Trading Update

| The Reserve Bank of Australia (RBA) has once again shown a steady hand, holding the official cash rate at 3.60% at its September meeting. This decision signals a period of strategic observation, allowing the market to fully absorb the impact of the three prior rate cuts this year and assess forthcoming economic releases. This cautious approach is supported by a mix of encouraging and nuanced economic data. Inflation remains well-behaved, with the latest figures sitting comfortably within the RBA’s 2-3% target band. The Australian economy demonstrated greater-than-expected resilience in the June quarter, with a strong 0.6% expansion. However, the RBA is closely monitoring the labour market, which, despite a stable unemployment rate, is showing signs of moderating job creation evidenced by the recent unemployment data, which showed a jump in the unemployment rate to 4.5% for September in seasonally adjusted terms which is up from 4.3% in August. Most economists continue to forecast a 25-basis-point rate cut by May next year, taking the cash rate to 3.35%. Westpac remains the only major bank expecting an earlier cut next month, followed by two additional 0.25% reductions by mid next year. The positive momentum in the property market continues, driven by improved borrowing conditions. Auction clearance rates across major capital cities are robust, reflecting renewed buyer confidence and healthy market dynamics. This environment, characterised by strong demand and tight supply, creates a favourable landscape for our short-term, flexible lending solutions. Our High Yield Fund continues to perform strongly, offering a targeted distribution rate of 7.50% p.a. on a 12-month investment term. We maintain our disciplined approach to credit selection and active portfolio management, which remains central to delivering consistent and reliable outcomes for our investors. |

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.00% | 7.50% | 7.10% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.00% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

Managed Funds Under Management

as at 30th of September 2025

| September 2025 | |

|---|---|

| ASCF High Yield Fund | $174,830,729.93 |

| ASCF Select Income Fund | $54,144,271.73 |

| ASCF Premium Capital Fund | $29,724,221.99 |

| ASCF Private fund | $45,724,221.99 |

| Combined Funds under Management | $303,910,932.47 |

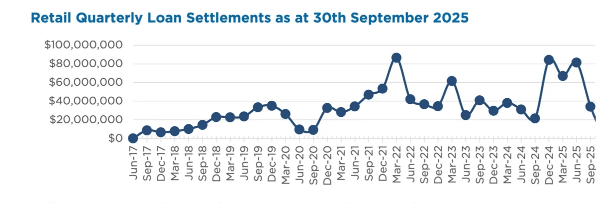

In September, loans and inquiry levels were steady, with $9,555,284.47 in loans settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of September.

Lending Activity Update

Quarterly Loan Settlements

as at 30th of September 2025

Current Loans by Fund Source

as at 30th of September 2025

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 74.76% | 100% | 100% |

| 2nd Mortgage Loans | 18.19% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 7.06% | 0% | 0% |

| Avg. Weighted LVR | 54.50% | 46.19% | 54.02% |

| Avg. Loan Size | $1,186,591.50 | $1,029,648.19 | $943,908.47 |

Current Loans Geography

as at 30th of September 2025

Why Invest with ASCF?

As Cash Rates Fall, Short-Term Mortgage Funds Gain Attention

With the cash rate reductions so far in 2025, investors may be wondering where the real opportunities lie. While borrowers will enjoy cheaper mortgages, the outlook for investors in short-term mortgage funds is increasingly relevant.

Why Short-Term Mortgages Benefit

Lower cash rates stimulate property activity — more buyers, more refinancing, more bridging finance. These situations often require short-term lending solutions, typically ranging from 6 to 24 months. As demand for these loans rises, mortgage funds that specialise in short-term lending may be able to deploy capital more frequently.

The Investor Advantage

For investors, ASCF short-term mortgage funds offer:

- Regular turnover of capital – shorter loan terms mean funds can recycle capital faster.

- Target distribution rates – which may be higher than some traditional income-focused options, depending on market conditions.

- Agreed rates for the chosen term – distributions are based on the target rate set at the start of the investment term.

- Loans secured by property – providing exposure to real-estate-backed lending.

Bottom Line

As the cash rate falls, demand for flexible, short-term borrowing is expected to rise. For income-focused investors, short-term pooled mortgage funds can provide diversification and exposure to increased loan activity in a low-rate environment.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker came to ASCF with a client who needed to settle the purchase of an investment property within a week. They had lodged an application with another bridging loan specialist prior to coming to ASCF, but that lender could not meet the deadline.

The borrower had a very strong assets and liabilities position, experience as a property investor, and sufficient income to support the exit strategy of refinance.

Solution:

ASCF was able to refinance one of the borrower’s existing investment properties and provide a first mortgage on the property being purchased. This provided sufficient funds to complete settlement and also fund renovations on the property being purchased.

The LVR across the two properties was 59.67%, with ASCF holding a first mortgage on both. Desktop valuations, supported by a local real estate agent’s appraisal of both properties, were used to confirm reliable valuation figures.

ASCF provided a total loan of $1,225,000 over a three-month term with an annual rate of 8.75%.

The urgent settlement date was met, and ASCF proved once again that it can meet deadlines that other lenders cannot.

What ASCF does differently

| ASCF recognised that this was a straightforward transaction for a strong borrower with a solid exit strategy. ASCF acted quickly to ensure the borrower did not miss settlement or lose their deposit. The practical valuation policy avoided lengthy delays, and loan documents were issued within two days of receiving a completed application form. |

Market Update

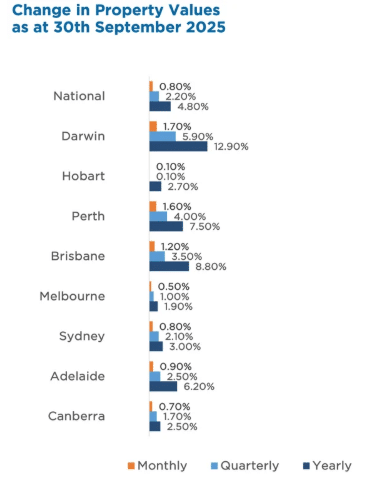

Australia’s housing market strengthened in September, with national dwelling values rising 0.8% — the fastest pace since October 2023.

Record-low listings are driving competition, with stock levels 53% below average in Darwin, 45% in Perth, and 31% in Brisbane, while auction clearance rates hold near 70%.

The Cotality Home Value Index climbed 2.2% over the quarter, adding about $18,000 to the median dwelling value. Growth was led by Perth, Brisbane, and Darwin, particularly in the unit market where supply remains tight.

With demand outpacing supply, prices continue to rise heading into spring, keeping momentum strong across all major markets.

Property Values

as at 30th of September 2025

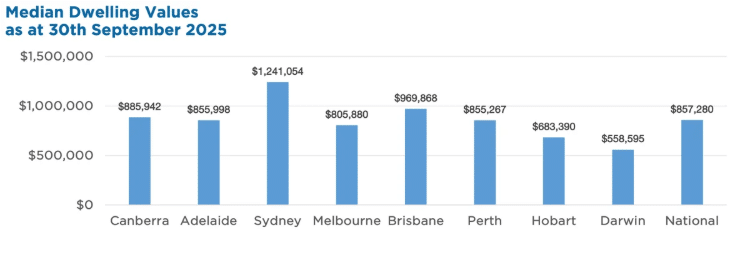

Median Dwelling Values

as at 30th of September 2025

Source: Cotality HVI, 1 Oct 2025