We’re back with another ASCF investor’s update, analysing all the key economic and investment trends from the past month, from the property market to RBA prospects and beyond.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

As anticipated in our previous update, the RBA have unanimously elected to hold the official cash rate at 4.35% following their June meeting. After three consecutive rises, this marks the first time in 2026 that the RBA has elected not to increase the official cash rate.

Future Prospects

The Board will next meet on August 11th, with three of the Big Four banks forecasting that they will hold the cash rate at 4.35% for the foreseeable future.

Specifically, CommBank says that they now “do not expect the RBA to alter course until the first half of next year.” ANZ have taken a similar neutral stance, noting that the RBA’s post-meeting minutes for May “point to a pause.”

Having earlier predicted further rises in June and August, NAB have now abandoned their tightening forecast, stating, “[we] now see the cash rate peaking at the current rate of 4.35% for the cycle. The next move in the cash rate is likely to be down, but the timing is uncertain.”

Westpac remains the hawkish outlier, continuing to forecast two further rate rises in August and September. Specifically, they expect the Board will be “less swayed by some of this softer data than some observers might assume”, adding, “we therefore retain our view that further rate hikes will occur in the following meetings (August and September).”

Property Market

Following recent RBA decisions, the ongoing Middle East tensions, and last month’s Federal Budget release, Cotality’s May HVI has shown early signs of a slowdown in housing demand.

Nationally, the estimated number of home sales over the past three months was 2.2% lower than in May 2025 and 4.1% below the five-year average. Primarily, this has been driven by a 17% drop in estimated sales in Sydney and a 14.2% drop in estimated sales in Melbourne compared to the same time last year.

Even so, the market remains distinctly two-speed, with some areas currently experiencing above-average demand, and Cotality warning that “conditions are likely to remain uneven across regions and price points through the remainder of 2026.”

How ASCF Helps

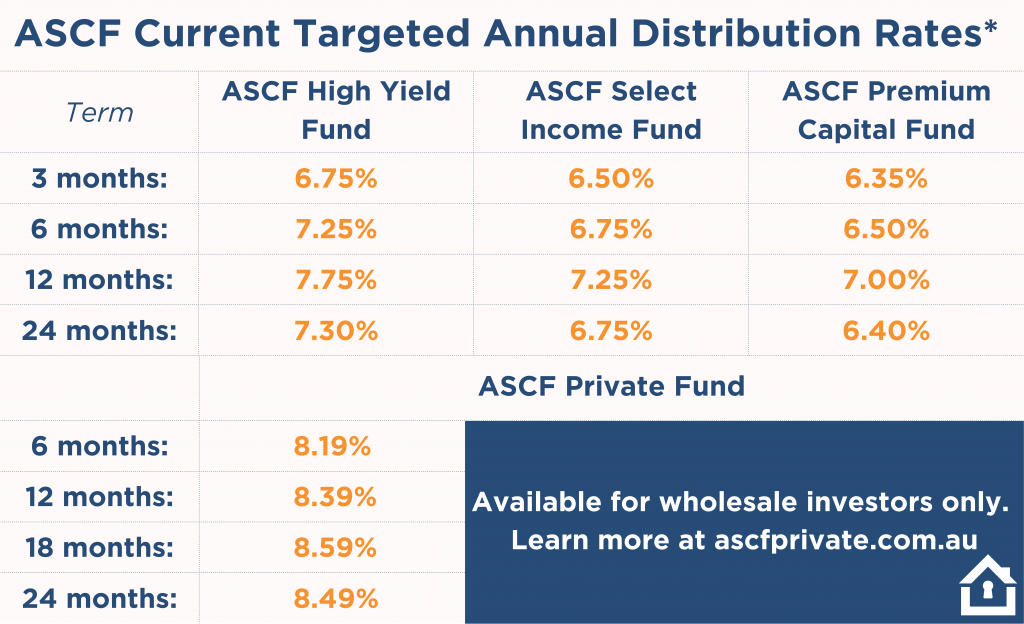

Despite shifting RBA forecasts and geopolitical volatility, ASCF’s funds provide an appealing alternative to fluctuating variable-rate assets. Our ASCF High Yield Fund offers a targeted distribution rate of 7.75% per annum for a 12-month fixed term, with interest paid monthly, and is worth considering as part of any diversified investment portfolio.*

Sources: Australian Fund Monitors, Bloomberg, Investing.com

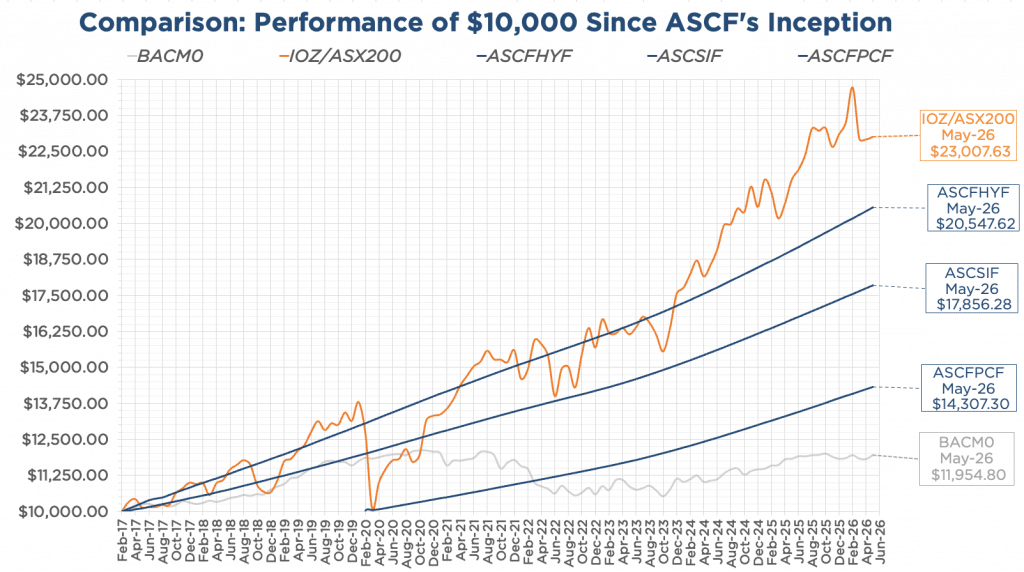

Note 1: Premium Capital Fund began in February of 2020

Note 2: Past performance is not indicative of future performance.

To learn more, see our Investor FAQs.

Lending Activity Update

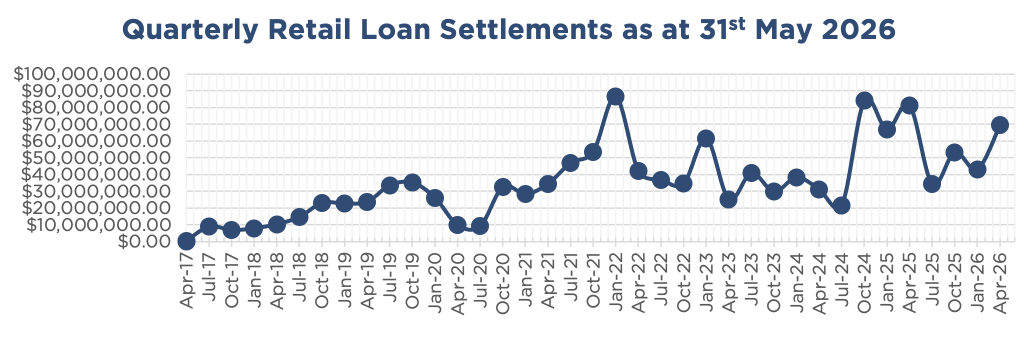

In May, inquiry levels were robust with $37,268,588.96 in loans settled.

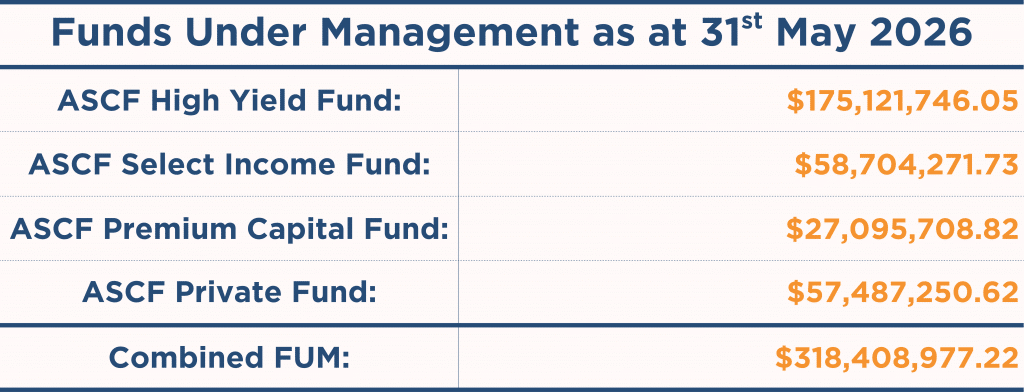

The unit price across all three of our retail funds remains at $1.00 per unit, and all monthly distributions have been paid in full for May.

To learn more, see our Borrower FAQs or visit our Loan Summary as at 31st May 2026.

Why Liquidity Matters in a Mortgage Fund

At ASCF, we have built a reputation as one of Australia’s leading short-term mortgage funds. Every loan we provide is secured by a registered mortgage over Australian residential, vacant, or commercial property. Importantly, we do not participate in certain lending sectors, such as construction finance, property development projects, high-rise apartment developments, unsecured personal lending, vehicle finance, or equipment loans.

This disciplined approach has helped ASCF maintain strong risk-management practices, particularly in liquidity management.

The Importance of Liquidity

One of the strengths of ASCF’s Mortgage Funds is our commitment to maintaining Fund liquidity. Typically, 5–10% or more of the Fund’s value is held in liquid assets to assist with investor withdrawals, monthly distributions, and operational expenses.

Effective liquidity management plays a critical role in the resilience and long-term performance of any mortgage fund. For investors, this can provide several important advantages:

Risk Management Through Market Cycles

Liquidity management is a core component of overall risk management. Maintaining appropriate reserves helps the Fund navigate periods of market volatility, economic uncertainty, and changing conditions with greater confidence.

Reduced Redemption Risk

A well-managed liquidity position allows the Fund to meet withdrawal requests without needing to sell loan assets under pressure. This can help reduce the risk of forced asset sales that could negatively impact investor returns.

Consistent Unit Pricing

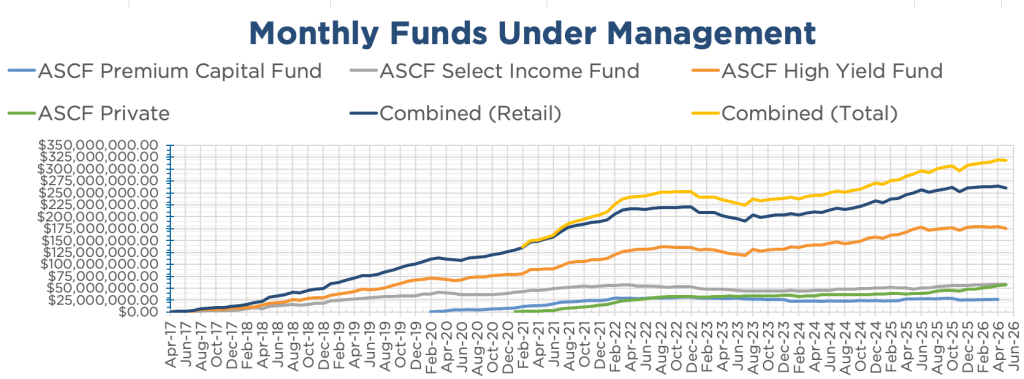

ASCF is proud to have maintained a unit price of $1.00 per unit since inception, reflecting our ongoing commitment to prudent Fund management.

Flexibility to Capture Opportunities

Strong liquidity also enables the Fund to respond quickly to quality lending opportunities as they arise. This flexibility can support enhanced yield opportunities and improved long-term outcomes for investors.

A Disciplined Approach to Investing

For investors considering mortgage funds, understanding how a fund manages liquidity is vital to assessing both risk and long-term performance potential. At ASCF, our disciplined lending practices and proactive liquidity management continue to underpin our commitment to delivering short-term lending solutions.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker reached out to ASCF on behalf of clients looking to consolidate high-interest business loans, clear an overdue ATO tax debt, and secure additional working capital without impacting their operational cash flow. The borrowers had previously utilised multiple unsecured facilities to fund the start-up and growth phases of their business, which was now placing pressure on their monthly servicing.

Solution:

By leveraging the strong residual equity in the clients’ Springrange, NSW property, ASCF provided a 12-month, 2nd mortgage loan of $323,000 at a 25.97% LVR at 16.95% per annum.

This facility allowed the clients to absorb their unsecured debts and ATO arrears into a single, more manageable repayment structure, protecting their credit file from impending defaults.

Crucially, the 12-month term provided the business with the necessary runway to improve monthly turnover, lodge their outstanding BAS, and complete their 2026 tax returns. This is ultimately designed to position them for traditional refinance options, which serves as the exit strategy before the expiry of the ASCF facility.

The ASCF Advantage:

ASCF’s ability to provide 2nd mortgages without disturbing a borrower’s existing 1st mortgage facility is a powerful tool for commercial debt consolidation.

Where traditional bank assessments can take weeks, ASCF focuses on rapid asset assessment. By identifying the client’s financial pressure points and structuring a facility that provides a genuine reduction in monthly obligations, ASCF can help growing businesses stabilise their cash flow and successfully transition back to mainstream lending.

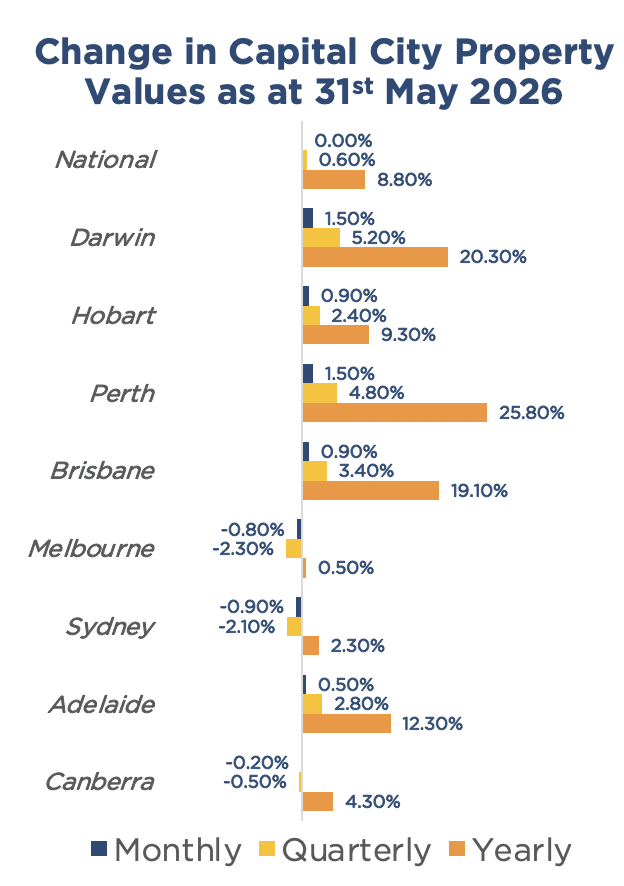

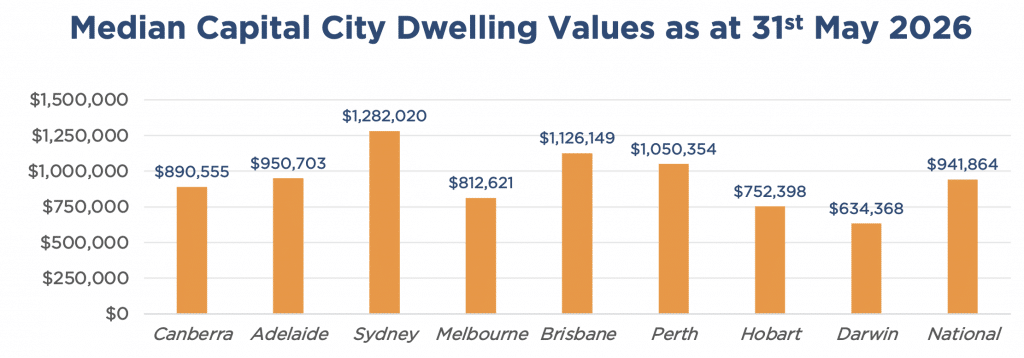

Property Update

May was another slow month for Australian property values, flatlining with no change in prices nationally. This marks the lowest monthly growth rate for Australian property values since January 2025.

Once again, Perth (+1.5%) led the way, however, there are signs of a slowdown, as this was the first time in 2026 that Perth home values have increased by less than 2% MOM. Dwellings in Brisbane (+0.9%), Adelaide (+0.5%), and Hobart (+0.9%) also continued to add value, though at a slower pace compared to the first quarter of 2026.

On the other hand, property values in Melbourne (-0.8%) and Sydney (-0.9%) declined for a fourth straight month, with values in Canberra (-0.2%) now also joining the slide.

Regional markets continue to show greater resilience in the face of this slowdown, posting a combined 0.6% increase in May, compared to a -0.1% decline for the capital cities.

Source: Cotality HVI, 01 June 2026