It’s time for another monthly investor’s update, this time, wrapping up November 2025.

You can catch up with past investor’s updates on the ASCF Blog. If you would like to receive these updates monthly via email, you can sign up to receive an Investor Pack here.

Trading Update

| As 2025 comes to a close, the Australian economy continues to show signs of continued upward momentum, with GDP growing by 0.4% in the September quarter and 2.1% on an annualised basis, compared to 0.8% a year ago. Residential property prices have increased by 11.3% nationally over the last 12 months, driven by ongoing sustained levels of migration, lower interest rates, and both State and Federal government assistance packages to first home buyers. The jobless rate held steady in November at 4.3%, and with underlying inflation coming in at 3.3% in the year to October, slightly above the RBA’s target range of 2%–3%, the RBA held rates steady at its December meeting last week. So what does this all mean for interest rates and property prices heading into 2026? At this stage, it appears that rate cuts are off the table until at least mid next year, and possibly later, with the possibility of rate increases now back on the agenda. However, any move will be data dependent, so the most likely scenario would be that rates now remain on hold for an extended period. Whilst higher interest rates would impact affordability should the RBA raise rates next year, we expect that residential property prices will remain stable, with a much slower pace of growth when compared to the previous 12 months. The country is still not delivering the housing it needs, and whilst governments continue to stoke demand through incentives, they continue to fail in addressing the supply issue, which is impacted by rising electricity costs, lack of labour, and environmental and bureaucratic red tape. As a consequence, we believe any rate rises which may occur next year will only result in a slowing of price growth, but not stall the growth momentum we have seen over the last 18 months. As this is our final newsletter for 2025, we would like to wish you and all your families a very Merry Christmas and a happy, healthy and prosperous New Year. To learn more, see our Investor FAQs. |

ASCF Current Targeted Distribution Rates

ASCF High Yield Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.50% | 7.00% | 7.50% | 7.10% |

ASCF Select Income Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 6.25% | 6.75% | 7.00% | 6.75% |

ASCF Premium Capital Fund

| 6 Months | 12 Months | 18 Months | 24 Months |

|---|---|---|---|

| 6.10% | 6.25% | 6.75% | 6.30% |

ASCF Private Fund

| 3 Months | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| 8.19% | 8.39% | 8.59% | 8.49% |

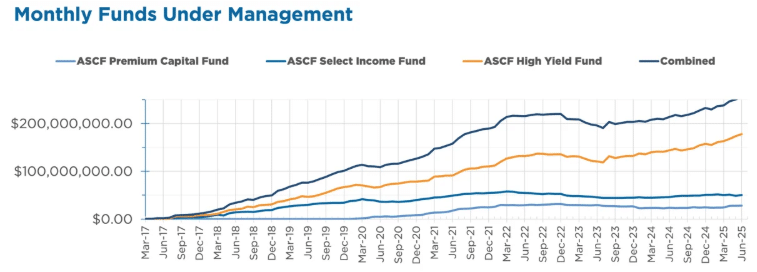

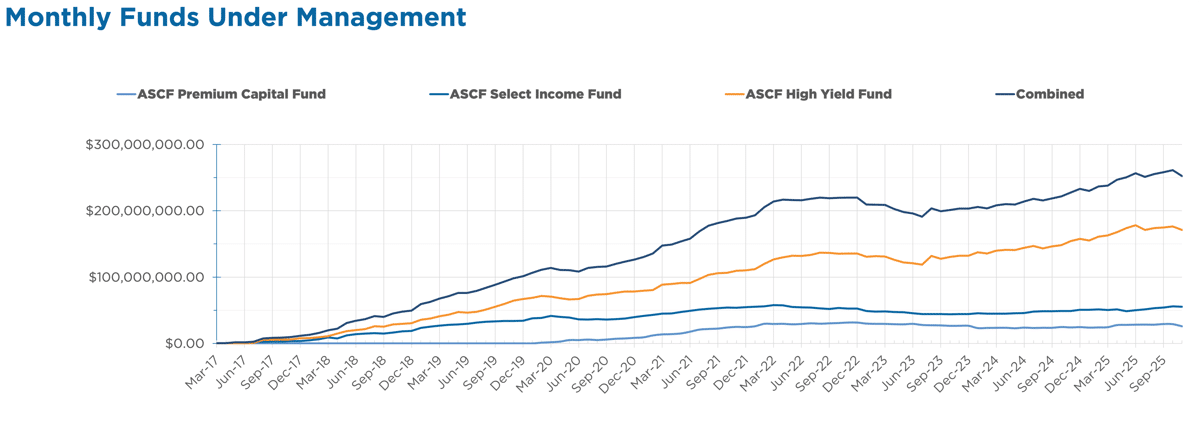

Managed Funds Under Management

as at 30th of November 2025

| November 2025 | |

|---|---|

| ASCF High Yield Fund | $176,213,664.67 |

| ASCF Select Income Fund | $55,892,271.73 |

| ASCF Premium Capital Fund | $29,016,708.82 |

| ASCF Private fund | $44,115,240.91 |

| Combined Funds under Management | $305,237,886.13 |

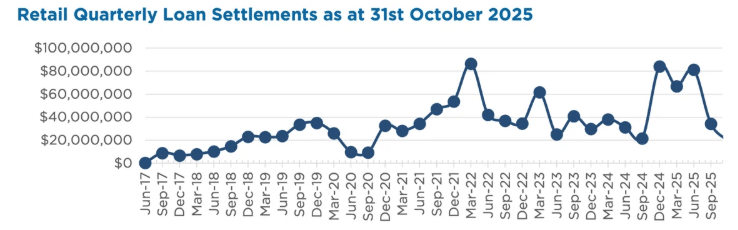

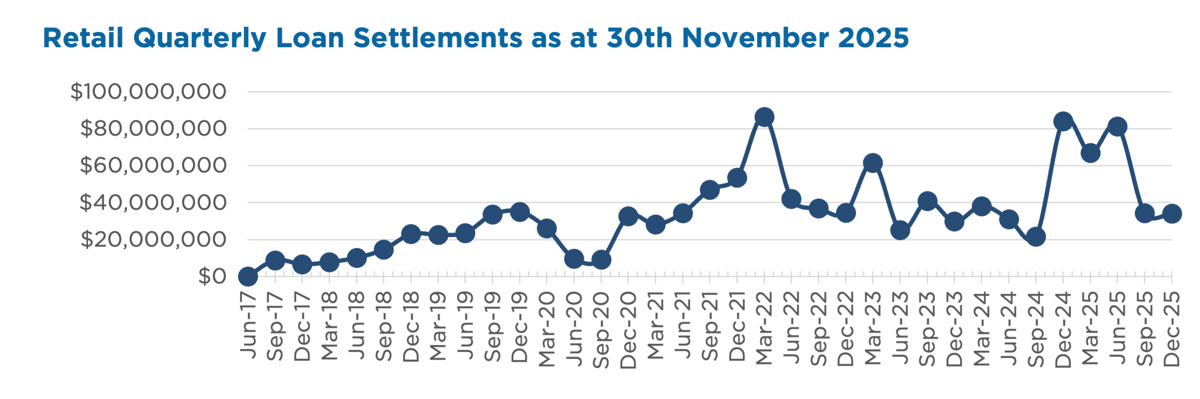

Lending Activity Updae

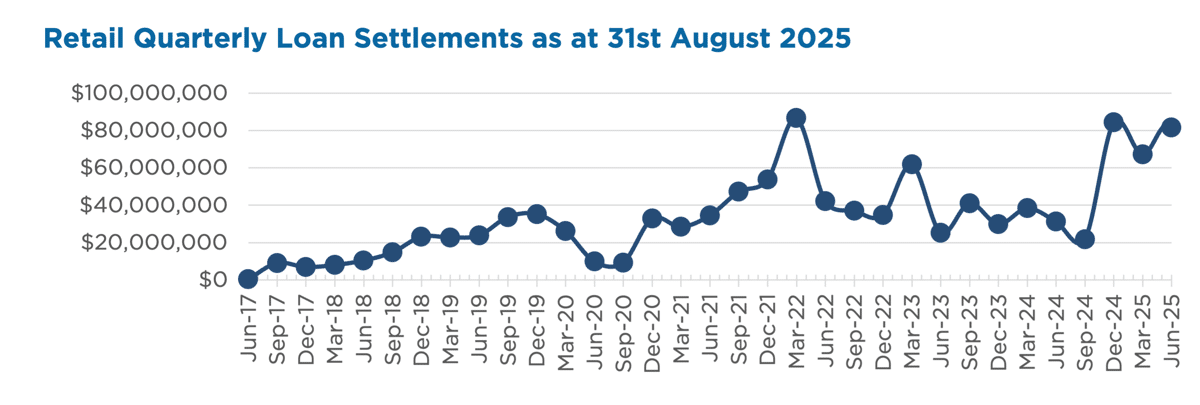

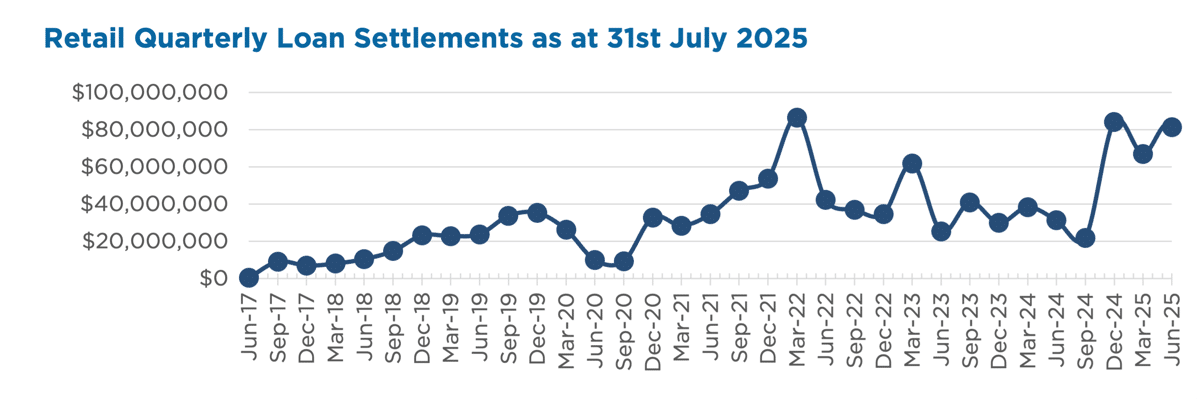

In November, loans and inquiry levels were up, with $15,110,604.67 in loans settled.

The unit price across all three of our retail funds remains stable at $1.00 per unit.

All monthly distributions have been paid in full for the month of November.

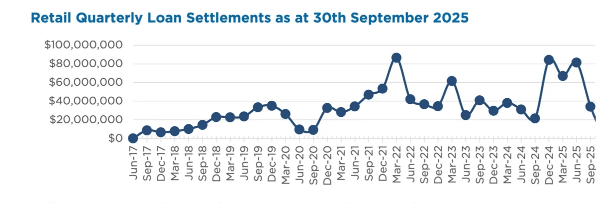

Quarterly Loan Settlements

as at 30th of November 2025

Current Loans by Fund Source

as at 30th of November 2025

| High Yield Fund | Select Income Fund | Premium Capital Fund | |

|---|---|---|---|

| 1st Mortgage Loans | 73.36% | 100% | 100% |

| 2nd Mortgage Loans | 20.46% | 0% | 0% |

| 1st & 2nd Mortgage Loans | 6.18% | 0% | 0% |

| Avg. Weighted LVR | 55.51% | 44.45% | 51.90% |

| Avg. Loan Size | $1,163,736.35 | $998,475.62 | $911,086.87 |

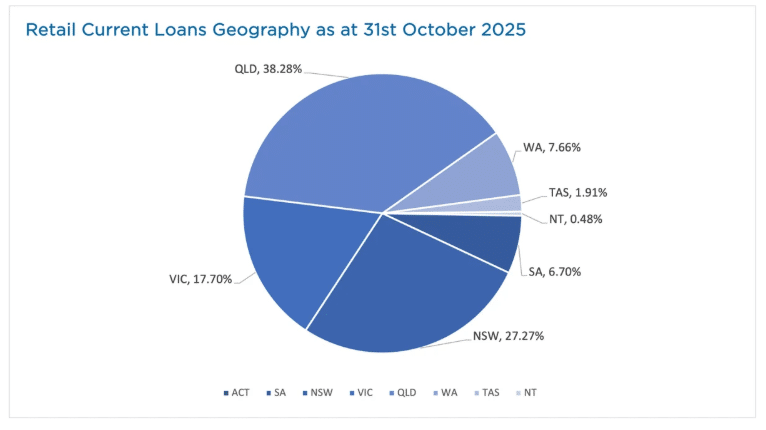

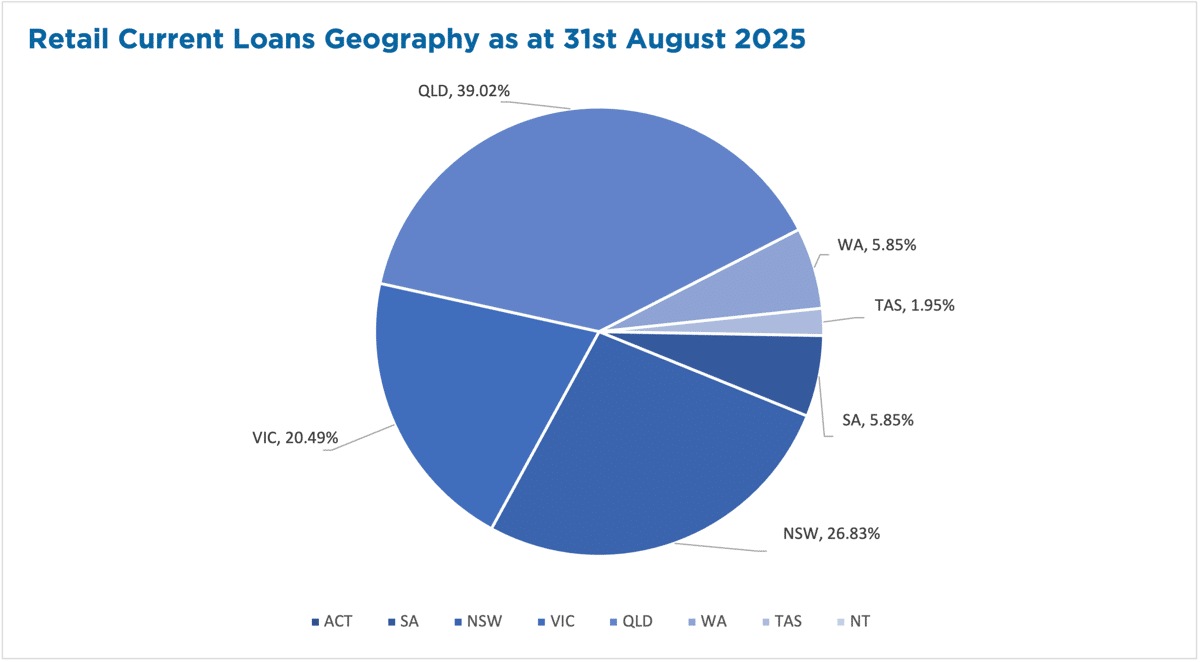

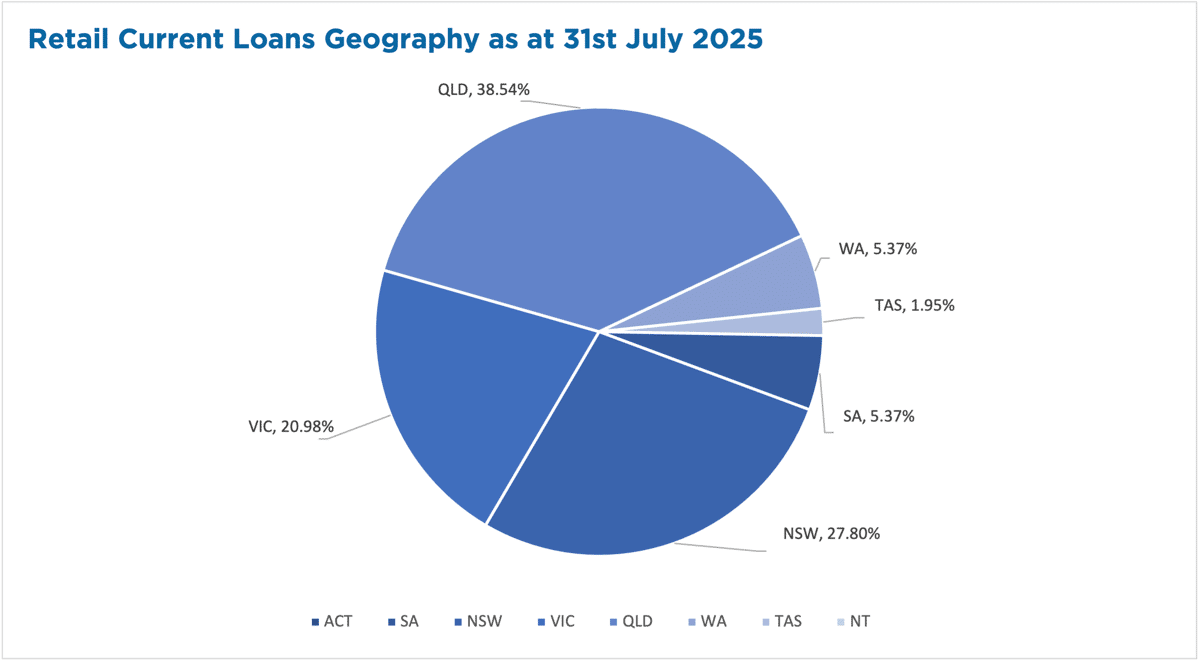

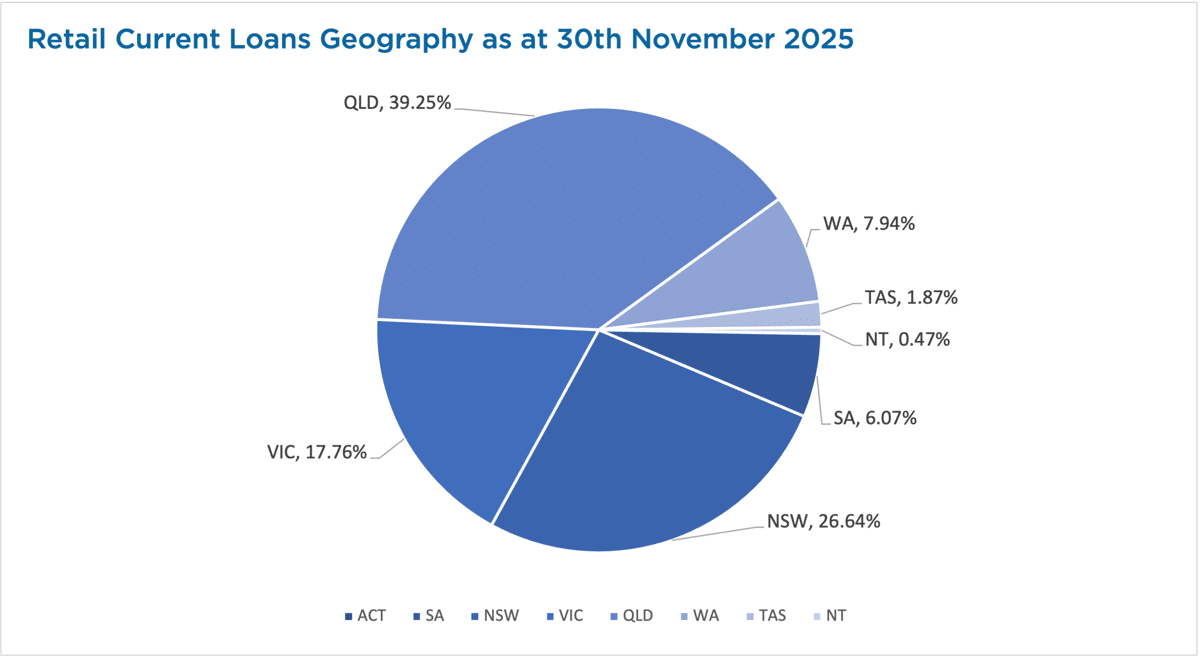

Current Loans Geography

as at 30th of November 2025

To learn more, see our Borrower FAQs.

Why Invest with ASCF?

Make This the Year You Finally Start Investing: Why a Pooled Mortgage Fund Could Be a Great First Step

Every year, many people set the same financial resolution: “This is the year I start investing.”

But life gets busy (work, family, everything in between) and before you know it, another year has passed without taking action.

If this sounds familiar, a pooled mortgage fund may be a simple, low-maintenance way to begin exploring investment opportunities.

A Consistent, Structured Investment Approach

When you’re new to investing, confidence matters. Pooled mortgage funds aim to provide stable, regular returns by spreading your investment across a portfolio of property-secured loans. It’s a way to access a diversified pool of loans without relying on the performance of a single property or asset.

No Property Management, No Stress

If the idea of tenants, maintenance, or managing a property has held you back, a pooled mortgage fund offers exposure to property-backed investments without the responsibilities of being a landlord.

Start With a Smaller Upfront Commitment

A major reason many people hesitate to start investing is the size of a typical property deposit. Pooled mortgage funds allow investors to participate in the property lending market with a smaller initial amount, making it a more accessible entry point.

Diversification to Help Manage Risk

Investing all your money into a single property can concentrate your risk. A pooled mortgage fund spreads your investment across multiple loans, each secured by property, helping reduce exposure to any single borrower or market.

More Flexibility Than Direct Property Ownership

Unlike owning a property — which can take time to sell — pooled mortgage funds generally offer clearer terms around withdrawals at the end of your investment period. This may provide more flexibility as your financial goals evolve.

Professionally Managed

ASCF’s pooled mortgage funds are managed by an experienced team who oversee loan assessments, approvals, and repayments. They handle the operational side so you can get started without needing to be an expert.

If you’ve been putting off investing, this could be the year to take the first step.

A pooled mortgage fund offers an accessible, professionally managed way to begin your investment journey — without many of the barriers that traditionally stop first-time investors.

Want to learn more? Contact us to explore your investment options.

Important information: Since inception, all investors have received their targeted distribution rate monthly and all redemption requests have been paid on time and in full, however past performance is not indicative of future performance. Distributions are not guaranteed nor a forecast. Lower than expected returns may be achieved. Investment in the Funds is not a bank deposit and investors risk losing some or all of their capital. Withdrawal rights are subject to liquidity and may be delayed or suspended. Read the PDS and TMD, available from our website.

An Interesting Transaction

Problem:

A broker came to ASCF with a self-employed client who had taken on a number of unsecured business loans to assist with cashflow and growth. The repayments on these loans had become unsustainable for his business and had in fact, impacted his cashflow and his ability to meet his other liabilities. The broker was unable to find a bank willing to consolidate the number and type of debts that the borrower had accumulated.

Solution:

ASCF was able to consolidate all seven unsecured business loans into a 2nd mortgage. The 2nd mortgage meant that the borrower only had one monthly repayment to make, simplifying their loan repayment arrangement as the business loans had repayment structures ranging from daily to weekly to monthly repayments. These were very time consuming and nearly impossible for the borrower to track.

Most importantly, ASCF’s loan saved the borrower over $15,000 in monthly interest.

The LVR on the security property was 57% with ASCF relying on a panel valuer’s full valuation report.

ASCF provided a total loan of $442,000 over 12-months with an annual rate of 16.95%.

Although ASCF provided a 12-month term, the monthly savings provided by the loan meant that the borrower was in a position to refinance and exit our loan within four months to a traditional bank.

What ASCF does differently

| ASCF was able to see that our facility would provide a material benefit to the borrower, their business and their state of mind. The monthly cash flow benefit helped the borrower to grow and focus on their business rather than costly and complicated repayment structures. |

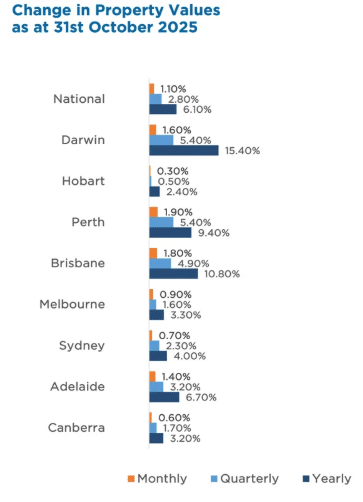

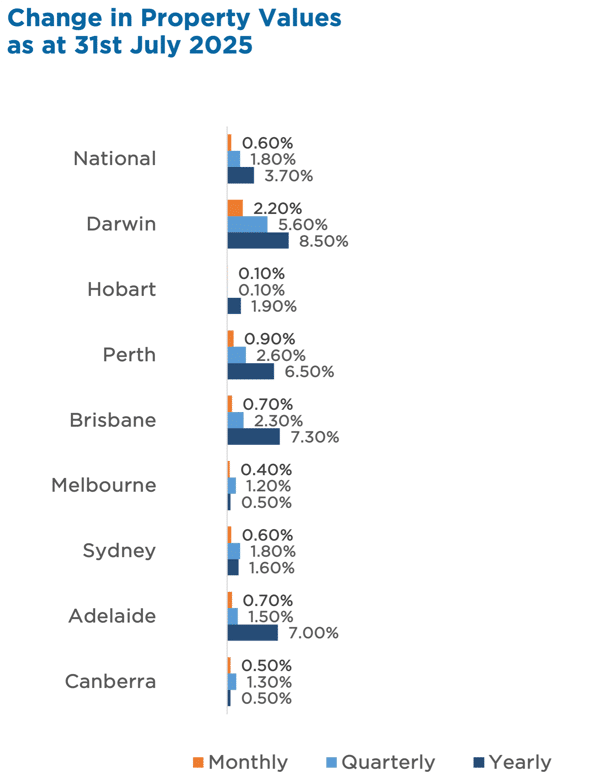

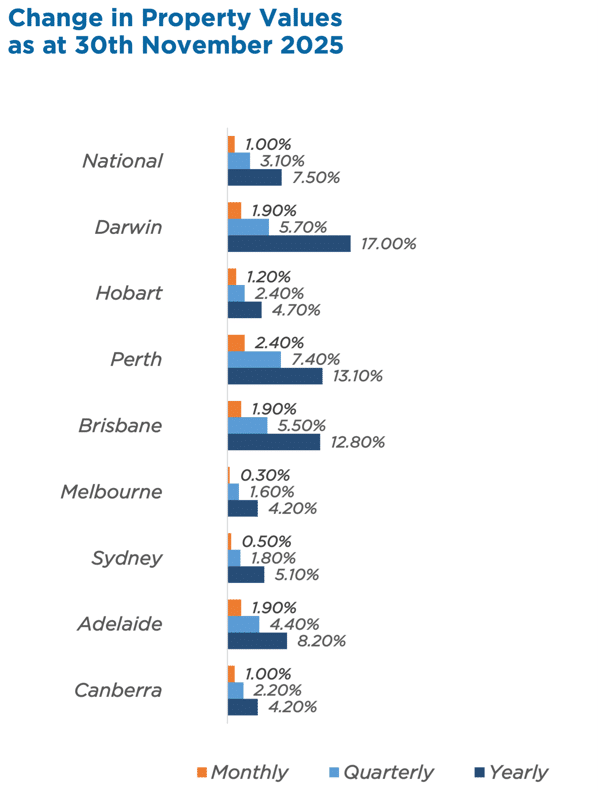

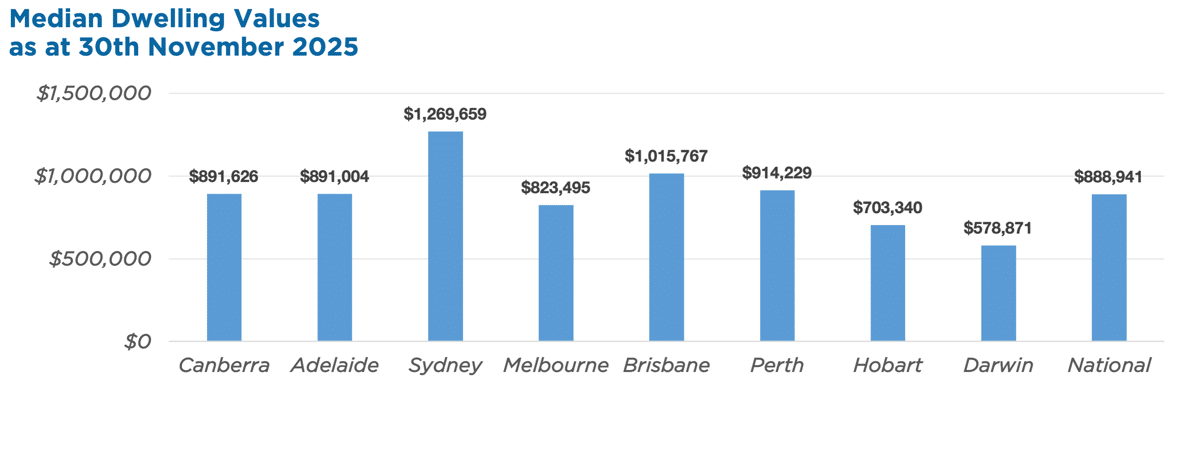

Market Update

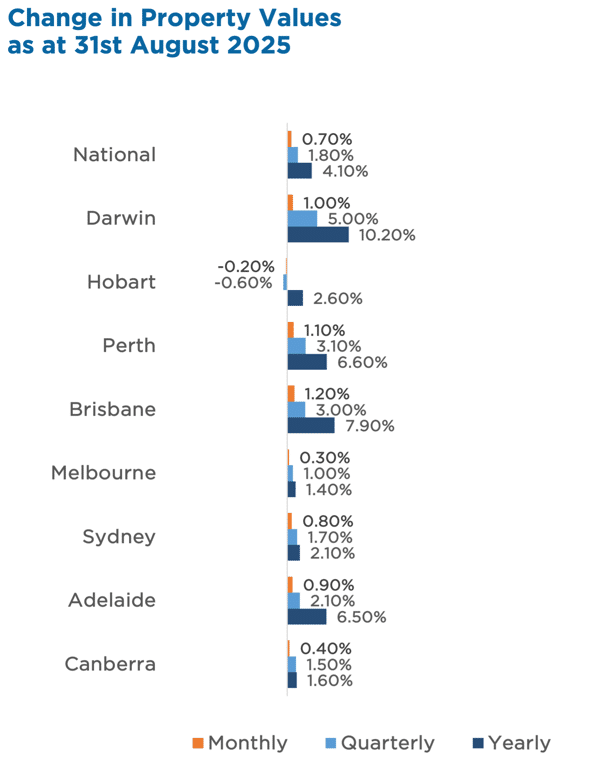

Home values rose another 1.0% in November, marking three straight months of solid gains, but momentum is shifting. Mid-sized capitals are doing the heavy lifting – Perth surged 2.4% – while Sydney and Melbourne continue to cool under affordability pressure.

Record-high value-to-income ratios and rising serviceability hurdles are starting to reshape buyer behaviour, with demand flowing toward lower-priced segments. Inflation has also ticked higher, and with rate cuts now off the table for the foreseeable future, borrowing power and sentiment may soften heading into 2026.

For investors, the key theme remains clear: tight supply and population growth continue to support prices, but affordability constraints are now playing a bigger role in where the growth is occurring.

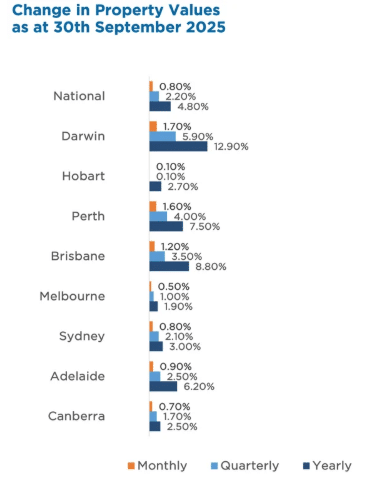

Property Values

as at 30th of November 2025

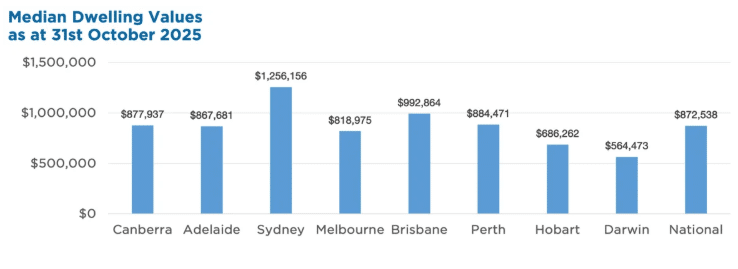

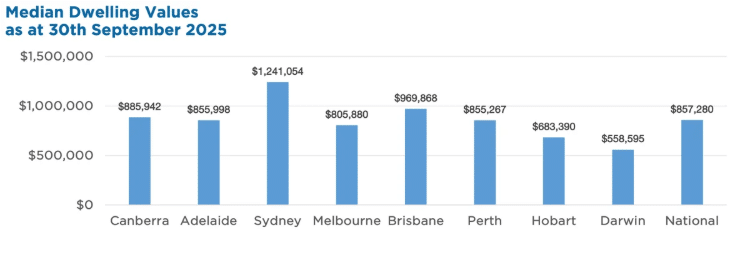

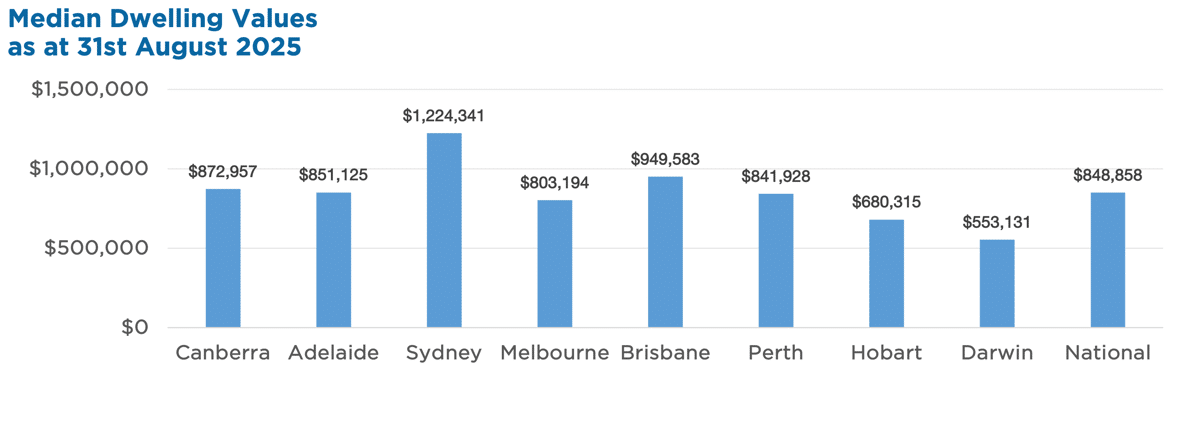

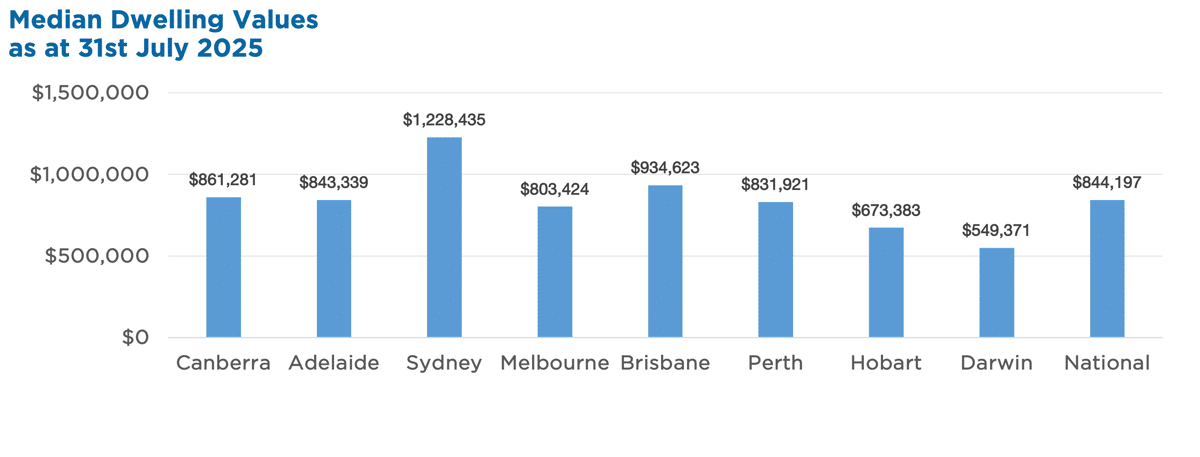

Median Dwelling Values

as at 30th of November 2025

Source: Cotality HVI, 1 Dec 2025

Continue Reading