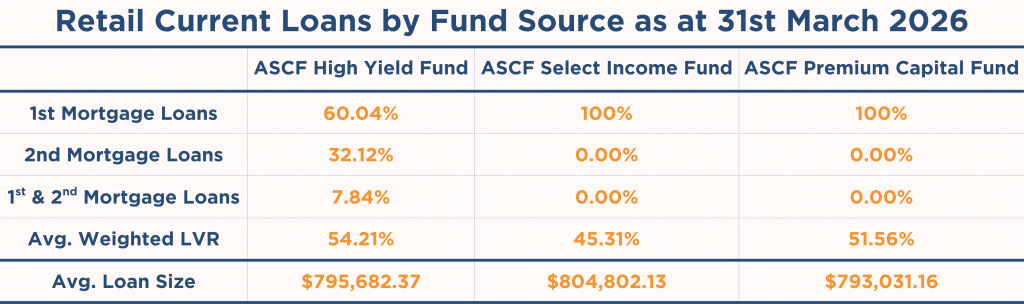

Lending Activity Update

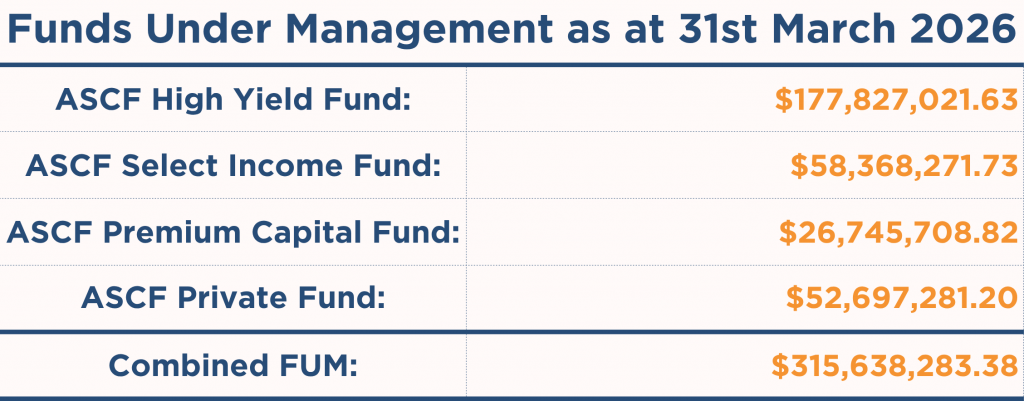

In March, inquiry levels were robust with $19,572,468.74 in loans settled.

The unit price across all three of our retail funds remains at $1.00 per unit.

All monthly distributions have been paid in full for March.

To learn more, see our Borrower FAQs or see our Loan Summary as at 31st March 2026.

Why Invest With ASCF?

A Beginner’s Guide to Pooled Mortgage Funds

A Beginner’s Guide to Pooled Mortgage Funds

For many investors, striking the right balance can be challenging, particularly in a world of uncertain global conditions. Considering this, one Australian-based investment option that has been steadily gaining attention are pooled mortgage funds. But what exactly are they, and how do you get started? Let’s break it down.

What Is a Pooled Mortgage Fund?

A pooled mortgage fund is an investment where your money is combined with other investors’ funds and used to provide loans, which are typically short-term and secured by real estate.

Unlike direct mortgage syndicates, where you fund a single loan, a pooled fund spreads your investment across a diversified portfolio of multiple loans. This diversification helps reduce risk while aiming to generate returns from the interest paid by borrowers.

How Do They Work?

- Investors contribute funds to a managed pool for a set term.

- The fund manager lends this money to borrowers, subject to strict criteria regarding property value, asset type, and the loan purpose.

- Borrowers pay any initial establishment costs and interest on their loans.

- The fund distributes this income to investors—usually monthly.

The short-term nature of the loans and the underlying property security are key structural features of a pooled mortgage fund.

Why Investors Are Considering Mortgage Funds

There are a few reasons these funds are becoming more popular:

Asset-Backed Security

Loans are typically secured against residential property with conservative LVRs to provide a protective equity buffer for investors.

Diversification

Investments are spread across multiple loans, reducing exposure to any single borrower or property security.

Lower Volatility

The underlying Australian residential real estate market has historically shown lower volatility due to demand and supply constraints.

What to Look for in a Fund

If you’re considering investing, some key factors to assess include:

- Loan-to-Value Ratios (LVRs) – Lower LVRs generally mean more conservative lending.

- Diversification – How many loans and borrowers are in the fund?

- Management Experience – The expertise of the team managing the fund is critical.

- Transparency and Reporting – How often does the fund provide updates on portfolio performance, and are the audited financial statements easily accessible?

Final Thoughts

If you’re considering investing in a pooled mortgage fund, get a copy of our PDS and read through it, highlight any areas that require further explanation, and speak to an investment manager, as they are there to give you clear answers to your questions.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker reached out to us last October with two clients seeking to downsize from their family home into a more manageable property for their retiree lifestyle. The borrowers, who were on a fixed retiree income, couldn’t find a major lender to assist them in bridging the gap due to their lack of serviceability for the peak debt during the bridging period.

As such, the clients were faced with the dilemma of either putting a contract down on the property they wanted to buy and hoping their current property sold within 60 days or finding temporary accommodation during the interim and moving all their belongings twice.

Solution:

By using a common-sense approach, ASCF assessed that the sale proceeds provided a definitive exit strategy. Accordingly, with expert insight from registered local agents and comparable sales across the area, the combined LVR was assessed at 47.65% across both securities. ASCF provided a $1.62 million loan at 9.75% p.a. over a 4-month term.

Ultimately, interest was capitalised into the loan facility, eliminating the need for ongoing cash-flow payments during the term and allowing the borrowers to focus on moving into their dream home without the urgency of forcing a sub-optimal sale.

What ASCF Does Differently:

The ‘bullet’ repayment strategy is the backbone of ASCF’s lending product suite, helping real-world borrowers in a finance industry often restricted by rigid amortisation schedules.Where traditional lenders come up short, ASCF makes a difference.

For more details about this transaction, see our Loan Summary.

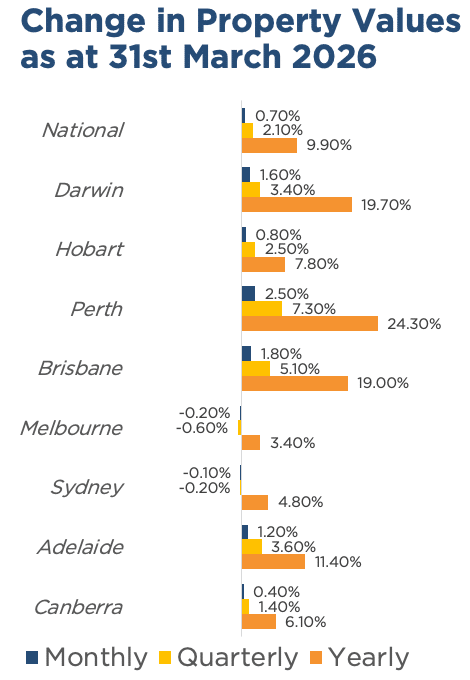

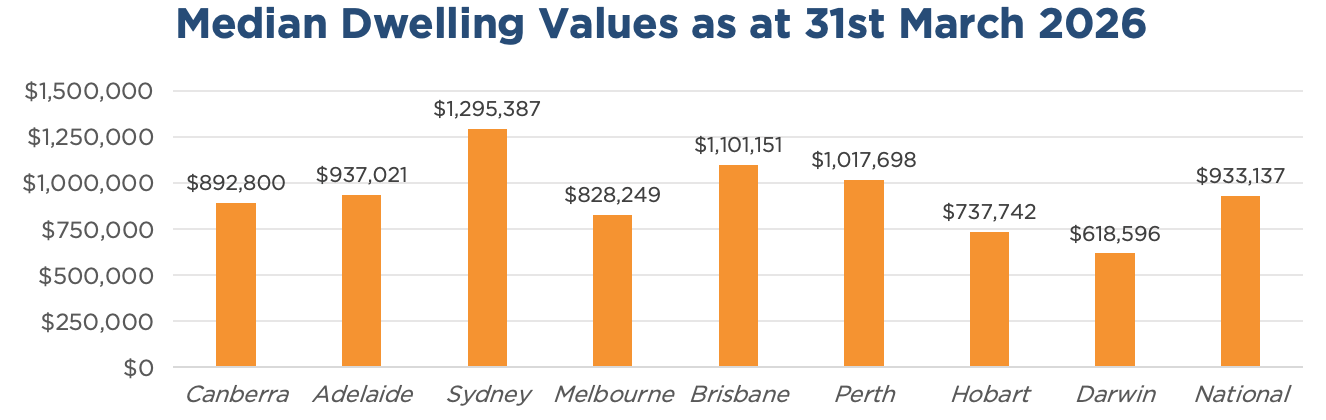

Property Update

March was another steady month for Australian property values, posting a national rise of 0.7%, down slightly from 0.8% in February.

Once again, Perth (+2.5%) led the way with a third consecutive monthly rise of greater than 2%, with the annual increase now reaching 24.3%. Likewise, Brisbane (+1.8%) and Adelaide (+1.2%) continued to add value, again posting monthly increases of greater than 1%.

Conversely, values in Melbourne (-0.2%) and Sydney (-0.1%) declined for a second straight month, with the cities notching rolling quarterly declines of -0.6% and -0.2%, respectively.

Due to this, regional areas (+1.1%) continue to outpace the capitals (+0.6%) by nearly double, with regional WA leading the way, posting a 6.2% quarterly increase.

Source: Cotality HVI, 02 April 2026